Reviewed and Validated by: Srijan Jha, Associate

Introduction – Annual Compliance Checklist

Running a business is already hard, but staying compliant as a private limited company in India. That’s a whole different game. And the real issue? Most founders think compliance ends with company registration, whereas that’s just the beginning.

Under Indian law, there’s a long list of annual duties that every private limited company is expected to fulfil, from filing financial statements to maintaining board resolutions and statutory registers. The compliance timeline stretches across the whole financial year. Ignoring these doesn’t just invite late fees, it can even lead to the disqualification of directors or the de-registration/striking off of the company itself.

This is why having a well-documented annual compliance checklist for private limited companies is no longer a good-to-have; it’s non-negotiable. Whether a company has one employee or one hundred, the Companies Act annual filing obligations remain the same.

Unfortunately, many companies don’t maintain proper records and depend entirely on CAs or outsourced consultants without verifying what’s being filed. This leads to:

- Incorrect filings with the Registrar of Companies (ROC).

- Missed deadlines for DIR-3 KYC, AOC-4, or MGT-7.

- Non-compliance with board meeting requirements and statutory registers.

- Late income tax return for a private limited company under ITR-6.

- Errors in ROC filing requirements lead to heavy penalties.

Some founders assume that if there’s no profit or activity, there’s no need to file. This is a legal mistake; even dormant companies must comply with the annual filings under the Companies Act.

If you’re a director, CFO, or startup operator, this guide is designed to help you stay on track. It’s not about overwhelming you with jargon, but showing what needs to be done, by when, and how. Even if one task on this list is being skipped or outsourced blindly, it’s probably time to fix that.

Why Annual Compliance Checklist Matters for Private Limited Companies

Most business owners in India are so focused on sales, hiring, and operations that they forget to comply with the basic compliances. And when it comes to a private limited company, these basics aren’t optional. They’re legal duties under the Companies Act, not best practices.

Many directors don’t realise how serious the consequences can be. Just missing a few filings, not holding board meetings properly, or skipping an auditor’s report can create a chain of penalties that can be detrimental to the existence of the company and drain both money and time.

The need for an annual compliance checklist for private limited companies goes far beyond just avoiding MCA notices. It’s about protecting the company’s legal existence and the reputation of its leadership. Here’s why it matters:

1. It’s a Legal Obligation Under the Companies Act, 2013

Every private limited company is bound by law to file annual returns, maintain records, and hold meetings, even if the business is inactive or has zero turnover. Skipping filings doesn’t mean “no one will notice”. The Registrar of Companies (ROC) tracks defaults by companies and initiates legal action against such defaulting companies.

2. Avoidance of Penalties and Director Disqualification

Under ROC filing requirements, even a one-day delay in filing a form can lead to a penalty of ₹100 per day for every continuing day, and there is no maximum cap. The director of a defaulting company can also be disqualified from being appointed or reappointed as a director under Section 164 of the Companies Act 2013, if the company, fails to file financial statement or annual returns for any continuous period of three financial years or fails to comply with any other provisions of the said section. Some directors believed that this rule only applies if fraud is committed. That’s incorrect; the law applies even to filing lapses.

3. Essential for Funding, Tenders & Business Growth

Investors, VCs, and even government authorities check your Companies Act annual filing status before issuing funds or approving tenders. Incomplete or missing filings suggest carelessness or even red flags. That’s why many startups with solid products still face funding blocks, because the income tax return for their private limited company wasn’t filed properly, or MGT-7 was overdue.

4. Builds Trust With Stakeholders

Timely filings and documented governance show maturity. Whether it’s employees, clients, partners, or shareholders, people want to work with companies that are clean on paper. A proper statutory compliance checklist for companies isn’t just for internal use; it becomes your shield when questions are raised.

5. Protects Against Strike-Off or MCA Intervention

Companies that don’t comply for extended periods risk being marked as “strike-off” under MCA records. Getting reinstated isn’t easy, and the directors face permanent records of non-compliance, thereby limiting future business activities.

