Reviewed and Validated by: Srijan Jha, Associate

A. Introduction

For any entrepreneur building a business in India, one of the earliest legal checkpoints they encounter is the question of GST registration. Whether you’re selling products online, offering digital services, or running a SaaS product, the Goods and Services Tax (GST) framework now governs nearly every kind of business transaction. Startups often hesitate on this front, not due to unwillingness, but due to sheer confusion, and the confusion is understandable. GST can look intimidating at first because of multiple tax rates, return filings, e-invoicing, and state-wise implications. But it doesn’t have to be that way. Once you understand when it applies, what documents are required, and how the process unfolds, GST registration becomes one of the more manageable parts of a startup’s legal journey.

This guide has been written for founders, early-stage operators, finance leads, and anyone trying to figure out what it really means to register for GST in 2025 and beyond. It’s not a tax thesis; it’s a ground-level, founder-friendly roadmap to startup tax compliance in India.

B. What is GST and Why Does It Matter for Startups?

Brief Overview of GST in India

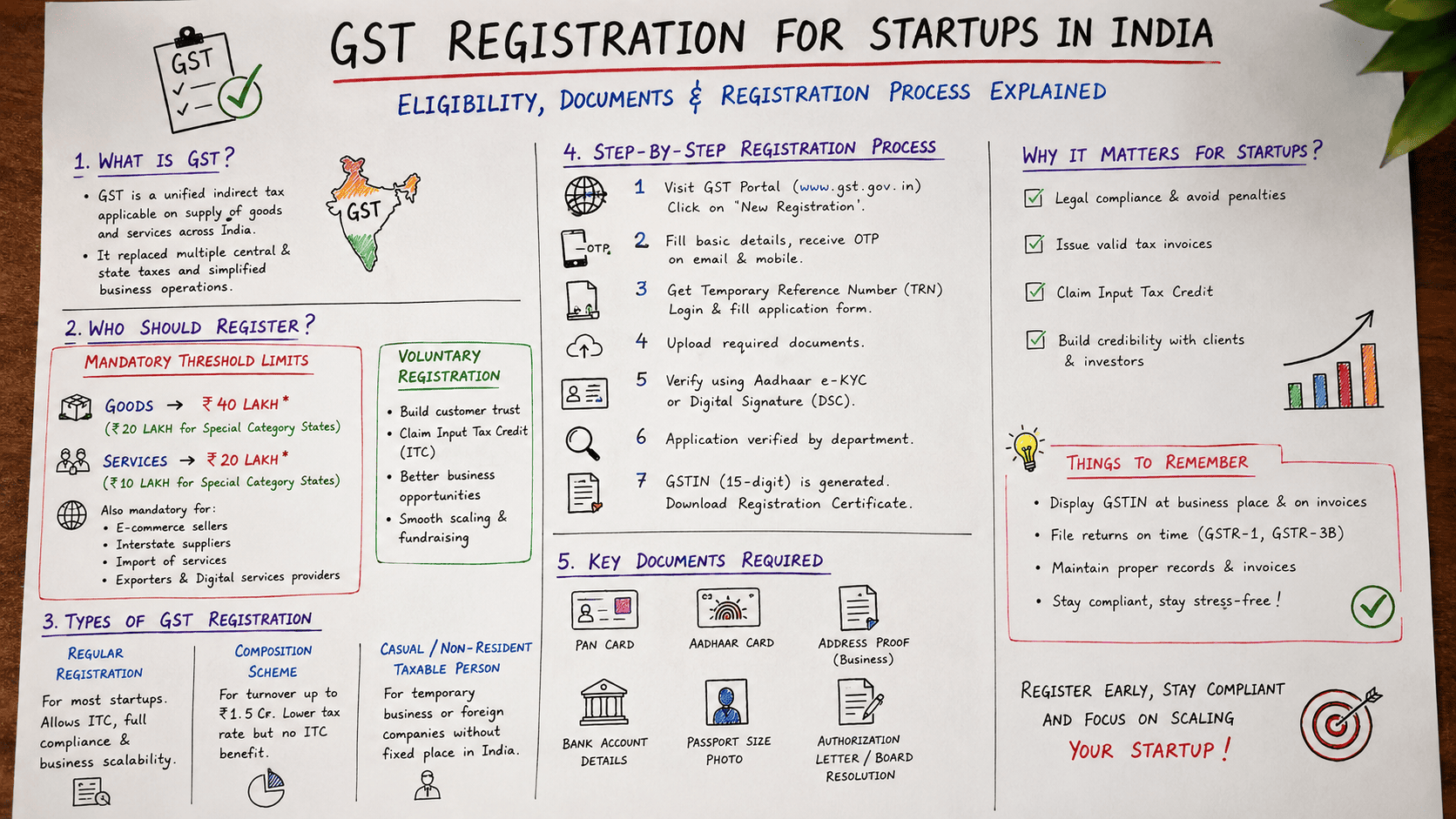

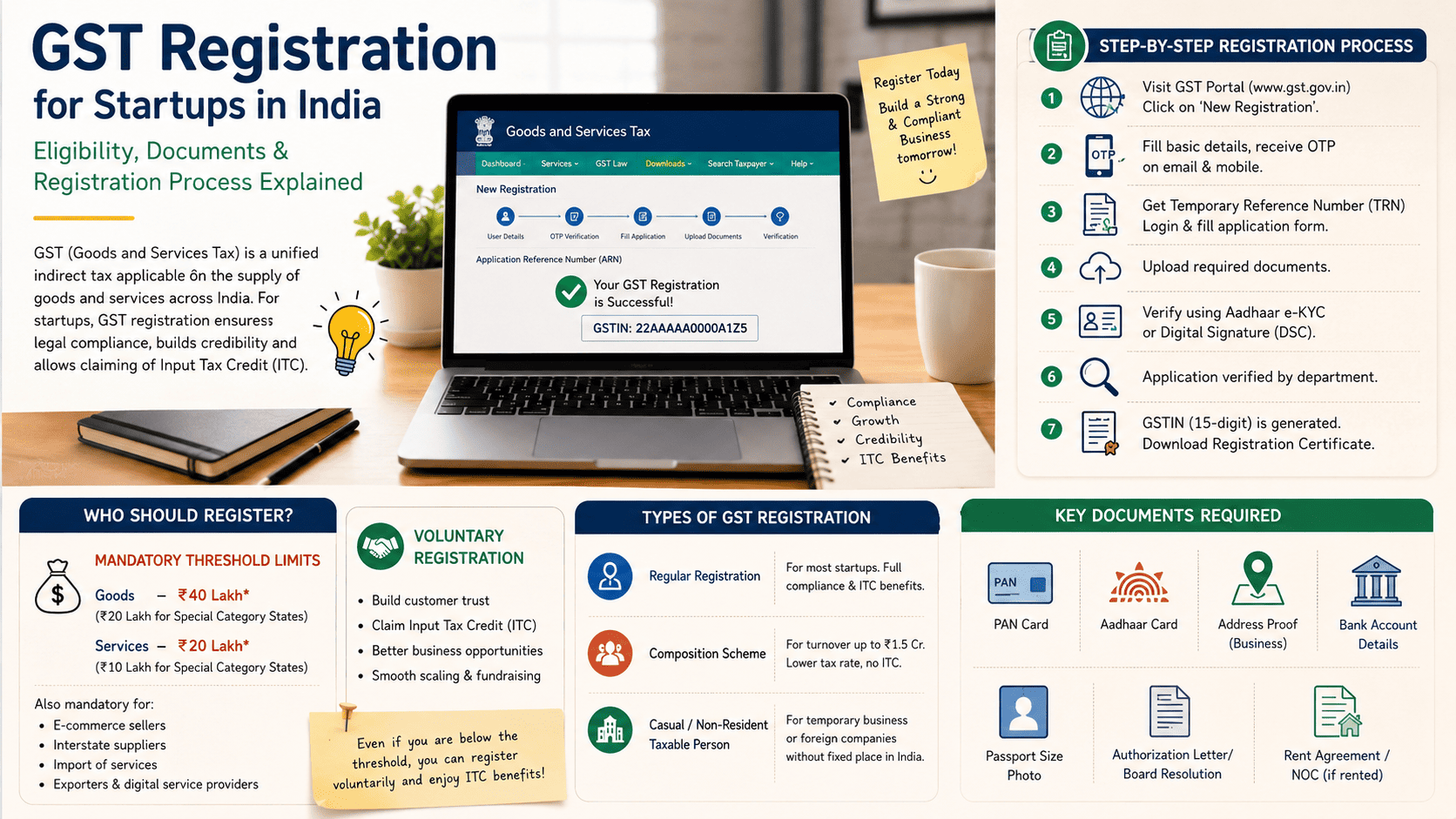

GST, or Goods and Services Tax, is a unified indirect tax that replaced several central and state taxes in India back in July 2017. It covers the supply of goods and services across India and works on a destination-based model. Tax is collected at the point of consumption.

