Reviewed and Validated by: Srijan Jha, Associate

Introduction – Close a Private Limited Company in India

Starting a company is exciting, but not all journeys go as planned. To close a private limited company in India isn’t just a matter of stopping work; there’s an entire legal process tied to it. Many founders think they can just shut shop and walk away, but that’s exactly where the problem starts. Unclosed companies can attract penalties, director disqualifications, and even notices from tax departments years later.

There are multiple legal ways to close a private limited company, and which one applies depends on your situation. If the company hasn’t been operational for a while, you may be eligible for a strike off under the Companies Act. But if there are pending liabilities or if creditors are involved, the process leans towards voluntary company closure in India or, in rare cases, winding up of a private limited company in India via a tribunal.

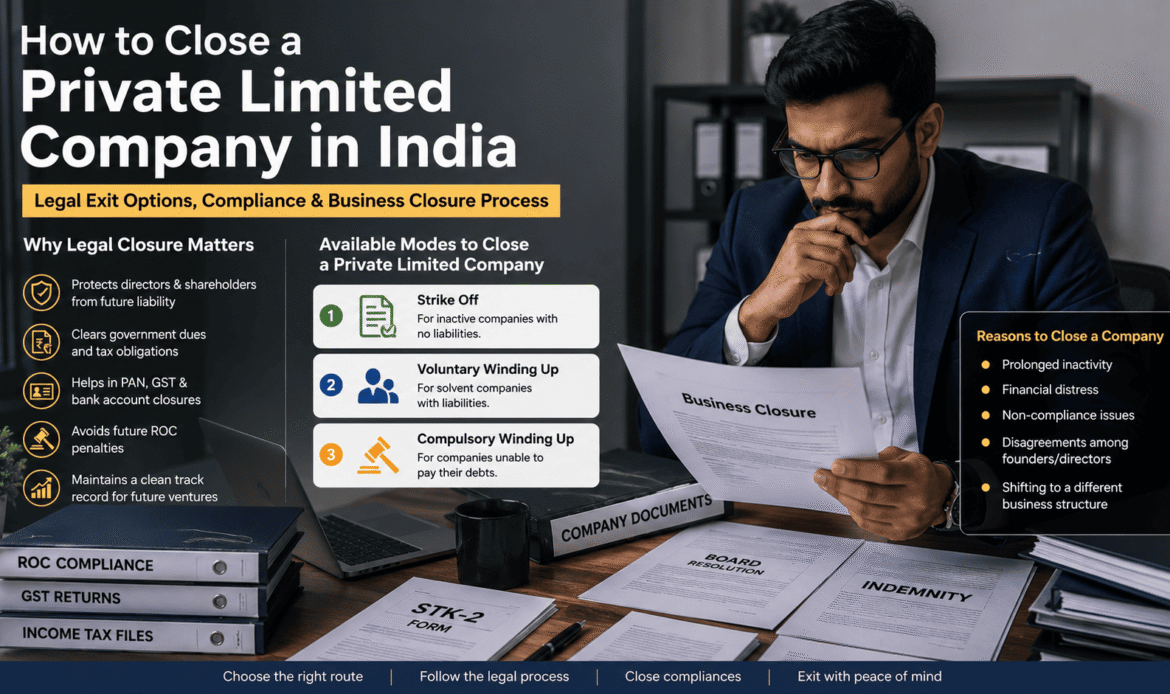

Here’s why legal closure matters:

- Keeps the directors and shareholders safe from future liability

- Clears up any government dues and tax obligations

- Helps in PAN, GST, and bank account closures

- Avoids future ROC penalties

- Maintains a clean track record for your next venture

It’s honestly not too hard, but if you don’t do it right, you might land in trouble. A lot of business owners miss the deadlines, file the wrong forms, or forget to cancel GST before applying. These small errors can delay the closure for months.

So, before you move on to something new, let’s walk through exactly how to do a proper private limited company closure process, with timelines, documents, and real examples. Because when you’re closing a business, the last thing you want is a mess following you around later.

Understanding the Reasons for close a Private Limited Company in India

No business owner starts out thinking they’ll have to shut things down. But the reality is, even the most well-planned ventures sometimes reach a point where it just makes sense to close. In India, the reasons behind shutting down a business are surprisingly common, but still, many people don’t really talk about them enough.

Some of the major reasons businesses decide to close a private limited company in India include:

- Prolonged inactivity: The company hasn’t had any operations or transactions for over a year.

