Reviewed and Validated by: Richa Thakur, Associate

Introduction: Understanding Gratuity and How to Calculate Gratuity Correctly

Every salaried employee must understand every detail associated with Gratuity to ensure that they get or receive the financial benefit they are entitled to upon resignation, retirement, or in layoff situations. Gratuity is a one-time payment that an employer makes to its employees as a token of appreciation for the employee’s long-term service. However, most employees aren’t aware if they are eligible for gratuity, how it is calculated, the tax implications and so on.

Gratuity (Mandatory Payment of Gratuity Act, 1972) is regulated by the Payment of Gratuity Act, 1972 – it is a statutory requirement in India, for employees in any organization (with at least 10 employees) who have rendered a minimum of five years of continuous service. The gratuity calculation formula is often not known, and some may not even be aware if their employer follows the mandatory gratuity guidelines.

In this guide, we’re going to cover everything you need to know about how to calculate gratuity, including:

- Gratuity Calculation Formula under the Payment of Gratuity Act, 1972.

- Eligibility criteria regarding gratuity and exclusions

- Step-by-step examples of gratuity calculation

- Tax implications, and ways to maximize tax benefits

- How to claim gratuity, and what to do if your employer does not pay you gratuity.

This article hence will give you clarity on how gratuity works in India and how you can claim the full gratuity amount should you be eligible.

What is Gratuity? A Retirement Benefit Employees Should Know About

Gratuity is a lump-sum payment provided by the employer to the employee for continuous service of at least five years. It forms an employee’s retirement benefits and is not deducted from salary, wholly payable by the employer. It is one such retirement benefit that every employee needs to know about.

Key Features of Gratuity:

- Mandatory for organizations with 10 or more employees under the Payment of Gratuity Act, of 1972.

- It is paid out when you resign, retire, or are terminated, except in case of misconduct.

- Gratuity is automatically given to government employees, while it has to be claimed by a private-sector employee.

- Tax exemptions up to Rs. 20 Lakhs are available under Section 10(10) of the Income Tax Act for private-sector employees.

- The gratuity is paid if an employee dies, or if he is disabled (even if he does not have five years of service).

Who is Eligible for Gratuity in India?

Many employees are confused and have questions about their eligibility and whether their employer needs to pay gratuity. Here are the main eligibility requirements you should know about:

Eligibility Criteria for Gratuity:

- The employee should have worked for the same employer for a minimum period of five continuous years.

- The employer must have at least 10 employees on at least one day in the previous 12 months.

- Gratuity is payable when employees are resigning, retiring, or being discharged (involuntarily, no firing for misconduct).

- Gratuity is paid to the nominee or legal heirs if an employee dies or becomes permanently disabled even before completing five years of service.

Mandatory gratuity is specified under UAE law and applies to employees who range between the 5-year and 10-year window of service with the employer.

