Reviewed and Validated by: Srijan Jha, Associate

Introduction

Over the last several years, a growing number of Indian businesses have taken the step to convert their existing partnership setups into private limited companies. While the traditional partnership structure works well during the initial stages of operation, many businesses eventually outgrow its limitations, particularly when it comes to liability exposure, investor readiness, and compliance expectations.

This article provides a detailed legal and procedural guide on how to convert a partnership firm into a private limited company under Indian law. The objective is not only to outline the statutory route but also to assist founders in navigating the practical steps involved during the transition, from documentation and registration, all the way to post-conversion compliances.

A typical partnership-to-private limited company conversion may be triggered by a variety of business needs:

- The firm is looking to attract institutional investment or external funding

- The partners want to limit personal liability in case of disputes or insolvency

- The company seeks better recognition and governance under the Companies Act

- The existing business is growing and needs a more robust structure for scalability

Regardless of the reason, the legal shift from partnership to private limited company in India brings significant implications, from ownership structure and taxation to compliance and operational controls.

The partnership conversion procedure is properly documented in the Companies Act, 2013, which lists all the formalities and required documentation for execution. This includes satisfying conditions under Section 366 of the Act, obtaining requisite consents, and filing forms like SPICe+ and URC-1.

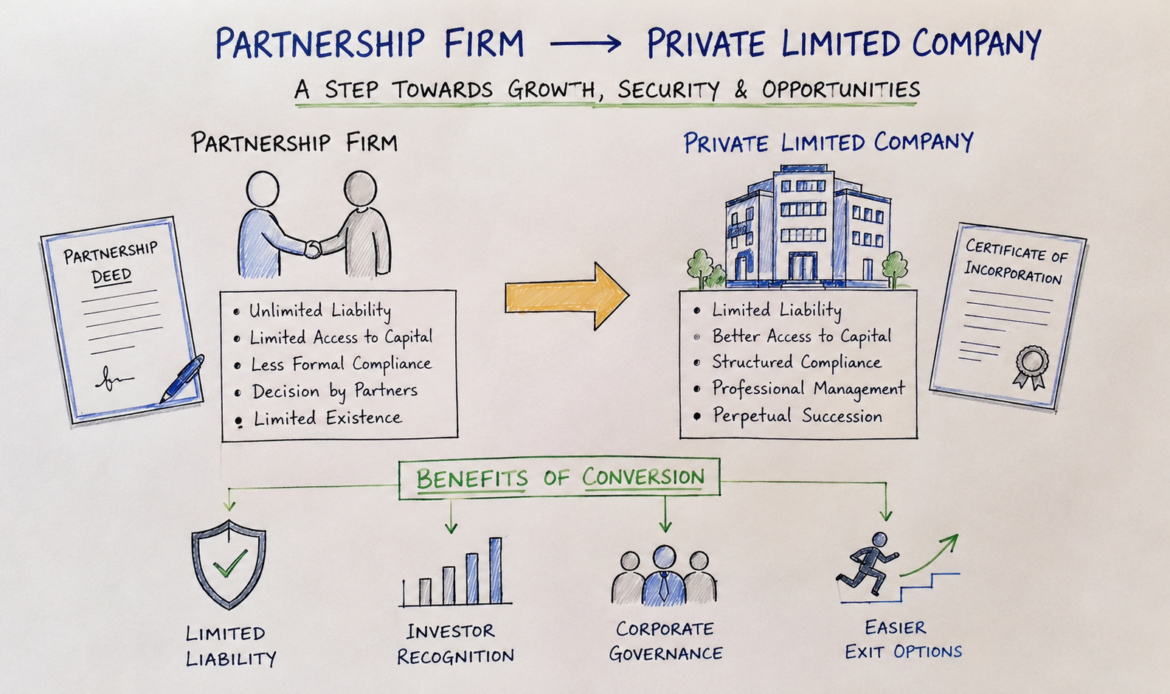

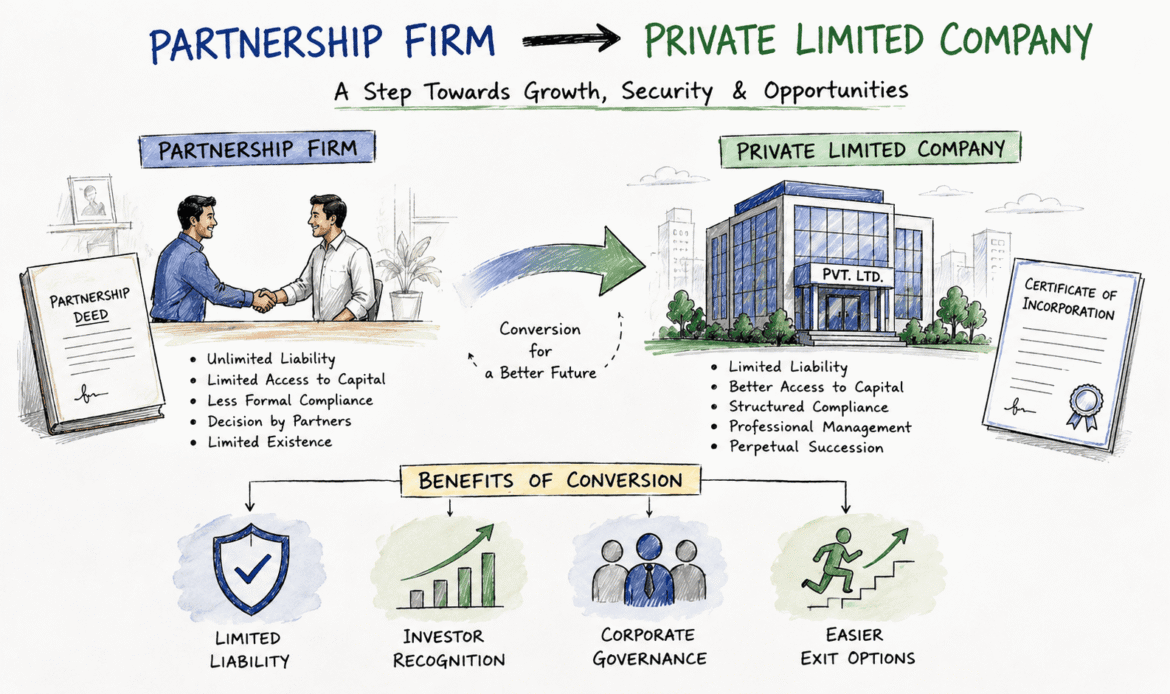

Key Differences Between Partnership Firms and Private Limited Companies

When a partnership firm is converted to a private limited company, the law treats the converted entity differently altogether. Everything from liability to investor perception to regulatory reporting changes.

The fundamental differences between a partnership firm and a private limited company are listed below:

Legal Structure and Recognition