Too often, compliance is seen as “the CA’s job”, and this mindset leads to errors, missed deadlines, and vague documentation. Legal responsibilities under labour law compliance in India and HR compliance requirements in India aren’t limited to labour issues; they tie into every part of company operations, including how directors function and how filings are handled.

In short, annual compliance is not paperwork; it’s your foundation. Get that wrong, and everything built on it will shake sooner or later.

Mandatory Annual Compliance Filings under the Companies Act, 2013

Once a company is registered as a private limited company, most directors feel like the legal work is done; that’s not even close to the truth. The real legal responsibility starts after registration. Every year, companies are required to file multiple forms with the Registrar of Companies (ROC) as part of their ongoing obligations.

Skipping these filings or doing them without accuracy can lead to penalties, disqualification of directors, and even company strike-off. A proper annual compliance checklist for private limited companies always starts with these core filings under the Companies Act annual filing norms. These aren’t optional; these are mandatory, even if your company didn’t operate or make any revenue during the financial year.

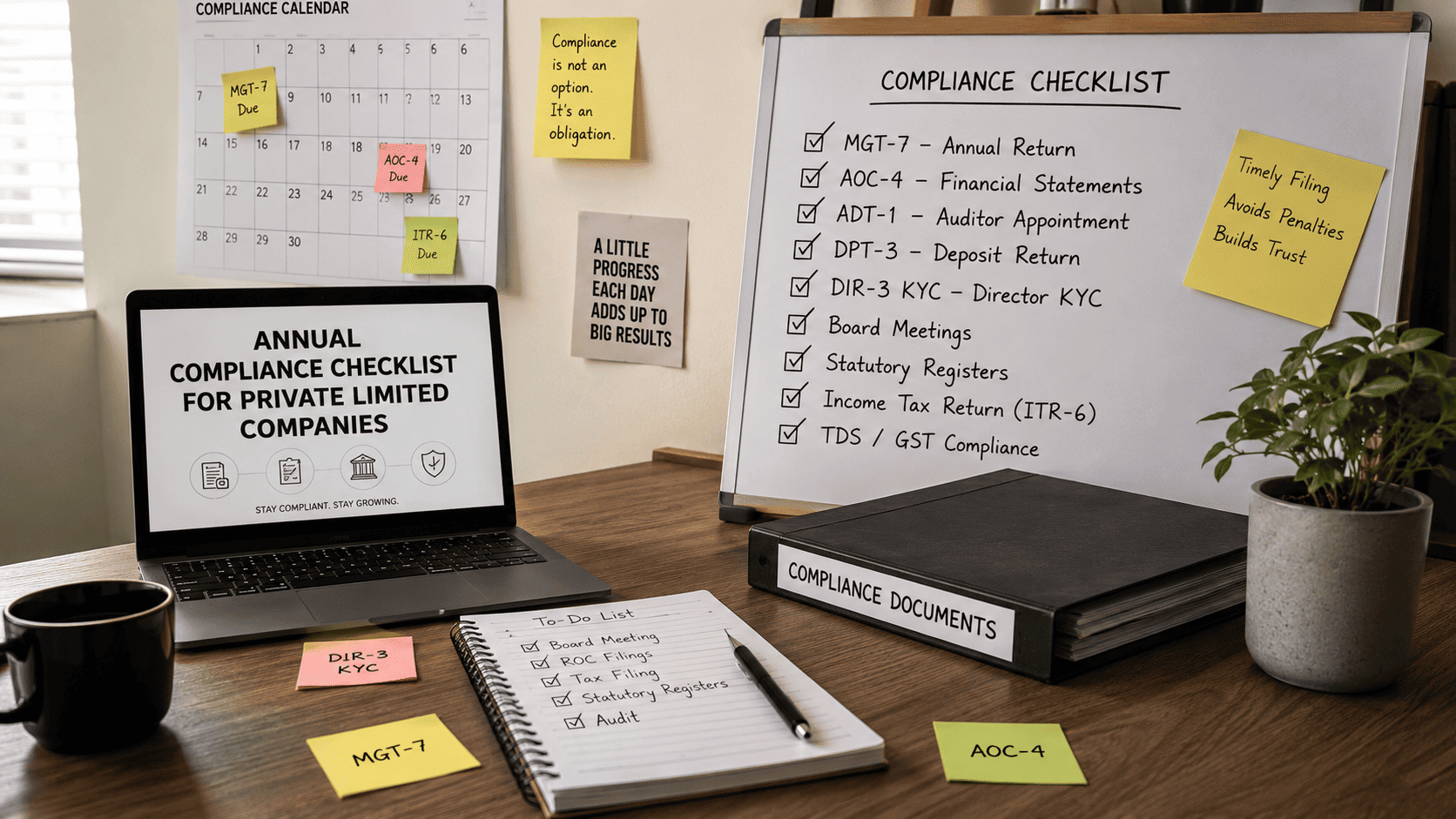

1. Form MGT-7 – Annual Return

- Filed within 60 days of the Annual General Meeting (AGM).

- Includes details of shareholding, directors, members, and changes in capital structure.

- Applicable to all private limited company types, regardless of turnover.

- Many companies don’t file this if there were no shareholder changes, which is legally incorrect.

2. Form AOC-4 – Financial Statements

- Filed within 30 days of AGM.

- Includes Balance Sheet, P&L, Board Report, Auditor’s Report.

- Filing is mandatory even for companies with NIL income.

- Some companies assume they can file AOC-4 after tax filing, whereas it must be filed before that.

3. Form ADT-1 – Auditor Appointment

- Required to be filed within 15 days of the AGM.

- Used to inform the ROC about the appointment or reappointment of an auditor.

- Many companies don’t file Form ADT-1 if the auditor hasn’t changed, whereas it must be filed every term.

4. Form DPT-3 – Return of Deposits

- Filed annually before 30th June.