- Financial distress: The Business is no longer profitable or cannot sustain its expenses.

- Non-compliance issues: Repeated defaults in ROC filings, audits, tax dues, or penalties.

- Disagreements among founders or directors: Internal disputes that can’t be resolved.

- Shifting to a different model or entity: Founders may want to move to LLPs or partnerships for lower compliance.

These situations are not uncommon, but unfortunately, a lot of business owners simply leave the company dormant instead of going through the proper private limited company closure process, which creates problems for the business owners later.

Why? Because a company that’s not closed properly still shows as “active” in the Ministry of Corporate Affairs records. That means:

- The company continues to attract compliance obligations.

- Directors may be marked non-compliant and disqualified from other companies.

- It becomes impossible to legally exit without penalties.

One of the most ignored mistakes is assuming that just because the business has stopped, everything else stops too. But the legal identity of a company doesn’t go away unless it’s formally wound up or struck off under the Companies Act, or you go for voluntary company closure in India.

Choosing not to act creates legal clutter and even reputational harm. In short, before deciding how to close a private limited company in India, business owners must first understand why it’s necessary and why simply ignoring it isn’t an option.

Read another article: Annual Compliance Checklist for Private Limited Companies in India

Available Modes to Close a Private Limited Company in India

If you’re planning to close a private limited company in India, you can’t just pick any method and file a form. The Companies Act, 2013 gives multiple routes to do this, and each has its own conditions and paperwork. Choosing the wrong method, or worse, using templates without understanding the rules, can lead to delays, rejection, or penalties.

Here are the three legally recognised ways to shut down a company:

1. Strike Off Under Section 248 of the Companies Act, 2013

This is the fastest and most widely used route, but it only works for certain types of companies. A company can apply for a strike off under the Companies Act if it has:

- No business activity for at least 2 financial years.

- Cleared all dues, liabilities, and filings.

- Closed its bank accounts.

- Taken approvals from all shareholders and directors.