A partnership firm is governed by the Indian Partnership Act, 1932. It may be registered or unregistered, and its existence is not independent of its partners. It is, in essence, a collection of individuals doing business together.

A private limited company, on the other hand, is a body corporate under the Companies Act, 2013. It is treated as a separate legal person, can sue and be sued, and continues to exist beyond the life or death of any one shareholder or director.

For businesses seeking more formal recognition, the shift from a partnership to a private limited company in India offers a significant elevation in status. The new structure is recognised by banks, NBFCs, and investors as a standard form of entity for commercial engagements.

Liability and Ownership

The liability in a partnership is personal. Each partner is jointly and severally liable for the actions of the firm, even those taken by another partner. This can be an issue if the firm faces losses, penalties, or legal proceedings. In a private limited company, shareholders’ liability is limited to the value of shares they hold. This shields personal assets unless there is a case of fraud or misrepresentation. Therefore, when a firm evaluates how to change partnership firm to a private limited company, the major reason for such a change is the limited liability for a private limited company.

In terms of ownership, it is also more structured for a company as shares define ownership. For partnerships, ownership is percentage-based and not easily transferable.

Taxation and Compliance

Significant differences are observed during the growth stages of a partnership firm and a private limited company. Partnership firms are taxed at a flat rate of 30% plus surcharge and cess, regardless of income slabs. Also, remuneration and interest paid to partners are subject to limits under the Income Tax Act.

Private limited companies are also taxed at 25% (for companies with turnover less than ₹400 crore), but are eligible for certain deductions and benefits under various schemes.

In terms of compliance:

- Partnerships file a simple ITR-5; no need to get ROC filings done.

- Private limited companies must file annual returns, board resolutions, statutory registers, etc.

Compliance adds workload, but also formalises the business. If you’re looking at private limited company registration after a partnership, these obligations are worth preparing for in advance.