- Required for all companies with loans, advances, or borrowings, even if from directors or group entities.

- One legal confusion is that some companies assume it applies only to NBFCs or finance companies, whereas Form DPT-3 applies to all non-exempted private companies.

5. DIR-3 KYC – Director KYC Filing

- Every director with a DIN must file this annually.

- Filing after the due date results in DIN deactivation.

- No exemptions, even if the director is inactive or resigns later in the year.

- Companies often forget that new directors must also file within the same cycle.

6. Holding the Annual General Meeting (AGM)

- Must be held within six months from the end of the financial year.

- Even if there’s only one shareholder, the AGM still needs to be recorded and minuted.

- If AGM is skipped, companies cannot legally file MGT-7 or AOC-4.

- Many startups assume that a board meeting is enough in place of AGM, whereas AGM must be held within six months from the end of the financial year.

Compliance Snapshot Table – Annual Compliance Checklist

| Compliance Item | Form / Requirement | Due Date | Common Mistake |

| Annual Return | MGT-7 | Within 30 days of the AGM | Filed only if changes occurred |

| Financial Statements | AOC-4 | Within 15 days of the AGM | Delayed until ITR filing |

| Auditor Appointment | ADT-1 | Treated the same as board meeting | Not filed if the auditor remains unchanged |

| Deposit Returns | DPT-3 | Before 30th June | Filed only by NBFCs |

| Director KYC | DIR-3 KYC | Usually 30th September | Ignored for newly appointed directors |

| AGM | Minutes + Resolutions | By 30th Sept (for March F.Y. end) | Treated the same as a board meeting |

Companies that build systems around these tasks by incorporating reminders, approvals, and pre-filled templates end up staying compliant without last-minute chaos. Whereas, those that rely fully on external consultants without internal reviews often discover mistakes only after a notice from MCA lands in the inbox.

Annual Income Tax Compliance for Private Limited Companies

Income tax compliance isn’t something that a private limited company can afford to overlook, not even in the early growth years, and yet, it’s one of the most misunderstood areas of corporate governance. The focus often stays on ROC filings, while tax requirements are pushed till the last moment, or worse, left to an external CA who doesn’t always follow up unless asked.