For businesses, GST meant a shift away from older service tax, VAT, and excise laws. Everything got consolidated under one tax regime, with different slabs depending on what you’re selling or offering.

For startups, this had two major consequences:

- First, it simplified interstate operations. You no longer need different VAT registrations for every state.

- Second, it brought with it compliance layers like e-invoicing, HSN codes, and return filings—even if you’re a small SaaS company.

B. Applicability for Startup Businesses

Here’s the thing: GST applies to businesses based on turnover, type of supply, and business model. It’s not just for traditional traders or product sellers. If you’re offering consulting, development, digital services, or SaaS, you may need to register even if your revenues are modest.

Startups offering services outside India (i.e., exports) or working with foreign clients are also subject to GST compliance. You may need to classify your services as ‘zero-rated’ exports and file accordingly. In many cases, GST registration becomes mandatory before you can get paid by larger corporate clients or access government tenders.

Legal Consequences of Ignoring GST Registration

It’s tempting, especially in the early stages, to delay or skip GST. But that comes with risk. If you cross the registration threshold and still don’t register, the authorities may:

- Levy penalties (which can be hefty—up to 100% of tax due);

- Issue a notice for non-compliance;

- Bar you from issuing valid tax invoices (which affects your customers too); or

- Block your ability to claim input tax credit on purchases.

In worst cases, it can affect funding or vendor onboarding. No startup wants a situation where investors ask for compliance proof and you can’t show a GSTIN.

C. Who Should Register for GST?

Mandatory Threshold Limits

As of 2025, the registration threshold for GST varies depending on your business type and where you’re located.

For goods:

- If you’re supplying goods and your aggregate turnover exceeds ₹40 lakhs in a financial year (₹20 lakhs for special category states), you must register.

For services:

- If you provide services and your turnover exceeds ₹20 lakhs (₹10 lakhs in special states), registration is mandatory.

Aggregate turnover includes all taxable, exempt, export, and interstate supplies. It’s not just your taxable revenue. This is important because many startups underestimate their reportable turnover by excluding zero-rated exports or exempt income.

Voluntary Registration

Even if you’re below the threshold, you can register voluntarily. Startups often do this because:

- Clients (especially B2B) prefer dealing with registered vendors;

- You want to claim input tax credit (ITC) on software tools, office supplies, rent, etc., or

- You’re planning to scale or raise funds and want your books clean.

Voluntary registration does bring compliance obligations—but for many startups, it’s a small cost for professional perception and better cash flow management.

Sector-Specific Triggers

There are certain cases where GST registration becomes mandatory irrespective of turnover:

- If you’re selling through e-commerce platforms like Amazon, Flipkart, Shopify (in most cases);

- If you’re offering SaaS or digital services and collect money from outside India;

- If you’re importing services (even things like buying ads on Google or Facebook), or

- If you’re providing interstate services.

So even if your income is below ₹20 lakhs, your business model may push you into the mandatory GST category.

D. Types of GST Registration for Startups

Regular Registration

This is the standard form of registration under GST. It applies to most startups, including those offering SaaS, consulting, tech-enabled services, or selling goods online. With regular registration, you’re expected to:

- Collect GST on your invoices.

- File monthly or quarterly returns;

- Maintain proper records and invoices; and

- Claim input tax credit.

This is the most common route for early-stage and growth-stage startups that want full access to tax credits and plan to scale.

Composition Scheme

The composition scheme is available for small businesses with a turnover below ₹1.5 crore. It allows you to pay GST at a flat rate (usually 1% or 5%) without needing to track ITC or file full returns. But here’s the catch: service providers have limited access to this scheme, and if you’re doing business interstate or online, you’re probably not eligible. Also, you can’t claim input credit under this scheme. For a startup offering services or digital products, composition is rarely the right fit.

Casual & Non-Resident Taxable Person

This category applies to startups that:

- Sell goods or services temporarily in a different state (e.g., pop-ups, exhibitions);

- Operate without a fixed place of business; and

- Are foreign companies operating in India without a physical office?