Capital Raising Capabilities

This is where the biggest limitation of partnerships is felt. Firms cannot issue shares. So, raising capital means bringing in more partners, which dilutes control and creates legal risks.

Private limited companies, however, can issue equity shares, preference shares, and convertible notes, subject to the Act and FEMA regulations. That’s why most investors, especially institutional ones, will ask for conversion before investing.

So, if fundraising or ESOPs are in your growth plan, this is your signal to initiate the partnership firm conversion procedure under the correct route.

Conditions for Conversion Under the Companies Act, 2013

Converting an existing partnership into a private limited company is permitted under Section 366 of the Companies Act, 2013. However, several legal conditions must be satisfied before your application is accepted by the Registrar of Companies (RoC). This section outlines those key conditions so that founders can ensure compliance before filing.

Consent of All Partners

The first non-negotiable step is unanimous consent. All existing partners of the firm must agree to the conversion. There should be:

- A resolution was passed by the partners.

- An affidavit or declaration from each partner affirming no objection.

- A statement agreeing to the takeover of assets and liabilities by the proposed company.

This becomes the backbone of the application when one converts a partnership firm into a private limited company. Partial consent doesn’t work. MCA portals require all partner names to be uploaded and mapped to the new shareholder/director list.

Requirements under Section 366 of the Companies Act

Section 366 governs the conversion of firms, LLPs, societies, and other “unregistered companies” into companies under the Companies Act.

Key conditions under Section 366 include:

- The firm must have at least 2 members at the time of conversion.

- The company to be formed must be for a lawful object.

- All documents must be filed as per Rule 3 and Rule 4 of the Companies (Authorised to Register) Rules, 2014.

- No part of the firm’s income or property can be distributed among members other than by way of a dividend post-conversion.

- Newspaper advertisement is required to be published in two languages (in some cases).

Any non-compliance here will cause delays or rejections in the process of partnership with a private limited company in India.

Number of Members and Directors

The new private limited company must:

- Have at least 2 shareholders and 2 directors.

- Maximum of 200 shareholders.

- At least one director must be a resident in India (per Section 149 of the Companies Act).

In most cases, the existing partners become both shareholders and directors. But if a partner isn’t willing to take a DIN or digital signature, they can remain only as a shareholder.

It is to be noted that the directors and shareholders need not be the same people. But at least two directors must be named during incorporation.

Name Availability and Reservation (RUN)

The company’s name must be reserved with the Ministry of Corporate Affairs (MCA) before the incorporation documents can be filed. This is done through the RUN (Reserve Unique Name) service.

Requirements:

- The proposed name must not conflict with existing registered companies or trademarks.

- Use of the suffix “Private Limited” is mandatory.

- If the firm name is being retained, an NOC must be filed.

- Ideally, apply with two name options to avoid rejection.

The RUN application is not the same as the incorporation form. It’s a separate filing and must be approved first.

If the name is rejected, it causes cascading delays in the rest of the partnership firm conversion procedure.

No Objection Certificate from Registrar of Firms (if registered partnership)

Suppose the original partnership firm was registered with the Registrar of Firms (RoF) under the Indian Partnership Act. In that case, a No Objection Certificate (NOC) from that office is often requested by the MCA.

While not explicitly mandated in every case, several RoCs insist on it as part of their internal checklist. It’s safest to get it upfront.

Details to be included in NOC:

- Date of firm registration.

- Details of partners at the time of registration.

- Confirmation that there are no pending legal or regulatory issues.

- Statement permitting conversion into company format.

For unregistered partnerships, this step may be skipped, but you must submit an affidavit stating the same.

Step-by-Step Procedure for Conversion

The Ministry of Corporate Affairs has laid out a structured process for those intending to convert a partnership firm into a private limited company. While the steps look simple on paper, in practice, most delays and rejections happen due to skipped forms, missing affidavits, or incorrect attachments.

To avoid delays and rejections, the founders must follow each step carefully, keeping in mind timelines, supporting documents, and the review of draft filings.

Below is a breakdown of the practical process followed for a partnership to a private limited company in India:

Step 1: Convene a Meeting of Partners and Pass Resolution

The first step is internal, before any MCA form is touched. All partners must meet, agree on the decision to convert, and record it formally.

The checklist for this step includes:

- Minutes of Meeting stating intent to convert.

- Resolution passed with unanimous approval.

- Decision on who will become directors and shareholders.

- Authorisation to one partner to execute the incorporation process.