What’s often missed is that tax obligations go beyond just filing an income tax return for a private limited company once a year. They include advance tax calculations, TDS responsibilities, audits, and keeping the numbers aligned with what’s filed under MCA. And when there’s a mismatch? Notices follow.

Even companies with no major revenue or active operations are still legally required to comply with tax laws, but many directors think that no profit means no filing, which is wrong. Tax laws and Companies Act annual filing obligations are separate, and both must be followed.

Key Tax Compliances Every Private Limited Company Must Handle

- Filing ITR-6: This is mandatory for all companies except those claiming certain exemptions. Filing must be done regardless of revenue status. Some directors were under the impression that this applies only if GST is applicable, which it isn’t.

- Tax Audit (Section 44AB): Required when annual turnover crosses ₹1 crore (or ₹50 lakh for professional services). A lot of startups miss this when growth happens quickly, as neither are they aware of the threshold, nor do they notice when they’ve crossed the audit threshold.

- Advance Tax Payments: Instalments are due quarterly if the total tax liability exceeds ₹10,000/year. Ignoring this leads to interest under Sections 234B and 234C. And yes, even early-stage companies fall into this if they receive income from rent, services, or capital gains.

- TDS Filings (Forms 24Q, 26Q): TDS must be deducted and filed on time, especially if you pay salaries, rent, or freelance fees. Skipping TDS or filing it late triggers a ₹200/day penalty per return, and often goes unnoticed till a year-end audit.

Common Missteps That Lead to Trouble

- Filing ITR after the ROC forms, without checking if the P&L matches.

- Missing Form 3CD (tax audit report), assuming the CA would “take care of it”

- Delaying advance tax, thinking cash flow is low, it doesn’t matter; tax is based on estimates.

- Not linking TDS payments properly in the books, which causes a mismatch during scrutiny.

Tax Compliance Summary Table

| Compliance Area | Form(s) Involved | Deadline / Frequency | Mistake That Happens Often |

| Income Tax Return | ITR-6 | 31 Oct / 30 Nov | Filed without final audit closure |

| Tax Audit | 3CD, 3CA/3CB | Before ITR filing | Skipped if no profit |

| Advance Tax | Quarterly instalments | 15 Jun, 15 Sep, 15 Dec, 15 Mar | Paid late assuming nil cash flow |

| TDS Returns | 24Q, 26Q | Quarterly | Filed late or not filed at all |

Unlike individual taxation, where a delay is often forgiven with a small fee, corporate delays add up faster and come with larger consequences, and the systems today are automated. Once you’re flagged for a mismatch or non-filing, getting clean again takes months.

The smart way forward? Don’t rely completely on external advisors. Internal tracking of these tax dates, even on a simple spreadsheet, saves a lot of panic later. If something as basic as ROC filing requirements or Companies Act annual filing is mapped, why not tax dates too? Because once a company misses enough deadlines, it’s not just about paying fines, it’s about whether that company looks trustworthy to investors, banks, or regulators.

Statutory Registers and Board Meeting Requirements

There’s a strange tendency among new businesses to treat board meetings like informal catch-ups and statutory registers like just any other spreadsheet. But under the Companies Act, maintaining registers and conducting board meetings isn’t just a formality; it’s a legal requirement, and for a private limited company, these records play a major role in proving corporate governance.

Yet, most founders don’t maintain the proper formats. They either rely on templates downloaded online or leave it entirely to their CA, and that’s where problems begin.

A structured annual compliance checklist for private limited companies must include not just ROC filings, but also how well you’ve documented your board decisions and shareholding changes throughout the year. Because if the Registrar of Companies (ROC) ever asks for records and which they often do, you can’t just give them an Excel file with names.

Statutory Registers Every Private Limited Company Must Maintain

- Register of Members: Must include shareholder names, dates of allotment or transfer, and shareholding structure. Skipping even one entry may invalidate a transaction.

- Register of Directors and KMP: Includes appointment, resignation, and remuneration details. Some firms weren’t updating it when a director resigned last-minute, and that’s a mistake.