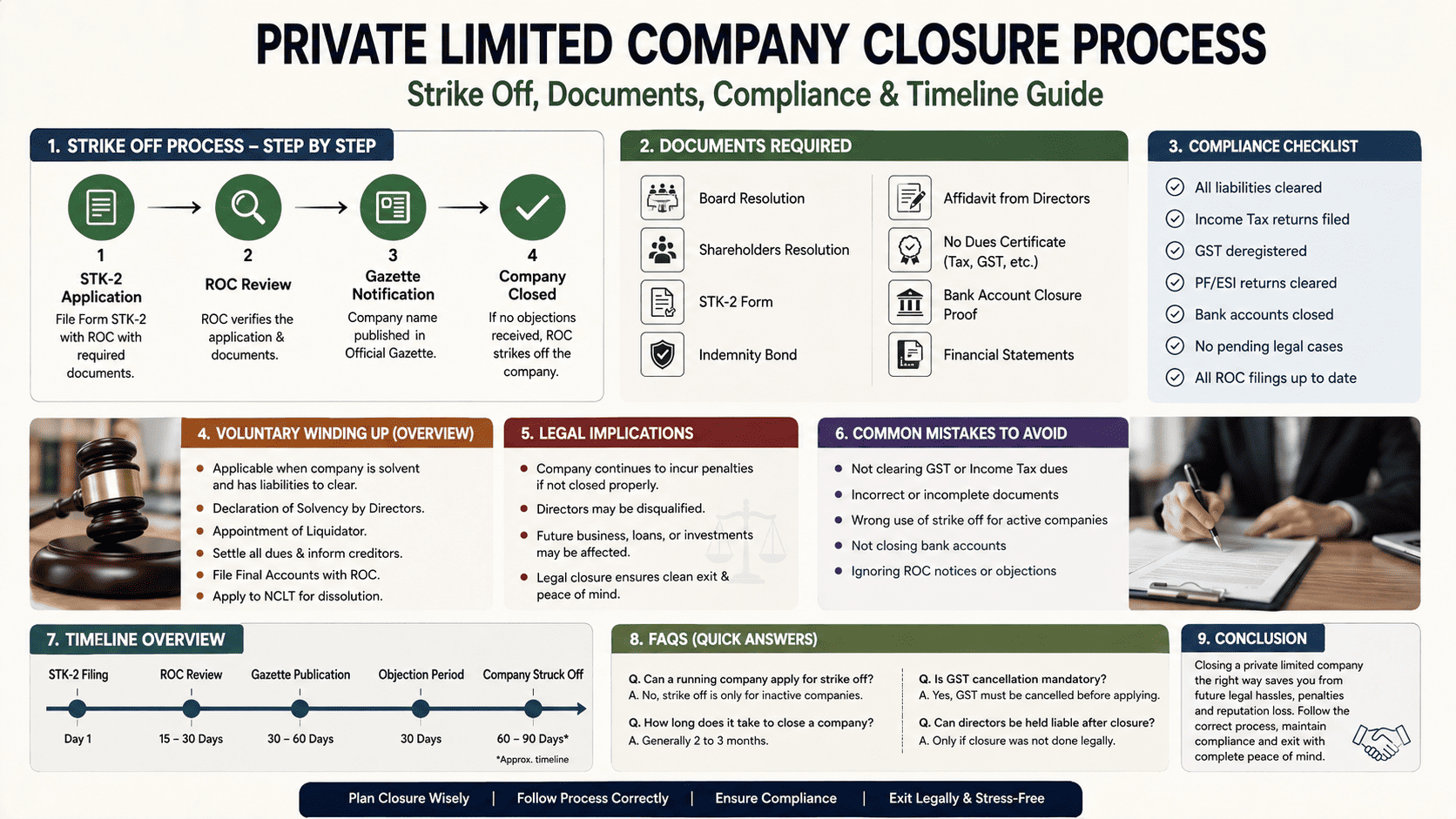

The company must file Form STK-2 with the Registrar of Companies (ROC), supported by documents like board resolution, indemnity bond, director affidavits, and financial statements.

Quick Table: Strike-Off Snapshot

| Criteria | Requirement |

| Company Status | Inactive for at least 2 years |

| Liabilities | Must be fully cleared |

| Director Approval | Unanimous or majority board consent |

| Documents Required | Affidavits, indemnity bond, resolutions |

| Form to File | STK-2 |

This method is ideal for startups or SMEs that are dormant and wish to legally exit without the complexities of winding up of private limited company in India through the courts.

2. Voluntary Winding Up

When a company is still operational or has liabilities that must be paid off, and the directors/shareholders agree to close, this route applies.

Conditions:

- The company is solvent (can pay its dues).

- A declaration of solvency is filed.

- A liquidator is appointed.

- Creditors are notified.

- ROC is updated with the final accounts.

While this process is detailed and a bit time-consuming, it’s necessary when the company has assets, employees, creditors, or complex accounts. The final closure is submitted to NCLT, and post-approval, ROC files the dissolution. Founders often ignore this route, thinking it’s too much work, but it protects you legally if funds are involved.

3. Compulsory Winding Up by Tribunal

This is the last-resort method and is initiated by a stakeholder, like a creditor, ROC, or the Central Government.

Situations where this applies:

- The company has acted against the interests of the state or the public.

- Fraud, mismanagement, or serious non-compliance is discovered.

- The company has defaulted continuously.

- It’s unable to pay creditors or resolve internal disputes.

The Tribunal (NCLT) appoints an official liquidator, and the court monitors the entire process. This path is time-consuming and involves a lot of hearings and submissions. It’s best avoided unless necessary.

Choosing the Right Route

When deciding on your private limited company closure process, ask these key questions:

- Is the company active or inactive?

- Are there pending dues or liabilities?

- Are shareholders/directors aligned?

- Is there any government investigation or case pending?

If the answer is no to liabilities, no operations, and no disputes, a strike-off is often your best bet. But if things are more complicated, voluntary company closure in India or legal winding up may be needed.

Strike Off Process – Step-by-Step Guide

If your company hasn’t operated in the past 1–2 years and meets the right conditions, the best route to close a private limited company in India is through the process of strike off under the Companies Act. This method is straightforward but still legal-heavy. Many businesses get confused during filing or miss key forms, leading to rejection from the Registrar of Companies (ROC).

Here’s a full walk-through so you don’t end up making unnecessary errors.

1. Hold a Board Meeting and Pass a Board Resolution

First, a board meeting must be convened with all directors. During the meeting, the board must:

- Approve the intent to close the company.

- Authorise a director to initiate the private limited company closure process.

- Fix a date for the shareholders’ meeting to pass the special resolution.

One of the common errors is not minuting this properly or skipping notice timelines.