This is especially important where the firm has multiple partners. Disputes later about consent can invalidate the entire partnership firm conversion procedure.

Step 2: Obtain Digital Signature and DIN for Directors

Since all filings with MCA are digital, each proposed director must:

- Obtain a Class III Digital Signature Certificate (DSC) from a licensed certifying authority.

- Apply for Director Identification Number (DIN) through the SPICe+ Part B form (or earlier if preferred).

It’s advisable to get this done before the name reservation so that the form-filling becomes smoother later. A maximum of three DINs can be applied for through SPICe+.

List of documents required for DSC/DIN:

- PAN card copy (mandatory for Indian citizens)

- Aadhaar card or passport copy

- Passport-size photograph

- Mobile number and personal email ID

- Address proof (utility bill, bank statement, etc.)

At least 2 directors are necessary to incorporate a private limited company. MCA won’t allow incorporation until at least 2 DINs are generated and mapped.

Step 3: File Name Reservation Application (RUN Service)

The next step is to secure a name for the new private limited company using the Reserve Unique Name (RUN) facility on the MCA portal.

Key rules:

- Name must not be identical or too similar to an existing company, LLP, or registered trademark.

- “Private Limited” must be added at the end.

- If the existing partnership name is being retained, attach NOC on the letterhead of the firm

- It is advisable to check availability on the MCA and IPIndia portals before filing.

The name gets reserved for 20 days. If not used within that period, a fresh application must be made.

It is advisable to apply with two name options, as rejections can cause timeline slippage.

Step 4: Draft and Approve MOA & AOA

Once the name is approved, the Memorandum of Association (MOA) and Articles of Association (AOA) must be drafted.

- MOA outlines business objectives, liability clause, capital, and name.

- AOA governs internal rules, director powers, shareholder rights, etc.

Care should be taken while drafting these documents, as errors here can delay the private limited company registration after the partnership.

Important clauses:

- Capital clause (must match declared shareholding).

- Object clause (should reflect old business + expansion plans).

- Subscriber sheet signed by all proposed shareholders with a witness.

Tip: For simple structure, consider using model Table-F of the Companies Act for AOA.

Step 5: File SPICe+ Form and E-Form URC-1

This is the core step. You now need to file SPICe+ (Parts A & B) and E-Form URC-1.

What they include:

- SPICe+ A – Company Name.

- SPICe+ B – Company details, director info, registered office, share capital.

- URC-1 – Declaration of conversion from partnership to company.

Documents to be attached:

- Partnership deed

- No Objection Certificates (NOC) from partners and creditors

- List of assets and liabilities

- Affidavit stating that the firm has not been dissolved

- Details of partners, their DINs or PANs

- Consent letters to become directors

This is the most sensitive part of the entire partnership firm conversion procedure. Even a small mismatch (like a partner’s name spelling) can lead to rejection. Consultation with a professional is advisable at this stage if one is unsure.

Step 6: Publish Newspaper Advertisement (as required)

If required by the RoC, an advertisement must be published in:

- One English daily.

- One vernacular language paper in the principal place of business.

Format is prescribed under Rule 4(1) of the Companies (Authorised to Register) Rules, 2014. It must state:

- Name of the partnership firm and the proposed company

- Intention to convert

- Request to raise objections within 21 days (if any)

This step is sometimes waived by RoCs if the firm is small and local, but it’s better to prepare for it in advance.

Read another article: Trademark Registration in India

Step 7: Obtain Certificate of Incorporation

If all forms and declarations are accepted, MCA will issue a Certificate of Incorporation (COI), signifying that the firm has now become a private limited company.

Details in the certificate:

- New CIN (Corporate Identity Number)

- Date of incorporation

- PAN and TAN (if applied via AGILE-PRO form)

- MCA login credentials for company filings

This marks the legal end of the conversion process. From here on, the firm ceases to exist as a partnership and becomes a company.

Summary Table: Conversion Process Snapshot

| Step | Action | Form / Output |

| 1 | Partners’ Resolution | Internal Resolution |

| 2 | DSC + DIN | DIN Approval Email |

| 3 | Name Reservation (RUN) | Name Approval from MCA |

| 4 | Draft MOA/AOA | Signed Docs (PDF) |

| 5 | SPICe+ + URC-1 Filing | Incorporation Application |

| 6 | Newspaper Ads (if required) | Copy of Published Notices |

| 7 | Certificate of Incorporation Issued | COI + CIN + PAN/TAN |

Documents Required for Conversion

Here’s where a lot of applications get delayed or rejected, because the documentation isn’t fully aligned. MCA requires specific records when reviewing applications to convert a partnership firm into private limited company.