- Register of Charges: Needed whenever the company avails loans or creates security against assets. Even short-term unsecured loans sometimes get wrongly excluded.

- Register of Share Transfers: Any transfer must be recorded immediately. Backdating entries or skipping entries due to “internal understanding” isn’t legally accepted.

Board Meeting Requirements Under the Companies Act

- A minimum of four board meetings per year are mandatory for every private limited company. The gap between two meetings should not exceed 120 days.

- Quorum must be maintained as per Section 173 of the Act. Many early-stage companies think one founder can conduct a meeting alone whereas the requirement under law is that, even if other directors are inactive, quorum rules still apply.

- Resolutions passed during board meetings must cover matters like approval of financials, appointment of auditors, signing of returns, and allotment of shares.

- Minutes of each meeting must be prepared and circulated within 15 days. Keeping minutes in WhatsApp screenshots or email chains doesn’t qualify as the statutory requirement.

Common Issues Companies Face

- Minutes prepared but not signed or bound.

- Share transfer entries are done only at year-end, not at the time of the transaction.

- Registers are stored digitally but not in a prescribed physical format.

- No record of quorum or director attendance.

- Decisions taken over the call or message without a formal meeting or documentation.

Quick Table: Register & Meeting Compliance

| Item | Requirement | Frequency / Rule |

| Register of Members | Names, shareholding, allotment dates | Update on every change |

| Register of Charges | Details of all loans secured by company assets | Maintain throughout loan term |

| Board Meetings | Minimum 4 per year, gap ≤ 120 days | Mandatory under Section 173 |

| Board Resolutions | Financials, auditor, returns, key appointments | As needed, recorded in minutes |

| Minutes | Maintain throughout the loan term | Sign & bind in register |

Ignoring these requirements won’t cause issues immediately, but it usually does during due diligence, funding rounds, or a random MCA compliance check, and at that point, reconstructing board minutes or registers retroactively is not just messy but also illegal.

To stay ahead, the Companies Act annual filing should be paired with a disciplined approach to internal documentation. It’s not just about filings, it’s about proof. Proof that decisions were made correctly, by the right people, and at the right time. A clean register and properly recorded board minutes also play a role when you file your income tax return for a private limited company, since all major financial approvals must be traceable.

Other Key Annual Compliances (Depending on Company Type)

While most private limited company owners know about the core filings like MGT-7 and AOC-4, there’s a second layer of compliance that often gets overlooked. These depend on the nature of business, capital structure, outstanding liabilities, and other specific activities during the year.

What makes these dangerous is that they’re not triggered automatically, MCA won’t send you reminders, and neither will your CA unless you’ve asked the right questions. That’s where many companies fall short; they follow the Companies Act annual filing blindly but ignore event-based or type-specific filings that are equally mandatory.

Below is a breakdown of other key annual compliances that form part of a complete annual compliance checklist for private limited companies.

1. GST Annual Return – GSTR-9

- Applicable to companies registered under GST, with a turnover above the audit threshold.

- GSTR-9 is a summary return that consolidates monthly filings and reconciles the year.

- Due date: 31st December of the next financial year.

- Many directors don’t know that even if monthly GSTR-1 and 3B were filed, GSTR-9 is still required.

- Some businesses assume that if turnover is under ₹2 crore, the return is optional. That’s partially true for non-audit cases but depends on notification updates, which must be checked and kept updated each year.

2. MSME Form 1

- Applicable if a company has outstanding payments to MSMEs beyond 45 days.

- Must be filed twice a year, in April and October.

- Even if a company is not registered as an MSME itself, if its vendors are, this form becomes mandatory.

- Many founders think this is only for manufacturing or service MSMEs, but any MSME supplier triggers this obligation.

3. Form BEN-2 – Beneficial Ownership Declaration

- Filed when there is a shareholder who holds 10% or more beneficial interest in the company but is not listed on the register.

- Common in cases where shares are held by another company, trust, or nominee.

- Some companies don’t file BEN-2 because they believe it only applies to foreign shareholders. Whereas, it applies to any structure where the name on record differs from the true owner.