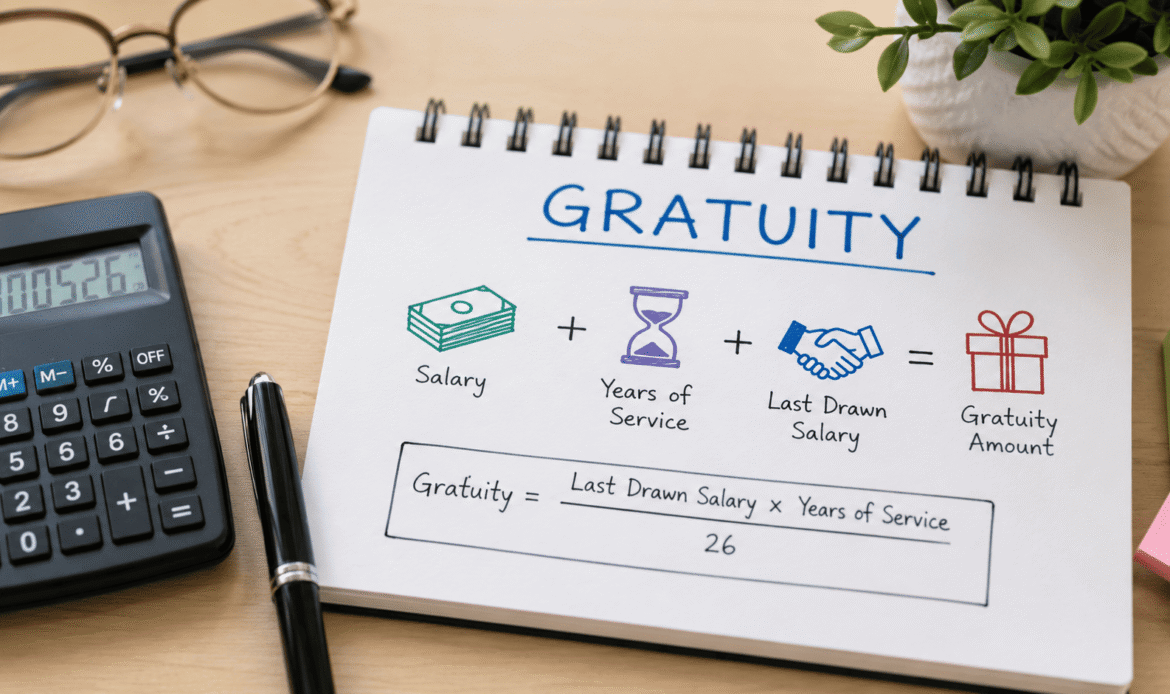

How to Calculate Gratuity? The Correct Formula Explained

The formula for calculating gratuity differs for employees who are covered and employees who are not covered under the Payment of Gratuity Act, of 1972.

Gratuity = (Last Drawn Salary×15×Number of Years Worked)/26

Formula to Calculate Gratuity for Those Covered Under the Act

Gratuity=(Last Drawn Salary×15×Number of Years Worked)/30

Breaking Down the Formula Parts:

- Last drawn salary = Basic salary + Dearness Allowance (DA)

- 15 Days Salary = (Last Drawn Salary/26(for covered employees) or 30(for non-covered employees) *15

- Num Years Worked = Rounded to the nearest whole year.

Example of Gratuity Calculation

| Employee Name | Last Drawn Salary (₹) | Years of Service | Gratuity Formula | Gratuity Amount (₹) |

| Rajesh | 50,000 | 10 | (50,000 × 15 × 10) ÷ 26 | ₹2,88,461 |

| Priya | 75,000 | 15 | (75,000 × 15 × 15) ÷ 26 | ₹6,49,038 |

This gratuity amount can increase by quite a bit if the salary components include extra years of service, additional benefits such as bonuses and higher allowances.