Every file must be clean, signed, and as per format. Older or expired documents (like outdated licenses or PAN mismatch) should be fixed before submission.

Below is a full checklist of documents that need to be kept ready.

1. Partnership Deed

- Must be stamped and executed

- If there are amendments, include all addendum deeds

- Should match names and capital contributions as declared in the forms

This is the foundational proof of your existence. Missing deed results in rejection.

2. Consent Letters from Partners

- Format must state that all partners agree to the conversion

- Also declare who will act as shareholders and directors post-conversion

- To be signed by all partners with date and place

Sometimes RoC insists on notarised consent letters. Keep signed hardcopies ready.

3. No Objection Certificate from Creditors

- Declaration from principal vendors, lenders, or service providers

- Confirms that they have no objection to the conversion

- At least two major creditor NOCs are usually sufficient

This assures RoC that you’re not running away from financial obligations.

4. Latest IT Returns and Business Licenses

- Copy of the latest Income Tax Return filed under the firm’s PAN

- GST certificate (if applicable)

- Shops & Establishments Certificate, FSSAI license, trade license, etc.

These support the firm’s financial activity and business operations history.

5. Identity & Address Proofs of Directors

Each proposed director must submit the following documents:

- PAN card copy

- Aadhaar card or passport copy

- Bank statement or utility bill (not older than 2 months)

- Passport photo

- Mobile number and email ID for OTP verifications

Ensure that the address in the DIN matches with ID proof. Mismatches cause DIN rejections.

6. Affidavit and Declarations as per URC Rules

- Affidavit confirming that the firm has not been dissolved

- Declaration of assets, liabilities, pending cases (if any)

- Declaration under Rule 3(1) of the Companies (Authorised to Register) Rules

These forms are standard templates, some RoCs require them on ₹100 stamp paper.

Post-Incorporation Compliance

Once you receive the Certificate of Incorporation (COI) and the private limited company is officially formed, the transition is not over. Several post-registration compliances must be followed immediately, both statutory and practical. These ensure your newly incorporated company starts operating without legal disruption and avoids penalties later.

This section lists what must be done after the legal conversion of a partnership to a private limited company in India is complete.

PAN/TAN Application and Bank Account

If the PAN and TAN weren’t generated during the SPICe+ application (AGILE-PRO part), they must be applied separately.

Checklist:

- Apply for company PAN via the NSDL or UTIITSL portal.

- Apply for TAN (Tax Dedication Account Number) for TDS compliance.

- Submit COI, MOA, AOA, and PAN to open a current account in the company’s name.

- Shareholder and director KYC will be required by most banks.

Some banks also request a Board Resolution authorising account operation. Draft it immediately after incorporation to avoid delays.

Failing to open a current account quickly may disrupt vendor payments and invoice raising, slowing business post conversion.

GST Migration (if applicable)

If the original partnership was registered under GST:

- Apply for an amendment in the core fields on the GST portal.

- Upload the Certificate of Incorporation and the new PAN.

- Change the legal name and the constitution of the business.

- Retain GST number (if approved) or apply afresh if the portal does not permit transition.

If not updated timely manner, invoices raised under the old firm name become legally questionable.

For proper private limited company registration after a partnership, GST continuity must be handled properly.

Transfer of Assets and Liabilities

All assets of the partnership, movable and immovable, must now be reflected in the company’s books.

Required steps:

- Pass Board Resolution for the takeover of assets and liabilities

- Prepare a statement listing each asset: laptops, furniture, inventory, etc.

- Update ROC records where applicable (e.g., leased premises or IP assigned)

- Stamp duty may be applicable if the transfer is documented formally

Also, update the books to reflect outstanding creditors, debtors, loans, and advances in the company’s balance sheet. This step validates the completion of the partnership firm conversion procedure.

Intimation to Vendors and Clients

Update all third parties, vendors, clients, service providers, about the change in entity status.

Notify via:

- Formal letter or email

- Attach Certificate of Incorporation

- Share new bank details, GST number, and contact sheet

- Update agreements or purchase orders where the firm name appears

This avoids confusion during payment collections, TDS deductions, or contract renewals. In some sectors (e.g., export/import), DGFT or IEC records must also be updated.