- Not filing BEN-2 can lead to personal penalties for directors, especially in funding or audit scenarios.

4. MBP-1 – Disclosure of Director Interests

- Every director must declare their interest in other companies, partnerships, or directorships.

- Filed in the first board meeting of the financial year, and when there is a change.

- Many directors submit this informally via email, but that’s not valid unless it’s tabled and recorded in board minutes.

- It’s also tied to conflict-of-interest provisions under the Act, which can result in board resolutions being voided if disclosure isn’t proper.

5. DIR-8 – Non-Disqualification Declaration

- Directors must annually confirm that they are not disqualified under Section 164.

- This must be filed internally and recorded during board meetings.

- A lot of companies forget to collect this, assuming that if ROC hasn’t flagged anything, the director is in the clear on compliance.

Other Optional but Recommended Disclosures

- MSME Registration Update – If your company supplies to the government or works under tenders, updated registration helps.

- FEMA Compliance (if foreign shareholding exists) – Reporting to RBI through the SMF portal.

- CARO Applicability Review – For audit firms to determine if additional reporting applies.

- Related Party Transactions Review – Especially if directors are involved in vendor or service arrangements.

Summary Table of Conditional Annual Compliances

| Compliance Item | Applicability | Common Errors |

| GSTR-9 | GST-registered companies | Assumed optional due to small turnover |

| MSME Form 1 | Outstanding dues > 45 days to MSMEs | Not checking vendor MSME registration |

| BEN-2 | Beneficial interest ≠ registered holder | Ignored in group company structures |

| MBP-1 | All directors annually | Done informally or without board noting |

| DIR-8 | All directors annually | Not collected or tabled in meetings |

These compliance items don’t apply to every company, but when they do, skipping them can have long-term consequences. A typical private limited company that deals with investors, third-party contracts, or holds layered ownership must take them seriously. Ignoring them doesn’t just trigger late fees; it signals weak internal controls, which becomes a red flag for investors, banks, or even potential acquirers, especially when income tax returns for a private limited company or ROC filing requirements are being reviewed alongside these records.

A complete statutory compliance checklist for employers in such cases must be customised each year, based on the company’s structure, vendors, and shareholding patterns. Not every compliance will apply, but the ones that do must be done right.

Penalties for Non-Compliance & Common Mistakes

Every private limited company registered under Indian law is required to comply with a variety of statutory and regulatory obligations, and when that doesn’t happen, even unintentionally, the penalties are immediate and often harsh. Many founders don’t realise the extent of the consequences until the notice arrives.

The Companies Act annual filing, ROC filing requirements, and income tax return for a private limited company are only the beginning. It’s the smaller, often ignored filings and disclosures that lead to bigger trouble. What’s worse? Many companies think that if they hire a consultant or CA, the responsibility shifts, whereas the legal obligation still rests with the board and directors.

The MCA doesn’t wait around for intent; it penalises based on action or inaction. Here’s what every director should know.

Major Penalties That Hit Private Limited Companies

- Delay in Filing ROC Forms (MGT-7, AOC-4)

- Penalty: ₹100 per day, per form.

- No upper cap, which means companies that delay 3–6 months end up paying ₹15,000–₹30,000 easily.

- This amount cannot be waived even if the delay was accidental.

- Some assume that if there’s no AGM, there’s no need to file; that’s wrong. The forms must still be submitted, or delayed filing must be explained.

- Failure to Appoint Auditor (Form ADT-1)

- Within 15 days of the AGM, Form ADT-1 must be filed.

- Non-filing can lead to a fine of up to ₹25,000 on the company and every officer.

- In many startups, the CA continues as auditor informally without proper reappointment, which is not valid in the eyes of the law.

- Non-Filing of Income Tax Return

- Penalty of ₹5,000 under Section 234F.

- If tax is payable and the return is not filed, interest under 234A, 234B, and 234C applies.

- Some directors were thinking that NIL income means no filing needed, but every private limited company must file a return annually, regardless of profit or loss.