In these cases, you must register as a Casual or Non-Resident Taxable Person. The registration is valid for a limited time and requires an advance tax payment.

E. Step-by-Step GST Registration Process

Preparing Documents

Before you start the online application, make sure you have the following:

- PAN of the business or proprietor;

- Aadhaar card of directors/founders;

- Address proof of business premises (rent agreement, electricity bill);

- Passport-sized photo of promoters;

- Cancelled cheque or bank account details; and

- Authorization letter or board resolution (for companies).

If you’re using a shared workspace or coworking space, you may need a No Objection Certificate from the lessor.

Online Application on GST Portal

- Visit gst.gov.in and click on ‘New Registration’.

- Select ‘Taxpayer’ and fill in basic details like legal name, email, and mobile number.

- You’ll receive an OTP on both email and mobile — this is used to generate your Temporary Reference Number (TRN).

- Log in using TRN and fill out the remaining application — business details, promoter info, place of business, goods/services supplied, and bank details.

- Upload documents in PDF or JPEG formats as required.

- Submit with Aadhaar e-KYC (if applicable) or via DSC.

Verification and GSTIN Generation

Once submitted, the application is verified by the department. You may be asked for additional documents or clarification. If everything checks out:

- The application is approved within 3–7 working days.

- GSTIN (15-digit GST Identification Number) is issued, and

- You can download the registration certificate from the portal.

Post-registration, you’re expected to display your GSTIN at your place of business and on invoices.

F. Post-Registration Compliance

Getting a GSTIN doesn’t mean the process is over. In fact, that’s where startup GST compliance really begins. Many early-stage founders assume that once they’ve received the registration certificate, there’s nothing more to do unless revenue starts flowing. But the GST framework imposes monthly (or quarterly) obligations regardless of revenue stage.

Let’s walk through the critical items that startups must be aware of post-registration.

GSTIN Display Requirements

Section 25(6) of the CGST Rules requires every registered person to display:

- GSTIN at the entrance of the principal and additional places of business.

- GSTIN on every tax invoice, debit/credit note, and relevant documents.

For those selling online, platforms like Amazon and Flipkart won’t even activate your account unless this is correctly done. Neglecting this step may not lead to penalties right away, but during inspections or site visits, this is one of the first things officers check.

GST Returns Filing Timelines

Once registered, even if your revenue is nil, returns must be filed. The primary returns include:

- GSTR-1: Captures outward supplies (sales); monthly or quarterly.

- GSTR-3B: Summary return of tax payable, ITC claimed, liabilities paid.

Startups under ₹5 crore turnover may opt for the QRMP (Quarterly Return Monthly Payment) scheme. Still, GSTR-3B must be filed monthly or quarterly, depending on the scheme selection. Failure to file on time leads to automatic late fees, ₹50 to ₹200 per day for every continuing day. Even worse, continuous default can lead to suspension or cancellation of the GSTIN.

E-Invoicing (Turnover Threshold)

Startups with turnover crossing ₹5 crore must issue e-invoices:

- Via IRP (Invoice Registration Portal);

- With a valid IRN (Invoice Reference Number), and

- It contains a dynamic QR code (for B2B).

Generating regular invoices without an IRN makes them legally invalid. This is one area where software tools are highly recommended.

Input Tax Credit (ITC) Clauses

Claiming ITC under GST requires compliance not just from you, but from your vendors. Here’s what startups need to do:

- Reconcile monthly GSTR-2B with vendor invoices.

- Track vendor filings, if they miss GSTR-1, your ITC is blocked; and

- Use basic ITC reconciliation tools (even Excel works).

Unclaimed ITC due to vendor defaults leads to real money being lost. So having a basic tracker for ITC claims is not optional anymore; it’s necessary.

Change in Business Particulars

Changes in address, business name, authorised person, or additional place of business must be updated on the GST portal. The timelines are strict:

- Address changes – File amendment within 15 days.

- Addition of a new place – Submit address proof + utility bill.

- Changing business type (e.g., going from partnership to Pvt Ltd) – New registration required.

Startups undergoing a pivot or rebrand should ensure the GSTIN reflects the correct current entity details.

Responding to Notices

Startups sometimes receive notices due to:

- Return mismatches (e.g., GSTR-1 showing ₹1 lakh, GSTR-3B showing ₹0);

- Late filing (even nil returns, if missed, trigger notices); and

- Inactive GSTIN (if multiple filings skipped).