Change of Signage, Letterheads, Invoices

One of the practical steps after you convert a partnership firm into a private limited company is rebranding internal materials.

Changes required:

- Office board and door signage must reflect the new name with CIN.

- Letterheads must carry the company name, CIN, registered office address, email, and website (if any).

- Update invoice template to reflect new entity (with GST and PAN).

- Employee email signatures and business cards should be changed.

Ensure that all communication now goes out in the company’s name to build credibility and compliance continuity.

Summary Table: Post-Incorporation Compliance

| Area | Compliance Item | Notes / Timeline |

| Legal & Tax | Apply for PAN & TAN | Immediately after COI |

| Regulatory (GST) | Update GST profile / apply afresh | Within 30 days |

| Financial | Notify vendors, clients of the change | Within 1 week post COI |

| Accounting | Pass resolution for asset takeover | Within 10 days |

| Communication | Change signboards, email signatures, and invoices | Within 2 weeks |

| Branding / Stationery | Before raising the next invoice | Before raising next invoice |

Tax and Accounting Considerations

Many founders treat incorporation as a paperwork task, but it carries serious tax implications, too. The act of converting a firm to a company changes your tax identity, accounting treatment, and asset depreciation timelines. If not reviewed carefully, this can lead to double taxation, disallowed deductions or blocked input credits.

Here’s what you must watch for post-conversion under Indian tax law.

Capital Gains Implications

As per the Income Tax Act, Section 47(xiii) allows exemption from capital gains tax on transfer of assets from a partnership to company, only if certain conditions are met:

- All assets and liabilities of the firm become the company’s assets and liabilities.

- All partners become shareholders in the same proportion as their capital accounts.

- No other consideration (like cash) is received by any partner.

- Shareholding must continue for at least 5 years.

If any of these are breached, capital gains will be deemed to have arisen and taxed accordingly.

Therefore, when planning on how to change a partnership firm to a private limited company, this exemption must be planned and documented properly.

Carry Forward of Losses

One common question is whether business losses and unabsorbed depreciation of the partnership can be carried forward to the new company. Under current provisions, such tax benefits do not carry forward during conversion under the Section 366 route (unlike LLP-to-Company in some cases).

Therefore:

- Plan your conversion in a year where taxable profits are expected.

- Finish loss set-offs in the last return of the partnership.

- Start the company books fresh with opening balances (assets/liabilities only).

Depreciation and Revaluation Rules

For all depreciable assets like computers, machinery, vehicles:

- Depreciation restarts from the date of incorporation of the new company.

- Written-down value (WDV) as per the Income Tax Act is to be considered.

- Revaluation is not allowed to inflate the asset base post conversion.

Books should record:

- Original cost

- Accumulated depreciation to date of transfer

- WDV as on the conversion date

If you inflate the asset base, it will be disallowed during tax scrutiny.

GST and Input Credit Transition

If you retained your GST registration:

- Ensure that all closing input credit in the partnership’s books is transferred via TRAN-1 or a relevant form.

- Also transfer closing stock, purchases under reverse charge, and vendor accounts.

If you got a new GSTIN:

- Declare opening stock and claim fresh input credit.

- Close old account with NIL liabilities and input.

Watch for compliance gaps, vendors sometimes continue to issue invoices in the old firm’s name post conversion. This creates reconciliation issues during filing.

Benefits of Conversion

General perception amongst the founders often delays the shift from partnership to company. “Why fix what’s working?” is a common view. But as the business grows, even moderately, its structure starts to strain. From banking restrictions to team scale-up to pitching investors, the gap between a partnership firm and a company becomes too obvious to ignore.

So, when you convert a partnership firm into a private limited company, what exactly improves?

Limited Liability

This is the most immediate, and probably the most practical, advantage. In a partnership, personal assets are at risk. If the business fails or gets sued, creditors can chase the individual partners. There’s no legal shield.

In a private limited company, the liability of each shareholder is limited to the unpaid amount (if any) on their shares. No more, no less. The personal assets of the directors are protected unless there’s fraud or deliberate wrongdoing.

When you’re thinking about how to change a partnership firm to a private limited company, this should be your starting point.

Recognition by Investors and Banks

Venture capitalists, angel networks, and even most banks are more comfortable dealing with a company than a partnership. It’s a known format. It offers better governance, documented shareholding, and regulatory oversight.