- TDS Defaults and Late Filings

- ₹200 per day penalty for each return not filed (Form 24Q/26Q).

- Interest of 1%–1.5% per month on late deduction and late deposit.

- Salaries or contractor payments processed without deducting TDS may lead to the entire expense being disallowed during an audit.

- Director Disqualification (Section 164)

- If a company fails to file financial statements or annual returns for three consecutive years, all directors can be disqualified for 5 years.

- Disqualified directors can’t be reappointed in any company during that period.

- Some companies forget to file MGT-7 for two years and learns about disqualification only when they try to file third-year forms.

Other Frequent Mistakes (That Often Go Unnoticed)

- Assuming MCA will send reminders for compliance dates.

- Filing returns without verifying if the board has passed the resolution.

- Submitting documents via email or WhatsApp instead of formal board meetings.

- Using old director DINs without checking their current status.

- Filing GSTR-9 only when asked by the auditor, even if it was due months ago.

- Relying completely on external consultants without internal tracking.

Snapshot of Key Penalties & Triggers

| Non-Compliance Issue | Applicable Penalty or Consequence |

| Delay in ROC Filing (MGT-7, AOC-4) | ₹100/day with no max cap |

| Failure to File ITR | ₹5,000 + interest under Sections 234A/B/C |

| TDS Return Delay | ₹200/day + interest + disallowance of expense |

| Auditor Reappointment Lapse | ₹25,000 penalty + invalid appointment |

| Director Disqualification | 5-year bar under Section 164(2) |

Sample Annual Compliance Calendar (Month-Wise)

Managing the legal calendar for a private limited company is not just about remembering deadlines; it’s about tracking, internal approvals, documentation, and aligning finance with law. The mistake that often happens, especially with startups or smaller firms, is assuming the annual compliance checklist for private limited companies can be followed with a “year-end” mindset, but that doesn’t work as government portals don’t wait. Late penalties stack, director DINs get disabled, and companies find themselves disqualified for next steps like loans or tenders.

And let’s face it, ROC filing requirements, Companies Act annual filing, and income tax return for a private limited company aren’t the only things to tick off. From TDS filings to internal board disclosures, compliance needs to be monitored every month. A month-wise compliance calendar helps avoid last-minute chaos.

Why Month-Wise Compliance Matters

- Reduces last-minute panic during ROC season (Sept–Oct).

- Helps you align accounting with legal filings.

- Avoids interest, late fees, and legal notices.

- Ensures internal board approvals happen on time.

- Prevents oversight on quarterly returns like TDS, GST, or PF/ESI.

| Month | Compliance Item | Form / Requirement |

| April | Start audit prep, board meeting planning | – |

| July–Sept | Hold AGM, file AOC-4, MGT-7 | AOC-4, MGT-7 |

| September | DIR-3 KYC for directors | DIR-3 KYC |

| October | DPT-3, BEN-2 | DPT-3, BEN-2 |

| November | Tax Audit, ITR-6 filing | Form 3CA/3CB, 3CD, ITR-6 |

| December | TDS return, Advance Tax payment | 26Q/24Q, Advance Tax |

| March | Final board meeting, review all registers | Minutes, Registers |

Common Calendar-Related Errors

- Companies forget to conduct board meetings every quarter, even if financials were discussed informally.

- Assuming tax filings are CA’s responsibility and not following up internally.

- Missed Form BEN-2, thinking it’s only for foreign investment.

- DIR-3 KYC not completed, which leads to the DIN getting deactivated.

- Filing TDS returns late just because “nothing major was deducted” still attracts a penalty.

Legal Mistakes That Commonly Go Unnoticed

- Treating AGM as optional – Some companies don’t hold an AGM if all directors agree, which violates Section 96.

- Skipping board resolutions for director salary, share allotment, or bonus, even though the Companies Act mandates board approval for such.

- Maintaining registers in Excel only, whereas these need to be properly bound and signed as per Rule 15 of the Companies (Management and Administration) Rules, 2014.

Practical Tips to Stay Compliant

- Maintain a shared Google Sheet or Excel file with a compliance tracker per month.