It is advised not to ignore these filings and to ensure filings via the GST portal within the deadline. Keep a consultant looped in if you’re unsure.

GSTR-9 Annual Return

This is currently optional for businesses under ₹2 crore, but mandatory above that. Even if not mandatory, filing shows financial discipline. Startups going through fundraising or due diligence often prefer to file to show transparency.

G. Key Documents Required

When early-stage founders begin working on their GST registration for startups, the process usually seems more digital than it actually is. On paper, yes, the portal is online, and yes, everything is supposed to be scanned and uploaded, but that doesn’t mean the groundwork is any less document-heavy. In fact, one of the biggest delays we’ve seen, time and again, comes from incomplete uploads or tiny mismatches that could’ve been avoided with better prep. So before hitting that “Submit” button on the portal, here’s what should already be sitting in your compliance folder.

Let’s walk through this in parts, based on what kind of business structure your startup follows and the level of registration you’re opting for.

Proof of Legal Existence of the Entity

This one’s foundational. The GST officer needs to confirm that your business exists in legal terms. What you upload depends entirely on your entity type. Here’s a short guide:

- For sole proprietors: the PAN card of the proprietor typically suffices, as there’s no separate legal identity.

- For partnerships: the Partnership Deed and PAN of the firm are mandatory. If it’s a registered partnership, include the registration certificate too.

- For LLPs: submit the Certificate of Incorporation, PAN of LLP, and the LLP Agreement.

- For Private Limited Companies: you’ll need the Certificate of Incorporation, PAN of the company, and optionally, MOA & AOA (some jurisdictions may request this during the GSTIN verification process).

These foundational documents are rarely rejected if properly scanned and uploaded in PDF, but do ensure there’s no mismatch between the legal name and the one you enter on the portal.

KYC of Promoters or Authorised Signatory

GST registration also focuses on who’s behind the business. The idea is to know who’s signing and taking legal accountability.

Keep these ready:

- PAN card and Aadhaar card of the promoter(s);

- A recent passport-size photograph; and

- One additional address proof, like a voter ID, driver’s licence, or passport, especially if Aadhaar shows a different address.

For startups with co-founders based in different cities, note that the primary signatory’s location becomes important. Any KYC mismatch can stall things.

Address Proof of Principal Place of Business

This is the most misunderstood and often rejected document category. The GST department wants to verify that the physical location from where the business will operate actually exists and is verifiable.

Depending on your setup, these are the options:

- If rented: upload the rent agreement + a utility bill (latest) + No Objection Certificate from the owner.

- If owned: a property tax receipt or sale deed works fine.

- For co-working spaces: a lease/licence agreement + letter from provider + utility bill

- For home-based setups: a rent agreement or declaration from a family member if the property is not in the founder’s name

This is where most startup GST compliance queries originate, and in case of doubt, upload two documents instead of one.

Proof of Bank Account

This proves that the business has a functioning account and can transact. For this, any of the following are usually acceptable:

- Cancelled cheque (best if the name is pre-printed);

- First page of passbook (for proprietors); and

- Latest bank statement (showing IFSC, account number).

In a few states, officers have requested letterheads bearing bank details, though not commonly. For early-stage founders, be cautious of using a personal account; if your startup is already incorporated, it’s better to open a current account before filing.

Authentication Method — Aadhaar or DSC?

There are two ways to verify your identity during registration:

- Aadhaar authentication: Quickest route. You’ll get an OTP on the mobile linked to your Aadhaar. Recommended for sole props and partnerships.

- Digital Signature Certificate (DSC): Mandatory for LLPs and companies. Before uploading, make sure the DSC is registered on the GST portal. Unregistered DSCs won’t be recognised.

For companies, failing DSC authentication during submission is a common cause for ARN (Application Reference Number) rejection.

Additional Documents (if applicable)

Depending on business type and state-specific practices, officers may ask for:

- Authorisation Letter or Board Resolution (if someone other than a director is signing);

- Proof of additional place of business, if you list more than one.

- Trade licence (especially in metro cities or state-mandated zones); or

- Declaration for opting out of the Composition Scheme.

These are not always asked up front but are often demanded at the time of review. So it’s better to keep them in the cloud folder alongside the others.