Many early-stage startups realise this when they start preparing pitch decks. Without private limited company registration after a partnership, they find it difficult to open new credit lines, get sanctioned for loans, or even onboard on vendor platforms.

A company structure also allows:

- Clear capitalisation tables

- ESOP plans for employees

- External investors to enter via equity

In contrast, partnerships can’t issue shares or raise formal capital.

Corporate Governance Framework

Companies, under the Companies Act, are bound by a mandatory governance structure:

- Board meetings

- Annual filings

- Shareholder resolutions

- Statutory auditor appointment

While this may seem like “extra compliance,” it also introduces discipline, founders start documenting decisions, tracking equity, managing reserves. Over time, this builds trust with regulators, clients, and employees.

The partnership firm conversion procedure becomes an opportunity to reset internal controls and adopt better reporting practices.

Easier Exit Options

Let’s say two partners fall out. In a firm, separation is painful. Assets are disputed, goodwill is hard to divide, and no one knows who owns what.

In a company, exits can be handled through:

- Share buyback

- Share transfer

- Capital reduction

Shares can be valued and monetised. This makes exits smoother, not just between founders but also when onboarding or offboarding investors.

For those planning long-term wealth creation or eventual acquisition, this is one of the underrated advantages of conversion.

Stronger Compliance Image

Clients and large vendors often ask for:

- Incorporation certificate

- GST and ROC filings

- Details of directors/shareholding

- Past annual reports

Having a company structure makes these documents standardised. There’s a central registry (MCA), and partners no longer need to send scanned deeds every time a new client signs up.

Table: Key Benefits of Converting to Company Structure

| Benefit | Partnership Firm | Private Limited Company |

| Liability | Unlimited | Limited to share capital |

| Funding Options | Capital contribution by partners only | Can raise equity, debt, convertible notes |

| Recognition | Informal setup | Can raise equity, debt, and convertible notes |

| Exit Flexibility | Complicated separation | Transfer of shares |

| Document Trail & Filings | No central registry | MCA-backed legal filings |

Common Pitfalls to Avoid

While the process to private limited company in India seems standard, in practice, mistakes are very common. Many incorporation requests are rejected, delayed, or returned with remarks. Others face issues during future audits or tax proceedings because something was skipped during conversion.

Here’s what typically goes wrong, and how to avoid it.

Incomplete Documentation

The number one reason for rejection is missing affidavits, unsigned resolutions, or outdated supporting documents.

Some of the usual misses:

- Old partnership deed does not match the names in PAN

- Consent letters signed without date or place

- List of creditors not uploaded or left blank

- Missing declarations under Rule 3(1) or 4(2) of Authorised to Register Rules

Each form (especially URC-1) requires multiple attachments. Cross-check against the MCA checklist. And always scan and upload clear, legible PDFs, not phone images.

If you’re planning private limited company registration after a partnership, treat the documents as legally binding, not just formalities.

Using Incorrect SPICe+ Formats

SPICe+ Part A and B must be filled out properly. But often:

- DINs are entered incorrectly

- The subscriber sheet doesn’t match the MOA

- The number of shares is miscalculated

- Directors’ residential status not clarified

Even small spelling mismatches between PAN and incorporation forms can cause rejection. You only get two resubmission chances; after that, a fresh filing (and fee) is required. Use professional help at this stage unless you’re confident with MCA filings.

Not Updating Tax Registrations

After you convert a partnership firm into a private limited company, GST, PAN, TAN, and bank records must be updated.

Common mistakes include:

- Using the old PAN for TDS deductions

- Raising invoices under the old GSTIN

- Forgetting to integrate vendor portals like GeM or Flipkart

- Not filing the closure of the partnership’s ITR and Form 16A

This creates future mismatches in tax audits and vendor reconciliations. You may even be penalised for issuing invoices under the wrong legal entity.

Non-Compliance with Section 374 Conditions

Section 374 of the Companies Act, 2013, deals with conditions that must be fulfilled for a valid conversion.

Some of the requirements:

- No income or assets can be distributed to members post-conversion

- Old liabilities must be taken over by the new company

- Directors must give a declaration of solvency

Ignoring these and treating the new company as “fresh” can lead to a denial of legal continuity and attract scrutiny later.

Ensure that the conversion complies with every clause, especially where the business is applying for government tenders or tax exemptions post conversion.