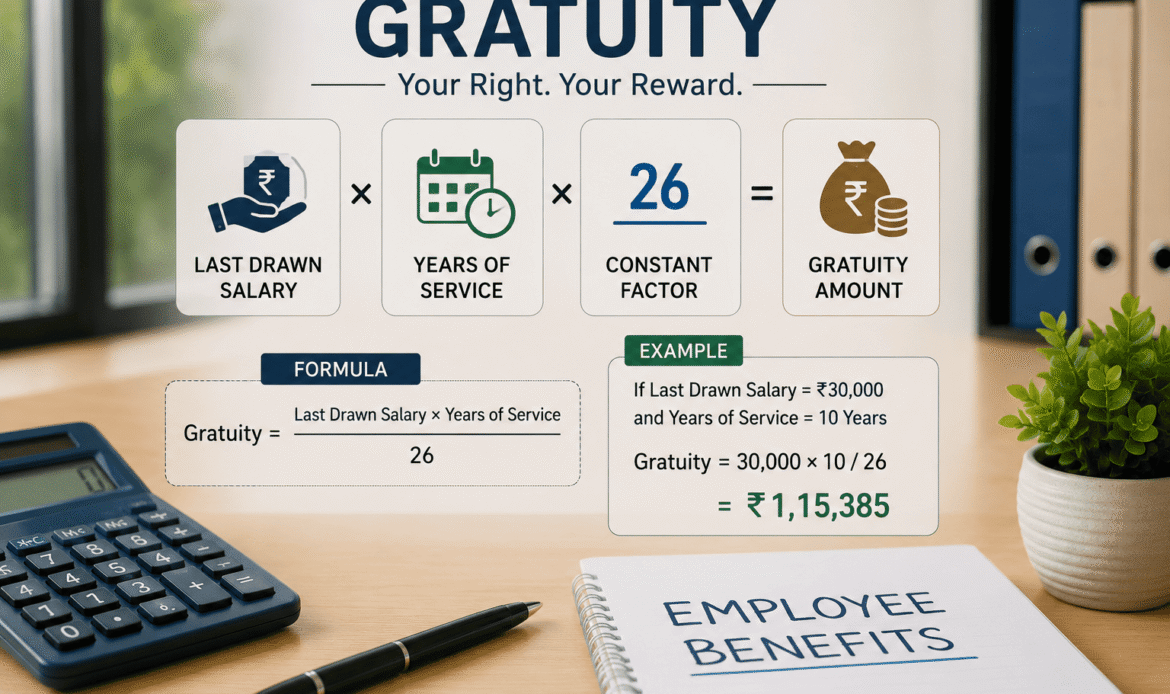

How to Calculate Gratuity in India?

Here is the formula for Gratuity in India:

Gratuity = (Last Drawn Salary × 15 × Number of Years Worked) / 26

Last Drawn Salary (Basic + Dearness Allowance) and service years would be accounted for in whole years. The limit for tax-free gratuity is the highest ₹20 lakhs for private-sector employees under Section 10(10) of the Income Tax Act.

How to Calculate Gratuity for Different Salary Slabs?

For gratuity calculation in India, you can use this formula:

Gratuity= (Last Drawn Salary×15×Number of Years Worked)/26.

Example calculations for different salary slabs:

| Salary Slab | Years Worked | Gratuity Amount (₹) | |

| ₹30,000 | 10 | ₹1,73,076 | |

| ₹50,000 | 15 | ₹4,32,692 | |

| ₹75,000 | 20 | ₹8,65,384 |

Structuring the salary to maximize the Basic+DA component can help increase gratuity benefits.

Tax Implications on Gratuity in India

One of the important parts of an employee’s financial security is Gratuity. While gratuity is tax-exempt, any excess amount over and above the tax-free limit is largely taxed according to an individual’s income tax slab.

Tax Exemption for Government Employees

As per the Income Tax Act, of 1961, Section 10(10) implies that Gratuity is fully exempt from tax for government workers. This implies that employees employed by the central government, state government, defense services, railways, and local authorities are exempt from tax on the gratuity amount received.

Tax Rules for Private Sector Employees

For employees in the private sector, gratuity received up to Rs. 20 Lakhs is tax-free under section 10 (10) of the Income Tax Act. If gratuity is received for multiple jobs in a career, the exemption will apply collectively.

Any gratuity amount exceeding ₹20 lakhs is added to the employee’s taxable income and taxed according to the applicable income tax slab.

How Gratuity is Taxed for Amounts Exceeding the Exemption Limit?

When a private-sector employee receives gratuity, and if the amount is more than ₹20 lakhs, the excess amount is included in the total taxable income of the employee and it is taxed at the applicable income tax slab of the employee.

For example:

| Gratuity Received (₹) | Tax-Free Amount (₹) | Taxable Amount (₹) | Tax Rate (%) |

| 18,00,000 | 18,00,000 | 0 | 0% |

| 22,00,000 | 20,00,000 | 2,00,000 | As per slab |

| 30,00,000 | 20,00,000 | 10,00,000 | As per slab |

So, if his or her gratuity calculation comes down to ₹10 lakhs, and the employee falls under the 30% bracket, they would need to pay ₹3 lakhs as an income tax on the excess amount.

How to Calculate Gratuity for Taxable Gratuity Amount

Formula for taxable gratuity amount:

Taxable Gratuity=Total Gratuity Received−Tax-exempt Gratuity (₹20,00,000 for private employees)

Example Calculation:

- Gratuity = ₹25,00,000

- Tax-free limit = ₹20,00,000

- Taxable gratuity = ₹25,00,000 − ₹20,00,000 = ₹5,00,000

- If the employee is in a 30% tax slab, tax payable = ₹5,00,000 × 30% = ₹1,50,000

How to Tax Planning Tips for Employees

- Exit at the right time — If you are planning to retire or resign, you can strategize the timing of your resignation so that you can maximize your tax-free gratuity benefits.