Table: Core GST Documents by Entity Type

| Entity Type | Business Proof | Promoter KYC | Address Proof | Bank Proof | DSC Required | NOC (if Rented) |

| Proprietorship | PAN of proprietor | Yes | Yes | Yes | No | Yes |

| Partnership | Partnership Deed + PAN | Yes | Yes | Yes | No | Yes |

| LLP | COI + PAN + LLP Agrmnt | Yes | Yes | Yes | Yes | Yes |

| Private Ltd Company | COI + PAN | Yes | Yes | Yes | Yes | Yes |

To wrap up, storing these GST documents for startups in a version-controlled Google Drive or Notion doc (with proper naming) will save massive time, not just during registration, but also in future audits and when raising investment.

H. Common Mistakes And How To Avoid Them

No matter how tech-savvy the platform looks, the actual process of GST registration for startups is still riddled with small procedural traps. Founders often misjudge what seems like a simple form fill-up exercise. In reality, some of the biggest delays in early-stage compliance come from very avoidable errors. Below are a few mistakes that keep recurring and how to steer clear.

Using Residential Address Without Clarity

Many founders start from home, and that’s perfectly fine. But if you use a residential address without providing proper supporting proof (like a rent agreement + utility bill), the officer will either reject the application or send a clarification notice.

How to fix it: Even for home-based startups, upload both the rent agreement and a recent utility bill. If it’s your own home, add a self-declaration or property tax receipt.

Submitting Wrong Authorisation Details

A lot of startups file using a junior team member’s Aadhaar or PAN as the signatory, not realising it’s technically incorrect. Under the GST law, only an authorised signatory (director/partner/proprietor) can validate filings.

How to fix it: Always attach a board resolution or letter of authorisation signed by the primary founder if someone else is signing the application. This is especially important for Pvt Ltd and LLP structures.

DSC Registration Issues

One of the most common delays in the GSTIN verification process comes from a mismatch or failure of the Digital Signature Certificate (DSC). Sometimes, the DSC isn’t registered on the GST portal, or it doesn’t match the PAN details uploaded.

How to fix it: Register the DSC on the GST portal before starting the application. Double-check PAN linkage with the DSC token software.

Skipping Bank Proofs or Uploading Wrong Format

Startups sometimes skip uploading a cancelled cheque or upload it in JPG instead of PDF, leading to rejections.

How to fix it: Upload a cancelled cheque in clear PDF format. If your cheque doesn’t show the business name, add the bank’s passbook or statement.

Filing Returns Late Post-Registration

Some founders assume that if no revenue is generated, no return is needed. But under the GST law, once you have a GSTIN, you must file even nil returns. Missing this step incurs daily late fees.

How to fix it: Use a calendar or compliance tracker to file GSTR-3B and GSTR-1 on time. Even if turnover is zero, don’t skip filing.

Not Opting for QRMP When Eligible

If your turnover is below ₹5 crore and you’re eligible for the QRMP (Quarterly Return, Monthly Payment) scheme, not opting in time could mean more frequent compliance than needed.

How to fix it: During registration, select the QRMP scheme if you meet the criteria. It reduces filing frequency while keeping compliance valid.

Summary Table: Mistakes & Corrections

| Common Mistake | Why It Happens | How to Avoid It |

| Residential address without proof | Home-based ops, no rent agreement | Upload rent agreement + utility + NOC/self-declaration |

| Wrong signatory on GST portal | Junior team member files on behalf | Attach authorisation from founder / board resolution |

| DSC mismatch or failure | Unregistered or wrong DSC token | Register DSC before submission, verify PAN-DSC linkage |

| Bank document in incorrect format | Uploaded photo instead of PDF | Use proper bank proof in legible PDF format |

| Missed return filing | No revenue so assumed not needed | File GSTR-1 and 3B even if nil; track deadlines monthly |

| Not choosing QRMP | Lack of awareness | Check eligibility during registration and opt if applicable |

Avoiding these early errors can save startups weeks of delay and prevent notices or suspension of registration. These mistakes are not just clerical; they impact startup GST compliance and must be factored into founder workflows.

I. Sector-Wise Examples For Startups (Saas, D2c, Marketplace, Etc.)

The GST framework looks deceptively standard from a distance. But in real practice, a startup’s sector plays a surprisingly central role in determining what kind of GST compliance work it has to put in from day one. A SaaS platform selling across borders, for instance, faces a completely different set of operational issues compared to a D2C brand selling on Amazon India. The law doesn’t change; the complications do. Let’s consider how different startup categories typically deal with GST and where things tend to go wrong (or get missed altogether) during the early stages.