Ignoring Post-Conversion IP Transfer or Leases

This is one that founders forget in the rush. Any IP registered under the partnership firm, trademark, domain, logo, must now be assigned to the new company. The same is the case with:

- Property leases

- Rental agreements

- Cloud licenses and software subscriptions

If not updated, invoices go to the old firm, and legal rights stay fragmented.

Summary Table: Common Pitfalls During Conversion

| Pitfall | Impact | How to Avoid |

| Missing documents or NOCs | MCA rejection or resubmission | Assign to the company post COI |

| Form mismatches in SPICe+/URC-1 | Resubmission, delays | Review all fields twice |

| Old PAN/GST usage post conversion | Tax mismatches and penalties | Notify vendors, update records |

| Section 374 conditions skipped | Loss of legal continuity | Submit all affidavits and solvency docs |

| IP or leases not transferred | Legal confusion and ownership disputes | Assign to company post COI |

Conclusion

Whether you’re running a small traditional setup or a fast-growing business that started lean, there comes a time when the partnership format begins to fall short, be it in terms of liability, structure, or recognition. That’s where the option to convert a partnership firm into private limited company becomes relevant. And more importantly, strategic.

As outlined in this guide, the legal framework under Section 366 of the Companies Act, 2013 offers a clear path to transition, provided all regulatory, tax, and procedural requirements are met. The process involves far more than just an MCA form submission. It includes internal approvals, documentation, statutory filings, post-conversion updates, and compliance restructuring.

If you’re evaluating the shift from partnership to private limited company in India, here’s a brief recap of what you’ll need to navigate:

- Pass internal resolutions and obtain unanimous partner consent.

- Secure digital signatures and DINs for proposed directors.

- Reserve the company name via RUN and file SPICe+ with URC-1.

- Upload all documents: NOCs, affidavits, declarations, lists.

- Receive Certificate of Incorporation and update tax/GST records.

- Transfer assets, liabilities, IP, and notify all external stakeholders.

And all this must align with the guidelines under the Companies (Authorised to Register) Rules, 2014, and Section 374 conditions for legal continuity.

Many businesses also find it useful to take legal help, especially during the SPICe+ and URC filings. The partnership firm conversion procedure has multiple moving parts, and rejections can be costly and time-consuming.

Frequently Asked Questions (FAQs)

1. Can a partnership firm convert into a company without dissolving?

Yes. That’s the core benefit of conversion under Section 366 of the Companies Act. The firm does not need to dissolve. Its assets, liabilities, and operations get transferred to the new company, which takes over the business as a going concern. This ensures continuity and avoids tax or contract disruption. However, formal consent from all partners is required.

2. Is there any minimum capital required for conversion?

No mandatory minimum capital is prescribed by law. You can register the company with as little as ₹1 lakh as authorised capital. However, MCA requires the shareholding pattern and capital clause to be mentioned in the MOA/AOA. Make sure the capital reflects your operational scale realistically.

3. Can the firm name be retained after conversion?

Yes, but with conditions. You must add “Private Limited” at the end and file a No Objection Certificate (NOC) confirming that the partnership firm consents to the name being used by the new company. Also, the name must be available on the MCA portal and not conflict with existing trademarks or companies.

4. Do I need to apply for a new GST number?

That depends. If the GST portal allows migration (amendment of core fields), you can retain the same GST number by updating the entity type and PAN. However, in many cases, especially if the PAN changes (which it does when converting from a firm to a company), you may need to apply for a fresh GSTIN. In either case, notify clients and update invoices immediately post-conversion.

5. How long does the conversion process take?

On average, if all documents are in place, it takes around 15–25 working days from the date of SPICe+ filing to the issuance of the Certificate of Incorporation. However, delays may occur due to:

- Name reservation rejection

- Missing documents or declarations

- Incorrect or inconsistent partner/director details

- Resubmission rounds required by RoC

6. Do I need to file tax returns for both entities?

Yes. You must file a closure return for the partnership firm (till the date of conversion) under ITR-5. After the private limited company is incorporated, it must file its return (ITR-6) for the remaining period of the financial year. Both entities will have separate PANs and must comply with respective tax deadlines.

7. Will my existing contracts and licenses remain valid after conversion?

In most cases, yes, if you notify the respective authorities and counterparties. However, many contracts include a clause stating that a change in legal structure requires prior written approval. You’ll also need to update:

- Shops and Establishments licenses

- FSSAI, DGFT, or MSME registrations

- Vendor agreements, lease deeds, and franchise agreements