2. Hold General Meeting and Pass Special Resolution

Once the board has approved, shareholders must pass a special resolution to approve the strike-off. This needs:

- At least 75% of voting power in favour.

- A certified copy of the resolution is to be filed in Form MGT-14 within 30 days.

If the company has creditors, the company must also take their NOC, else the ROC may reject the STK-2 application.

3. Filing of STK-2 Form with ROC

This is the main form under Section 248 for strike-off. The authorised director (usually the one who signed board resolution) will file Form STK-2 along with mandatory attachments.

Required Documents:

- Indemnity Bond (in stamp paper)

- Affidavit by all directors

- Statement of accounts (not older than 30 days)

- Shareholders’ resolution

- Copy of PAN, bank closure letter, etc.

Table: Key Document Checklist

| Document | Notes |

| Indemnity Bond (Form STK-2) | Must be notarised; signed by all directors |

| Affidavits from Directors | Stamp paper, notarised, and dated |

| Statement of Accounts | Audited by CA; not older than 30 days |

| Board & Shareholder Resolution | Attach certified true copies |

| PAN & Address Proof | Company PAN and cancelled cheque required |

4. Authentication & Digital Signatures

All directors must have active DSCs (Digital Signature Certificates) to file STK-2. Often, people forget to renew expired DSCs, which delays everything. If any director is abroad, their affidavit and bond must be notarised by Indian embassy or consulate, that step is often missed.

5. Government Fee Payment

The government fee for STK-2 filing is ₹10,000 and additional costs may include notary, CA certification, and legal drafts. Ensure you keep challans and acknowledgment slips safe.

6. Timeline & Approval

Once filed, ROC takes about 45 to 90 days to approve and publish the name of the company in the Official Gazette. If objections are raised (say, due to pending filings), the applicant must respond within 30 days.

Common Mistakes to Avoid During Strike-Off

- Filing STK-2 without MGT-14, or vice versa.

- Submitting outdated or unaudited financials.

- Director not having a valid DSC.

- Ignoring PAN and GST deactivation.

These small oversights can delay closure by months, or worse, get your application rejected.

If you follow the above steps carefully, the private limited company closure process becomes less daunting. In fact, for most inactive firms, this is the cleanest exit available, saving you from years of compliance and ROC penalty traps.

Full List of Documents Required for Strike Off

When it comes to executing the private limited company closure process, the documentation plays a huge role. One wrong form, one unsigned affidavit or missing notarisation and your strike off under Companies Act filing could be rejected right away by the Registrar of Companies (ROC).

To close a private limited company in India under Section 248, you’ll need to gather several specific documents that prove your company is inactive, compliant, and not trying to escape from obligations. These forms are not optional. They’re all mandatory.

Many founders assumes that just the STK-2 is enough and that’s not true. You’ll need to prepare all of the following:

Table: List of Documents for STK-2 Filing

| Document | Description |

| Indemnity Bond (STK-3) | Signed by all directors on ₹200 stamp paper, notarised |

| Affidavit by Directors (STK-4) | States company has no dues; on stamp paper and notarised |

| Statement of Accounts | Must be certified by a Chartered Accountant; not older than 30 days |

| Board Resolution | Approves strike-off and nominates authorised signatory |

| Special Resolution | Passed in general meeting with 75% approval |

| PAN, Aadhaar of Directors | Required as identity and address proofs |

| Consent Letter from Creditors | If applicable, in writing from all creditors agreeing to closure |

| Bank Account Closure Letter | Confirmation from bank that the business account has been closed |

| Latest ITR Acknowledgement | Last filed Income Tax Return, if any |

Additional Notes and Common Errors

- One common mistake is using outdated templates for affidavits and not customising them with company details.

- Some forget to notarise the indemnity bond, or use e-signature instead of actual ink signature, which ROC doesn’t accept.

- ROC expects these forms in PDF format with correct naming structure, wrongly named files are sometimes just ignored.

- If your company had GST registration, a cancellation certificate must also be attached.

Important Legal Conditions for Each Document

Let’s break down some legal nuances founders should not overlook:

- Affidavit and Indemnity: Every active director must sign. If someone has resigned recently, but was a director during the inactive period, they also must sign.

- Statement of Accounts: It must mention nil assets, nil liabilities. Even ₹1 pending can raise a flag.

- Consent from Creditors: If your company took any loan, even from friends or family and hasn’t closed it officially, their NOC is required.

- Bank Account Letter: Soft closure (inactive status) isn’t enough. The account should be formally closed, and proof must be attached.