SaaS Startups (Software as a Service)

A common assumption among SaaS founders is that since their product is cloud-based and intangible, the tax burden should be minimal or easily deferred. But the GST regime doesn’t treat online-only services lightly. The moment the ₹20 lakh threshold is crossed (or ₹10 lakh for special category states), GST registration for startups becomes mandatory. However, most SaaS businesses voluntarily register even earlier. Why? Because they’re spending on tools like AWS, Google Ads, and HubSpot, none of which are usable for input credit unless GST registration is in place.

If you’re billing foreign customers and haven’t filed an LUT (Letter of Undertaking), your invoices are technically taxable under GST, even if the money comes from a US bank account. Without that LUT, you must pay GST and later apply for a refund. This hits early-stage SaaS businesses hard, especially when cash flow is tight. Also, the reverse charge mechanism applies when paying foreign vendors for tools. Ignoring this creates audit risk down the line.

GST documents for startups in SaaS also need to clearly show SAC (Service Accounting Code), often 9983 or its close variant. Many early invoices either miss this or include vague descriptions like “software services”, which complicates filing.

D2C (Direct-to-Consumer Brands)

GST compliance for D2C brands takes a different route. Most founders building D2C brands start selling on marketplaces like Amazon or Flipkart, or through Shopify-powered personal stores. If you list on a marketplace, GST registration becomes non-negotiable, even if your revenue is ₹5,000. That’s because e-commerce aggregators deduct TCS (Tax Collected at Source) and deposit it with the government. To claim that TCS, you need to be GST registered.

Founders often forget that state-level registration matters too. If you’re warehousing in Haryana but incorporated in Maharashtra, you need a Haryana GSTIN. Without it, you’re dispatching interstate goods without registration, which is a red flag in GST audits. Marketplace TCS data doesn’t reconcile well unless this is fixed early.

Another challenge is on the invoicing side. The requirement for dynamic QR codes for B2C invoices applies once you cross ₹5 crore in turnover, but enforcement can begin even earlier in some jurisdictions. D2C businesses that hit scale quickly without the right systems find themselves scrambling to update invoice formats.

Moreover, the refund cycle on input credit (especially for packaging, logistics, and photo shoots) slows down if SKU-level details aren’t clean. This ties directly into the startup GST compliance problem: the backend stack is built for scale, not for audit readiness.

Marketplaces (Aggregator Platforms)

Startups running marketplaces, multi-seller platforms enter a more complex compliance landscape. GST sees them as “e-commerce operators” under Section 52 of the CGST Act. That means they’re responsible for collecting TCS from all seller transactions on the platform, even if those sellers themselves are unregistered. So, the marketplace ends up with a tax deduction obligation on behalf of parties that don’t even have a GSTIN. This creates a structural burden from day one.

Unlike in D2C or SaaS, GSTR-8 becomes a required monthly filing. Many founders discover this late and backfill months of data manually. The GSTN portal does not sync GSTR-8 with GSTR-3B automatically, leading to errors. One client discovered that the mismatch created by forgetting GSTR-8 filings resulted in a ₹60,000 penalty, simply because their accountant wasn’t familiar with marketplace provisions.

Another issue is seller data management. If a seller is later found to be a fake entity or evading tax, the operator (i.e., the startup) could be held partially liable under the anti-evasion rules. That’s why having updated GST documents for startups and their sellers, including PAN, Aadhaar, bank details, and valid GSTIN, is not just best practice, it’s defensive compliance.

B2B Service Platforms (Logistics, Manpower, HR Tech)

Startups offering bundled B2B services face challenges when their model includes both their own services and pass-through costs. For example, a platform that connects businesses with delivery partners or freelancers often collects a gross amount from the client, pays the gig worker, and retains a margin. But unless the invoice is split correctly, with value for service and reimbursements defined, the startup may end up paying GST on the full gross, rather than only on the margin.

Here, the distinction between principal supply and ancillary charges becomes important. Also, some founders don’t realise that if they’re paying foreign vendors for tools like Slack or Asana, they need to account for GST under reverse charge, even if the foreign vendor is not registered.

This category also often gets caught in litigation around classification. If you claim to be a “pure agent”, you need specific contract language with clients, clear documentation, and separate line-item invoicing. Without this, you may not qualify for exemption on reimbursements and may be asked to pay GST on them retroactively.