- Leverage Section 89 -If gratuity has been received for previous years of service, then exemptions under Section 89 of the Income Tax Act should be availed.

- Consult a Tax Professional – If the gratuity amount exceeds Rs. 20 lakh, advice from Tax Experts would help in exploring ways to minimize the tax burden through exemptions and financial planning.

Gratuity for Different Types of Employees

The gratuity rules are different depending on the type of employment, and eligibility conditions. Here is a category-wise breakdown of gratuity:

Gratuity Calculator for Private Sector Employees

- Private sector employees in companies with 10 or more employees are entitled to gratuity under the Payment of Gratuity Act, 1972. Ex gratia is tax-free for up to ₹20 lakhs.

- The formula for the calculation of gratuity would remain as mentioned in the Act.

- Employees need to satisfy the criteria of being in service for at least five years, other than in death or disability scenarios.

Gratuity for Central and State Government Employees

- Full tax exemption for Central, State, and local government employees.

- Based on the last drawn salary & years of service.

- Tax-free up to a maximum gratuity amount applicable under government regulations.

- Gratuity is given automatically to government employees on retirement and no separate claim is to be filed.

Gratuity for Contractual Employees

As for contractual employees, gratuity shall be paid based on the period of their continuous service under the same employer for five years.

- A contractual worker is eligible for gratuity if they work directly for a company for five years or more.

- If that contract is done exclusively through a third party to hire someone to work for the company, then the gratuity responsibility belongs to the contractor, not the company.

Read another article: How to Draft a Data Privacy Policy for your Business (With Checklist)

Gratuity for Self-Employed Professionals (Does It Exist?)

- Hence, self-employed professionals such as freelancers, consultants, gig workers, etc., are unable to earn gratuity as this statute only applies to employer-employee relationships.

How to Claim Gratuity?

Most workers are unaware of gratuity claim procedures and the necessary methods to follow to get paid. Here’s a step-by-step on how to claim gratuity and what to do if an employer refuses to pay.

What Employees Need to Know: A Step-by-Step Guide

- Submit Form I: The employee fills and submits Form I to his employer requesting him for the payment of gratuity.

- Validation by the Employer: The employer checks the claim and calculates the gratuity amount payable.

- Gratuity Payment: The gratuity has to be paid within 30 days of the claim’s approval by the employer.

- Tax Calculation: The tax-exempt portion will be calculated by the employer, and tax on the excess amount will be deducted as per the income tax slabs.

- Payment Method: Gratuity is normally paid through bank transfer or cheque.

Forms to Submit for Gratuity Claim

1. Form I – Application for Gratuity by an Employee

- File after resigning, retiring, or being terminated by the employer.

- Requires experience letter including last drawn salary, tenure of service, and reason for leaving.

2. Form J – Gratuity Claim by Nominee

- In case of an employee’s death, who can claim the gratuity?

3. Form K – Gratuity Claim by Legal Heirs

- Filed when an employee dies without naming a nominee.

4. Form L – Employer’s Notice to Employee

- Employer is Issued Form with Specified Details of Gratuity and Approval or Rejection.

Timeline for Employer Response (30 Days Rule)

Under the Payment of Gratuity Act, 1972:

- The employer is required to approve and pay gratuity within 30 days of receiving the claim.

- If the payment is delayed beyond 30 days, the employer is liable to pay interest on the gratuity amount

What to Do If an Employer Refuses to Pay Gratuity? (Legal Remedies)

If an employer refuses to pay gratuity or withholds it for more than 30 days, employees have the right to take legal action:

- Send formal Notice of Claim for Gratuity

- Submit a written letter requesting the employee to demand the gratuity.

- Employers have 15 days to respond.

- Complain with the labour commissioner

- If the employer is not responding, the employee can lodge a grievance with the Labour Commissioner.

- The Labour Commissioner has the authority to order gratuity payments along with interest.

- Visit the Gratuity Controlling Authority

- If the issue continues, then the employees can escalate the case to the regional Gratuity Controlling Authority.