How Many Copies?

- You’ll need 1 original + 1 scanned copy of each form.

- All notarised documents should be scanned in color (black & white scans often get rejected).

- Keep both soft and hard copies for future reference in case of ROC queries.

In summary, the documents required for strike off are not just checkboxes, they are proof that your company is not trying to escape liabilities or hide compliance. Failing to attach even one document can result in months of delay. If you want your strike off under Companies Act to go smooth, this list must be treated seriously, not just something to fill and upload fast.

Voluntary Winding Up – Process & Compliance

When business partners mutually decide they’re not going to continue anymore, and everything is settled clearly, voluntary winding up becomes the most transparent way to close a private limited company in India. It’s more structured than a strike off under Companies Act, but also more costly and time-consuming. Still, it’s often the preferred choice when you want to exit with compliance in order and have assets or liabilities on record.

Many people don’t understand that voluntary winding up is a legal process under Insolvency and Bankruptcy Code (IBC), not just a Companies Act provision.

Let’s break down the main stages:

Step-by-Step Process

- Board Meeting: A resolution must be passed approving the decision to wind up voluntarily.

- Declaration of Solvency: All directors must file a statement (verified by an affidavit) that the company can repay debts within 12 months.

- Appointment of Liquidator: A licensed insolvency professional is appointed to manage the winding-up process.

- Creditors’ Meeting: If the company owes any money, a meeting with creditors must be held. If 2/3rd in value agree, process can proceed.

- ROC Filings: Forms such as GNL-2, MGT-14, and after liquidation, STK-2 (if applicable) must be submitted.

- Reporting to NCLT: Final accounts and reports by the liquidator are filed with the National Company Law Tribunal.

- Dissolution Order: Once NCLT is satisfied, it issues an official order for the company’s dissolution.

Key Compliance Points

| Compliance Requirement | Details |

| Liquidator Appointment | Must be an IBBI registered professional |

| Solvency Declaration | Verified affidavit + latest audited balance sheet |

| Creditors’ Approval | Necessary if company has outstanding liabilities |

| ROC Forms | GNL-2 (Declaration), MGT-14 (Board Resolutions), STK (if going for strike-off post winding up) |

| NCLT Report | Includes final accounts, statement of closure, assets-liquidation info |

Time and Cost Overview

- Timeframe: Approx. 6 to 12 months, depending on complexity.

- Cost: Liquidator fees, legal assistance, filing fees, and publication charges may cost from ₹80,000 to ₹2,00,000+.

- If the company has no assets/liabilities, winding up under IBC can be avoided, and direct strike-off may be cheaper and faster.

Mistakes to Avoid in Voluntary Winding Up

- Forgetting to appoint a registered liquidator (not just any CA or CS).

- Submitting solvency declaration without affidavit, which will be rejected.

- Confusing voluntary winding up with company strike off, they follow totally different paths.

- Failing to hold creditors’ meeting, assuming it’s not needed (even if no dues, minutes must still be filed).

Legal & Financial Implications of Company Closure

The decision to close a private limited company in India doesn’t just end with filing some forms. There’s a big legal and financial aftermath, most people don’t prepare for that part, and that’s where problems begin. A shutdown might feel like the end, but for the government and financial systems, it’s actually a new round of checks, closures, and clearances.

Let’s break down what that looks like in practice.

1. Impact on Directors

Once the private limited company closure process begins, it directly affects the Directors’ Identification Numbers (DINs). Although your DIN doesn’t expire, ROC can flag your profile if your company didn’t comply with final return filings. A non-compliant DIN can:

- Prevent you from becoming director in another company.

- Attract penalties if ROC filings aren’t cleared.

- Result in disqualification under Section 164 of Companies Act.

Some directors don’t know this and end up surprised when trying to start another venture.

2. PAN, GST & Bank Account Closures

- The company’s Permanent Account Number (PAN) becomes inactive only when ROC marks the company as dissolved and you can’t just ignore it.

- For GST surrender, a final GSTR-10 must be filed within 3 months after surrender request. Many people miss this step and face penalties even after closure.

- Bank accounts must be closed formally. If not, they can still be charged maintenance fees, and bounced cheques may hurt director credit score.

3. Creditor & Employee Settlement

- If you go for voluntary company closure India, all creditor dues need to be cleared first.

- Even in strike-off, you’ll need to confirm via affidavit that no liabilities are outstanding.

