Reviewed and Validated by: Naman Jain, Associate

Introduction

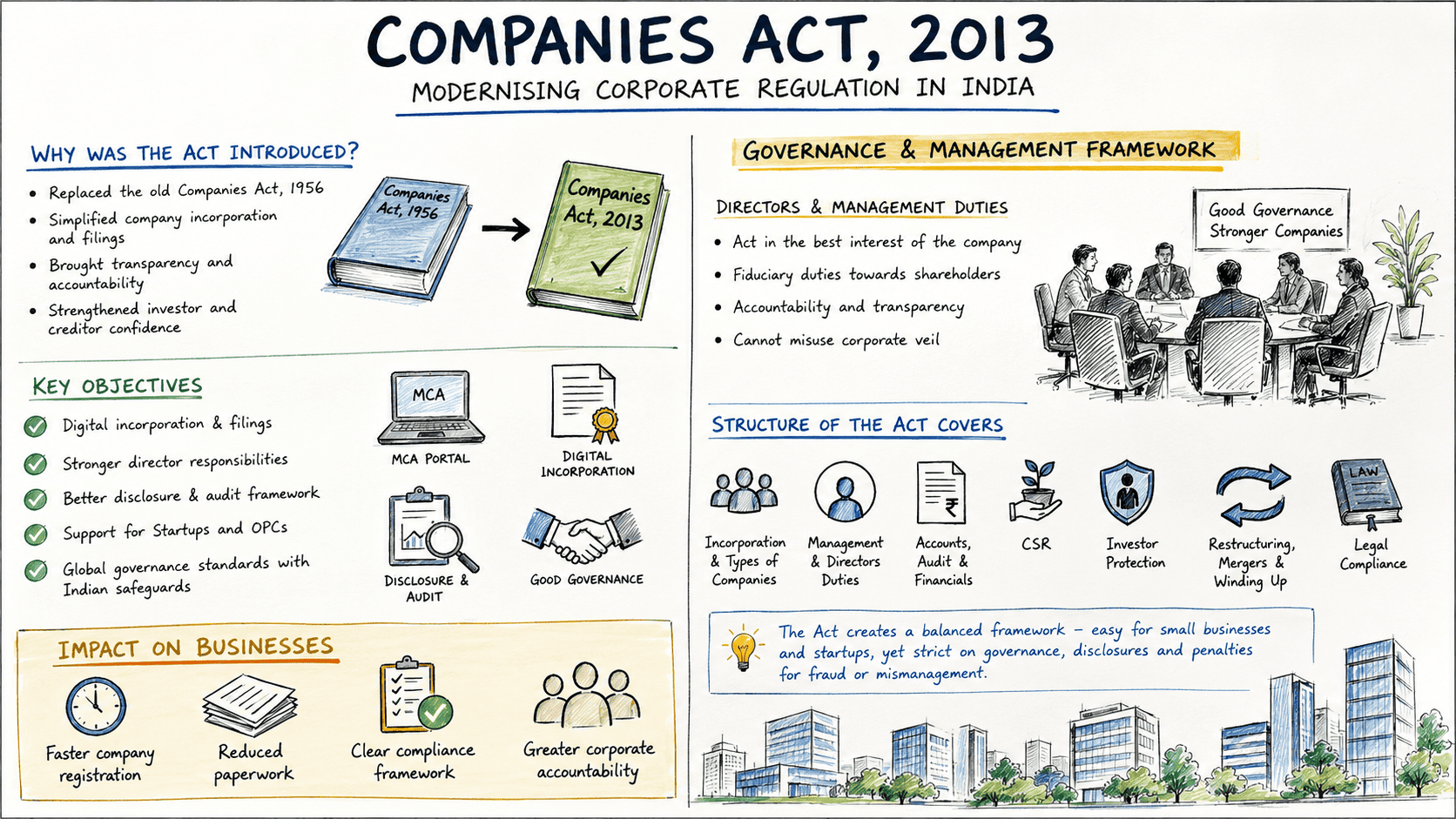

The Companies Act, 2013, read together with amendments up to 2023, is today the backbone of corporate regulation in India. It replaced the old 1956 Act, which had by then become bloated and outdated, and it was drafted with two clear intentions: first, to make life easier for those wanting to set up and run companies, and second, to tighten the responsibilities of those in charge so that investors and creditors were not left unprotected. The amendments over the past decade, including the 2020 and 2023 rounds, reflect how quickly the corporate landscape in India has changed. Start-ups needed lighter compliance; listed companies needed tighter oversight; and investors demanded more transparency. This Act tries to cover all of that. In this Bare Act by Corrida Legal series, the idea is not to replace the law but to give you a way to understand its structure before you dive into the sections themselves.