- Assign responsibility to one internal SPOC, not just the CA.

- Set calendar reminders for every 10th, 15th, 30th, and last working day.

- Link your accounting software with the GST and TDS dashboard to get real-time alerts.

- Cross-check MCA, IT, and GST compliance statuses every quarter.

Conclusion & Next Steps – Annual Compliance Checklist

Even when penalties are monetary, they bring reputational damage and practical delays, like bank loans getting stuck, investor diligence failing, or credit ratings dropping. The smarter approach is not just filing the forms but tracking them with internal accountability.

Just because the annual compliance checklist for private limited companies is templated, doesn’t mean your approach should be. Each company’s filing calendar, board calendar, and financial cycle is unique, and that’s how compliance must be managed.

Missed dates, wrong assumptions, and complete reliance on consultants are the usual culprits. But unfortunately, intent doesn’t matter much in compliance; proof of action is everything.

Compliance may seem like a back-office routine, but for any private limited company, it’s the spine of long-term growth and legal credibility. The minute it gets ignored or worse, outsourced blindly, directors put their company and themselves in risky waters. From Companies Act annual filing to even simpler things like TDS return or DIR-8 collection, missing one deadline can pull the entire board into regulatory default.

What’s often misunderstood is that annual compliance isn’t a fixed checklist. It varies each year depending on turnover, capital change, shareholding patterns, director activity, and even legal notices. Yet most directors don’t review the previous year’s filings before starting the next cycle. That’s where legal non-compliance creeps in—not because laws changed or amended, but because internal tracking didn’t.

Here’s why a quarterly compliance mindset helps – Annual Compliance Checklist

- MCA updates forms and portal requirements almost every 3–6 months.

- Vendor and employee contracts may trigger a statutory compliance checklist for the employer’s requirements.

- New board members or equity changes affect ROC filing requirements.

- Income tax return for a private limited company requires audit data that builds over quarters, not at year-end.

What should directors be doing proactively – Annual Compliance Checklist

- Create an internal compliance tracker that breaks down all monthly, quarterly, and annual filings.

- Meet with your CA or legal team every quarter, not just in March or July.

- Ensure resolutions are documented properly, not just sent by WhatsApp or signed digitally without discussion.

- Review your master data on the MCA site, check DIN status, KYC, PAN updates, and authorised capital figures.

- Maintain board minutes, financials, and statutory registers in bound form, not just in Google Drive.

Common Mistakes You Can Still Avoid – Annual Compliance Checklist

- Filing MGT-7 without actually conducting an AGM—yes, this happens, and it’s a serious violation.

- Thinking, Form AOC-4 isn’t needed if the company made losses—it’s still required, even for dormant companies.

- Assuming ROC filing requirements apply only to active companies—companies with no turnover are still required to file.

- Not linking auditor reappointment (ADT-1) with AGM minutes and filings.

- Treating the income tax return for a private limited company like an individual return, ignoring audit triggers or Section 44AB applicability.

But what if mistakes have already happened? – Annual Compliance Checklist

It’s fixable if you act fast.

Late filings can still be regularised. MCA allows for condonation of delay under certain conditions. You can also file compounding applications under Section 441 to reduce the penal impact. But these must be planned, not delayed further.

Many founders believed that if a notice hadn’t arrived, things were fine. But the new MCA portal is integrated with PAN, DIN, GST, and IT systems, so you won’t always receive an email. Whereas, you’ll see the consequences when your DIN is blocked, or when a bank asks for compliance records before approving a loan.

Read another article: Maternity Leave in India: Legal Rights and Protections for Working Women

Final Checklist (Before You Log Out of This Page) – Annual Compliance Checklist

- All MGT-7, AOC-4, and ADT-1 forms filed?

- MSME Form I filed for dues pending over 45 days?

- GST Annual Return (GSTR-9) filed, even for NIL turnover?

- DIR-3 KYC and DIN status checked?

- Statutory compliance checklist for employers up to date?

- Annual compliance checklist for private limited companies reviewed with the board?