- Forgetting to issue full & final payments or employee benefits can lead to labour complaints even post closure.

Here’s where many compliance issues happen. Owners assumes that informal settlements are enough. Whereas, every settlement must be documented.

4. Common Compliance Mistakes After Closure

| Mistake | Consequence |

| Ignoring GST or Income Tax filings for final period | Penalties + notice from departments |

| Not informing utility vendors or lease parties | Continued charges despite shutdown |

| Not archiving accounting and HR records | Legal issue if employee raises dispute later |

| Confusing strike-off and winding-up implications | Wrong route is equal to rejection from ROC or NCLT |

Mistakes to Avoid During Closure

It’s funny how everyone thinks that closing a company is just a formality, like submit one form, maybe a few signatures, and boom, all done. But that’s not how it works, especially when you’re trying to close a Private Limited Company in India under the legal framework. It’s honestly more frustrating than launching one sometimes.

Now, the Private Limited Company closure process looks simple on paper, but most founders, especially first-timers, mess it up in at least one or two steps, and not because they’re careless, but because they just don’t know the practical stuff, like what ROC actually expects, or how late filings create a paper trail you didn’t mean to leave.

Let me walk you through some of the real-world mistakes I’ve seen way too often:

Skipping mandatory filings because “no transactions” happened

- Just because your company didn’t do any business doesn’t mean you’re off the hook. You still need to file returns and annual forms.

- Many teams assume nil activity means no filing and this mistake brings penalties from both MCA and Income Tax, and it delays the company strike off under Companies Act.

Using outdated board resolutions or affidavits

- Another common issue is using templates from 2020 with missing DIN numbers or old director names.

- ROC rejects it immediately, and nobody bothers to tell you what’s wrong. You’re just stuck reapplying.

Not clearing statutory dues before closure

- Closure won’t be processed if you’ve got pending dues under TDS, PF, or GST.

- And GST final return (GSTR-10) is mandatory as forgetting it means the winding up of Private Limited Company in India could take forever.

Treating voluntary closure like just a checklist

- Some firms start the voluntary company closure process in India but forget the basics like closing the company’s bank account, or cancelling the PAN.

- You might think it’s closed, but technically? You’re still on the radar.

Real-World Table: Mistakes & Their Impact

| Mistake Type | Impact |

| Forgot GSTR-10 | ₹10,000+ fine, GSTIN stays active |

| Used wrong affidavit | Application rejected, rework needed |

| Didn’t clear EPF dues | Closure stuck until settlement |

| Strike-off without board meeting | Legally invalid closure |

| Left PAN active | Tax dept may still send notices |

People often confuse strike-off with winding up, these are not the same. One is governed by Section 248 (faster, if you qualify), while the other goes to NCLT and is a longer, messier process.

Another weird thing people do is they upload the documents, assuming ROC will handle it, and then forget that it exists, that’s not how it works. No updates, no email, no news for months, and then one day, you check MCA portal and your company is still listed as “active”.

How Long Does It Take to Close a Company in India?

One of the most common questions businesses ask is, “How long does it actually take to close a company in India?” The simple answer is it depends. Whereas the longer answer? Well, that depends too. Let’s break it down in a real-world way, without all the sugar-coating.

When you’re trying to close a Private Limited Company in India, there are typically two legal routes, strike off or voluntary winding up. Each of them has a very different timeline, and most people don’t realise that upfront.

Strike Off under Section 248

The strike off method is used when a company is not carrying on any business and wants to shut down fast. Here’s the thing though, it may look fast on paper, but ROC and MCA delays often turn that 3-month promise into a 6–9 month wait.

- First, directors must pass a board resolution and file STK-2 with attachments.

- Then comes the waiting game, MCA examines the documents and if everything’s good (and that’s a big “if”), they’ll issue a notice under STK-7.

- Public has 30 days to raise objections, and only after that can your company be legally removed.

Even if you’ve done everything right, realistic expectations should be at least 4–6 months before the strike off completes.

Voluntary Winding Up (NCLT Route)

Now, if your company has assets or liabilities, or legal disputes, you’ll need to take the voluntary company closure India route through NCLT. And that is a different challenge altogether.

- The process begins with a special resolution, appointment of a liquidator, and submission to the Tribunal.

- You must notify ROC, income tax, GST, and all creditors.

- Then the Tribunal takes over, and the timeline? That’s anyone’s guess.