Purpose and Objectives

Why was the law rewritten? The 1956 framework was no longer keeping up with reality. Incorporation was slow and paper-heavy, directors’ duties were loosely defined, and shareholder protections were not strong enough. The 2013 Act attempted to modernise the entire regime.

Broadly, it tries to:

- simplify incorporation and filings through digital systems,

- bring directors and management under sharper accountability,

- mandate disclosures and audits to give investors confidence,

- encourage small companies and one-person companies with relaxed rules, and

- align Indian corporate governance with international standards while retaining local safeguards.

In practice, what this means is that a promoter today can set up a private company with relative ease, but once incorporated, the board is bound by strict duties, they cannot treat the corporate veil as a shield against personal accountability.

Investor Protection and Compliance

One of the biggest complaints under the 1956 law was that minority shareholders had very little effective protection. The 2013 Act tries to deal with that head-on. Dividends, for instance, cannot be kept hanging indefinitely, if they are declared, they have to be transferred properly, and if they remain unpaid beyond a period, the money goes into the Investor Education and Protection Fund. That mechanism forces companies to either pay what is due or surrender it, rather than quietly sitting on investor money. Raising deposits is another area where misuse was rampant earlier. The Act now places strict controls on who can raise public deposits, how, and with what disclosures. Many promoters still think of this as “borrowing from the public,” but under the new law, it is a regulated activity with penalties for defaults.

The law also deals firmly with fraud and misstatements. If a prospectus contains false information, the liability is not only corporate but also personal, directors and officers can be held to account. The Serious Fraud Investigation Office (SFIO) has been given teeth to investigate major cases, and in recent years it has actually been active. For day-to-day compliance officers, this is the section that keeps them awake, because once fraud or oppression of minority shareholders is alleged, the law moves fast and penalties are severe.

Read another article: The Indian Partnership Act, 1932 – Executive Summary and Bare Act

Mergers, Amalgamations and Winding Up

Restructuring used to be a nightmare under the old regime. Multiple approvals, endless delays. The 2013 Act, read with its amendments, gives a cleaner pathway. There are provisions for fast-track mergers for certain classes of companies, and even cross-border mergers are recognised if regulators are satisfied. The National Company Law Tribunal (NCLT) is the key forum now, it deals with compromises, arrangements and winding up. Winding up can still happen in two ways: voluntarily or by tribunal order. But in both cases, the law insists that creditors and shareholders must be protected. In practice, what this means is that promoters can no longer treat winding up as a casual exit, filings, disclosures and procedures have to be observed, otherwise the tribunal will step in.

Special Provisions

The Act is not just for standard private or public companies. It also recognises producer companies, Nidhis, and even foreign companies that operate in India. Government companies have their own special rules. The compliance requirements differ, but the principle is the same: transparency and accountability. Special courts have been created so that offences can be tried faster. At the same time, recognising that small companies and start-ups cannot be burdened like listed giants, the law provides reduced penalties for them. This balance, strict for serious misconduct, lighter for genuine small-scale businesses, is really at the heart of the reform.

Conclusion

When you step back from the details, the Companies Act, 2013 (with amendments up to 2023) is really the framework within which Indian businesses now live their corporate lives. The old 1956 law had become too bulky and scattered. The 2013 Act, even though far from perfect, created a much clearer skeleton: how companies are born, how they raise

money, what duties fall on directors, and how they eventually restructure or shut down. The later amendments, especially in 2020 and 2023, show the government’s twin priorities. On one hand, it wants to make it easier for small firms, OPCs, start-ups and not-for-profits to comply without being crushed under paperwork. On the other, it does not want to leave investors exposed, which is why governance rules, disclosures, and penalties for fraud or mismanagement have been tightened.

This executive note, as part of the Bare Act by Corrida Legal series, is meant to help professionals, business owners, compliance officers and students get a grasp of the Act without wading through hundreds of sections. It is not a substitute for reading the Bare Act itself, but it makes the contours clearer: incorporation and types of companies, governance and management duties, accounts and audits, CSR, investor protection, restructuring, and special categories.