Startups that neglect this face double taxation later, especially if input credits get denied in audits. Filing obligations here aren’t always about GSTR-1 and 3B; they sometimes include GSTR-6 if input services are redistributed across multiple business units. That nuance is rarely caught by early-stage founders.

EdTech Startups

EdTech founders often start with the assumption that education is tax-exempt, but that’s not always true. GST only exempts services by recognised educational institutions. If your EdTech business is not formally affiliated with a board or university, the services are likely taxable, especially if the content is pre-recorded and paid.

Also, GST applicability for services changes when courses are delivered live versus on-demand. Live sessions with interactivity might be argued as educational, but pre-recorded video bundles are taxed at 18%. We’ve seen multiple startups realise this too late, only after investors request input credit schedules and discover that the startup was neither collecting GST nor recording credits properly.

Exports to overseas students can qualify as a zero-rated supply, but only if you’ve filed an LUT; otherwise, GST applies. So, even when a US student pays for your AI course in INR, without a proper LUT, GST is payable first and refundable later. This causes cash flow disruptions, especially if the refund takes 90+ days.

EdTechs also often deal with freelance teachers, voice artists, or course creators. Reverse charge applies if you’re paying them from abroad. Startup GST compliance here isn’t just about the platform; it’s about every service interaction tied to the course.

Table (Sectoral Risk Snapshot):

| Sector | Risk Trigger | Common Overlooked Compliance |

| SaaS | LUT missing, RCM untracked | Reverse charge on tools like AWS |

| D2C | Multiple warehouse states | State GSTINs, TCS mismatch |

| Marketplace | GSTR-8, Seller TCS reconciliation | Filing gaps, unverified sellers |

| B2B Service | Mixed invoicing | Improper classification |

| EdTech | Course type + foreign payments | No LUT, assuming education exempt |

J. Conclusion

In the early stages of building a startup, there’s always more to do than time allows. Hiring, product, customer feedback, funding, it all feels more urgent than paperwork. That’s probably why many founders treat GST registration for startups as something that can wait until later. But when “later” comes, it often shows up in the form of an onboarding rejection, a missing vendor invoice, or worse, an unexpected penalty. Many first-time founders delay getting a valid GST number, assuming they’re still below the threshold or that it’s something the finance team will take care of once the company grows. But legal and tax systems don’t always wait for growth. The rules under GST, especially for businesses operating across states, or dealing in digital goods and services, kick in much earlier than expected.

Some practical scenarios where GST registration becomes necessary, regardless of revenue stage:

- Selling digital services or software subscriptions across India;

- Listing products on platforms like Amazon or Flipkart;

- Hiring contractors or vendors who require GST invoices;

- Using paid SaaS tools with GST-inclusive expenses;

- Raising investment and undergoing financial due diligence, or

- B2B billing where clients expect input tax visibility.

In each of these cases, the absence of GST registration creates workflow friction. Without it, you can’t issue compliant tax invoices. If you miss out on claiming input tax credit, you lose leverage in vendor relationships and, perhaps most importantly, you create gaps in compliance history that later need to be explained or fixed under pressure.

A few of the long-term benefits of early registration include:

- Clean audit trail from the beginning.

- Better control over tax liabilities and credits;

- Ease of integrating accounting systems and ERPs;

- Smooth onboarding to platforms and payment partners;

- Stronger perception of compliance during investor diligence; and

- Avoidance of retrospective penalties or tax notices.

Startups that handle GST compliance well don’t necessarily have big finance teams. What they usually have is a clear approach to risk management, understanding which processes matter early, and building them into the business before they become liabilities. It’s not about perfection, it’s about preparedness.

For startups operating in India’s regulated business environment, being GST-registered isn’t just optional. It signals that the company is operationally serious, partner-ready, and less likely to hit compliance bottlenecks at scale. Those who wait tend to spend more later, in money, time, and energy, undoing avoidable issues. So while GST might seem like a bureaucratic step, it’s often the difference between operating informally and being taken seriously by vendors, platforms, and investors. If the business touches other states, serves B2B clients, or operates in any digital capacity, it’s probably time to ask: Are we ready for GST? If the answer isn’t a confident yes, it’s time to fix that, because GST registration for Indian startups is no longer a tick box in the checklist; it’s a starting point.