In practice, winding up of private limited company India through NCLT can take anywhere from 12 months to 2 years, especially if objections arise or accounts are not in order.

Table: Timeline Comparison

| Process Type | Legal Route | Average Time | Best For |

| Strike Off | Section 248 (MCA) | 4–6 months (can extend) | Dormant or inactive companies |

| Winding Up | Tribunal (NCLT) | 12–24 months (average) | Companies with assets/liabilities |

Mistakes That Slow It Down

Here’s what slows things down and makes even simple closures drag on for months:

- Delays in preparing accurate documents (I mean, some teams still use outdated formats)

- Directors not responding to MCA notices in time

- Filing errors, typos in DINs, mismatched signatures, expired DSCs

- Thinking MCA will send updates (they don’t, as they expect you to keep checking)

And sometimes, it’s just luck. Some ROC offices process faster than others. One time, a Delhi ROC finished a strike off in 3 months. Meanwhile, a Mumbai-based client waited 8 months, even when all documents were perfect. That’s how unpredictable it can be.

FAQs – Close a Private Limited Company in India

1. Is filing a return compulsory before closing a private limited company in India?

Yes, absolutely. You need to file all the ROC returns and I-T returns before anything can be done, even if the company is not running for a long time. Failure to do this can result in the rejection of the strike-off application. Sometimes founders forget about the GST part; also, you need to close that loop as well.

2. How long does it take to close a private limited company?

Well, it varies. In theory, the strike-off under Section 248 Companies Act should take an estimated 3-6 months. But in actual situations, it can get far worse than that, particularly when there’s a gap in the documents or the MCA portal gets jammed mid-process. So yeah, best to plan on some snags.

3. If a company has debts, can it be shut down?

Not really. Voluntary winding up of a company in India is available if the company has no debts or dues. The Registrar can red-flag the application if there are unpaid loans, salaries, or statutory dues. You will either have to negotiate them or go the liquidation route, which takes longer and involves a tribunal.

4. What is the difference between winding up and strike-off?

They’re both methods of shutting down a company, but they’re not the same. Winding up is a formal court-supervised process, generally employed in cases where the company is solvent or bankrupt. Strike-off, however, is a quicker voluntary dissolution for dormant or debt-free companies. Most start-ups opt for the second option, it’s less hassle.

5. Do I need an attorney or professional assistance to close down my business?

Technically, no. You can do it on your own if you’re good with the process. But if we are to be honest, many founders generally hire a Company Secretary or legal counsel to do the job, as the documentation, ROC filings, and follow-ups can become complex. A minor mistake in filing Form STK-2 or failure to attach an affidavit can leave you starting over from scratch.

Conclusion – How to Close a Private Limited Company in India

At the end of the day, choosing to close your Private Limited Company in India doesn’t mean just on up one day and filling out a few forms. It’s about making sure that every step, from resolutions to final returns, is tied up neatly. There is no shortcut, and each time you attempt to cut ahead, you are simply creating more headaches for yourself down the line, not less.

Many directors will take it when they shut operations, that the company is as good as closed. That’s not how it works. If you fail to follow the right closure procedure, the business legally remains in existence, penalties can escalate, notices of compliance can still be registered, and credit ratings are also affected.

If you’re planning for a company strike off under the Companies Act, then just have the compliance in place. No more returns languishing, taxes paid, assets transferred if required. This may sound basic, however, a lot of companies end up doing it after starting the process.

Also, some believe that closure is a formality, but for several stakeholders like shareholders, investors and employees, voluntary company closure in India is a good way to bring closure in a respectful way. It demonstrates the company appreciates proper process and treats legal closure with the same respect as incorporation.

Let’s discuss some last things to keep in mind while planning to close down a private limited company in India:

- Do not start closure when the board resolutions have not been adopted yet.

- See whether there are any outstanding regulatory filings this will make the process grind to a halt.

- Use the correct DSCs (Digital Signature Certificates). Some teams attempt with expired ones before shrieking about MCA website errors.

- Maintain evidence of communication with ROC, particularly if the deadlines drag on.

Through a clean closure, not only can they enjoy peace of mind, but they also can protect themselves from future liabilities or disqualifications. This legal process can seem very slow, but if you document everything and continue to be responsive, you’ll be done before you know it.

In short, don’t rush, read and follow every stage, don’t trust only the consultants and always read the document you have in your hands. There’s no reason to have a lawyer to run a company shutdown, just mind your do’s and dont’s and take care of the little things.