- Take Legal Action in Court

- If the Gratuity is still not paid, the employee can file a case in the Labour Court.

- If the court rules in favor of the employee, the employer must pay gratuity with interest and penalties.

FAQs About How to Calculate Gratuity

1. Can my employer refuse to pay gratuity?

No. Under the Payment of Gratuity Act, of 1972, an employer can deny gratuity only if the employee is terminated for proven misconduct such as fraud, theft or violence.

2. How is gratuity taxable in India?

For private-sector employees, gratuity is tax-free up to ₹20 lakhs. Any amount exceeding Rs. 20 lakhs is taxed according to the employee’s income tax slab under the Income Tax Act, 1961.

3. What if the employee dies before completing five years?

In the case of an employee’s death, gratuity is also paid to the nominee/legal heirs even if the five-year duration condition is not fulfilled.

4. What if I quit before finishing 5 years? Do I still get gratuity?

No, employees must complete five years of continuous service to qualify for gratuity. However there are exceptions if an employee is dying or has become permanently disabled as a result of an accident or illness. In such situations, gratuity is given to the employee or their nominees even if the employee has not served the minimum period of work. There may be employers who voluntarily pay a gratuity before the five years are over, but this is discretionary.

5. Is gratuity compulsory for all employers?

Yes, under the Payment of Gratuity Act, of 1972, gratuity is mandatory for all organizations with 10 or more employees. If an employer is covered under the Act, even if the number of employees drops below 10, they are liable to pay Gratuity. Gratuity is not an optional payment that the employer can decide to refuse to an eligible employee. If an employer fails to pay gratuity to an eligible employee, it is grounds for legal action.

6. How is gratuity taxed in India?

Government employees enjoy complete tax-free provision under Section 10(10) of the Income Tax Act, 1961. For private sector employees, gratuity is tax-free up to ₹20 lakhs and any amount above the limit is taxable as per the employee’s income tax slab. The lifetime tax-free limit for gratuity remains ₹20 lakhs for the entire career of an employee, even if he gets gratuity from multiple jobs.

7. How do I increase my gratuity amount legally?

Employees who wish to increase their gratuity payout can do so legally by negotiating a higher basic salary (since gratuity is calculated on Basic Pay + Dearness Allowance). Also, if an employee stays longer with the same employer, the employee’s gratuity amount will be higher.

Employees can also choose employers with a voluntary gratuity beyond the statutory limit or participate in corporate gratuity insurance plans, which provide a one-time bonus upon retirement.

8. Can Employers Deny Gratuity to Employees?

No, if an employee meets the eligibility criteria, an employer cannot refuse to pay gratuity. The only exceptions where gratuity can be denied are cases where an employee is terminated for misconduct, including fraud, theft, or violence at work. However, if an employer refuses gratuity without valid justification, the employee has a right to file a complaint with the Labour Commissioner against the employer.

9. Are contractual employees eligible for gratuity?

Yes, contractual employees are eligible for gratuity, provided that they have worked for the same establishment for five or more years. On the other hand, if a contract worker is hired through a third-party agency, the responsibility to pay gratuity lies with the contractor, not the company where the employee worked. Employees need to check if their contract provides gratuity benefits before joining an organization.

10. How to claim gratuity from an employer?

Employees can claim gratuity by following this step-by-step process:

- An employee is required to file Form I, which is a request for gratuity payment to be filed with the employer to claim gratuity.

- The employer then checks the claim, calculates the gratuity amount, and has to pay it within 30 days of approval.

In case the employer does not process gratuity within 30 days, they must pay the employer interest on the amount due. In case an employer refuses to pay any gratuity to the employee, the employee can file a complaint with the Labour Commissioner for legal action.

Conclusion: Why know how to calculate Gratuity?

Every employee should be aware of how to calculate gratuity to ensure they can receive the correct payout when they leave their job. Unfortunately, many employees miss out on their gratuity as they are not aware of their rights. Understanding the right gratuity calculation formula, eligibility, and tax exemptions can help employees better plan their financial future.

If you’re planning to resign or retire soon, calculate your gratuity payout in advance to ensure the maximum possible amount permitted under Indian law.