Reviewed and Validated by: Jefrin Johny, Associate

Introduction

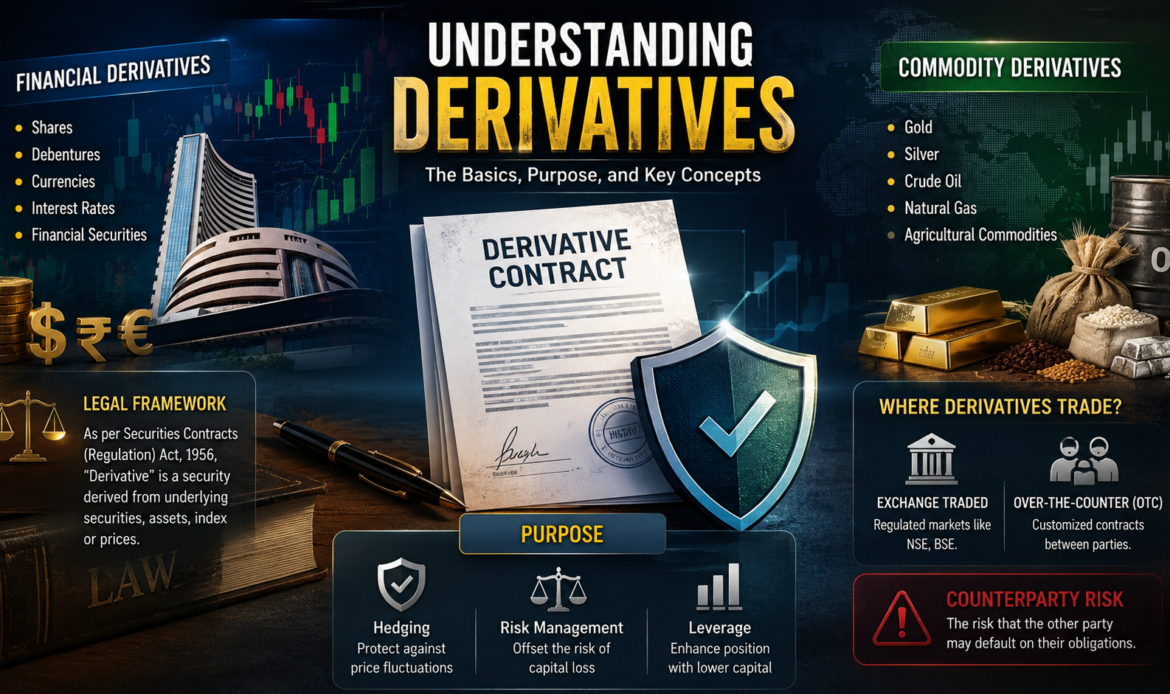

In layman terms, a Derivative based contract is a contract between two or more parties whose value is based on an agreed-upon underlying financial asset, index, or security. Some common financial instruments used for this purpose are Futures Contracts, Forward Contracts, Options Contracts, and Swaps Contracts. These are secondary securities whose value is solely based (derived) on the value of the primary security that they are linked to which is known as the underlying assets.

These underlying assets may be shares, debentures, tangible commodities, currencies, short term or long term financial securities, etc. If the underlying asset is a financial asset, the Derivative is called Financial Derivatives. On the other hand, if the underlying asset is a commodity, such as gold, silver, crude oil, etc., the Derivative is called a Commodity Derivative.

Legally, Clause (ia) of Section 2(h) of Securities Contracts (Regulation) Act, 1956 includes “Derivative” within the meaning of “securities” and section 2(ac) defines “Derivative” as “a security derived from a debt instrument, share, loan, whether secured or unsecured, risk instrument or contract for differences or any other form of security; or a contract which derives its value from the prices, or index of prices, of underlying securities.”

Now, one may ask what is the rationale behind these Derivative Contracts? Simply put, when investments are made in the market, the risk of capital loss always lies through the changes in the market price of investments. Investors need a hedging mechanism to offset the risk of investing in shares and debentures. Derivatives are one way that can help investors in hedging or protect themselves against loss on investment by making balancing or compensating transactions.

Coming to the question of where these Derivatives trade. it may be noted that Derivatives can trade over-the-counter (OTC) or on an exchange. OTC Derivatives contribute to a large share of the Derivatives market. In general OTC-traded Derivatives have a higher possibility of counterparty risk. Counterparty risk refers to the possibility that one of the parties involved in the transaction might default.

Explanation of the different kinds of Derivatives

The following provides a detailed explanation of different kinds of Derivatives along with their working.

Forwards: These are Contracts wherein one party agrees to buy or sell an underlying asset on a future date at a predetermined price with the other party. These Contracts can be traded in two ways, firstly, by buying the forward, as an implication of which the forward buyer agrees to buy the underlying asset at a predetermined price on a future date.

Secondly, by selling the forward, in which the forward seller agrees to sell an underlying asset on a future date at a predetermined price. Forwards generally falls into the category of OTC Derivatives.

For example. A and B are the buyer and seller of crude oil. A approaches B on 1st May 2021, wherein he offers to buy crude oil from B at a future date at a predetermined price. Let’s assume the price of crude oil per unit on 1st May was $100. After negotiations, B agrees to sell crude oil on a Forward Contract at $110 m per unit on 25th June 2021. Here, a Forward Derivative Contract is said to be formed. Now, depending upon the actual price of crude oil per unit on 25th June, it may be the case that one party benefts from the other, or vice versa.

Futures: Forwards and Futures though not the same, but are similar Derivative Contracts. However, Futures were created to offset some of the disadvantages present within Forward Contracts. A Futures Contract has similar characteristics as a Forward Contract, albeit with certain distinctions. Unlike Forwards, which are traded on OTCs, Futures are generally traded on well-regulated exchanges or markets. It does not contain any negotiations and cannot be modified in any way because such Contracts are transacted in a standardized structure format by the exchange facilitating its trading and settlement irrespective of the needs of the parties involved. While Forward Contracts have a lack of regulation, Futures do not bear any counterparty risk due to the intervention of an intermediary such as National Stock Exchange or the Bombay Stock Exchange which ensures the settlement of trades take place through a well-developed legal regime.

An example of a Futures Contract would comprise of two individuals, A and B deciding to form a contract with the underlying asset being the shares of Company X. Let’s assume the prices of shares to be $1000. Person A expects a bearish market and places an order to short one of X’s share at $950, believing that once the prices touch $950 with an expiry of 15 days its price will considerably fall even further. Person B on the other hand expects a bullish market and places an order to long X’s share at $950, with an expiry of 15 days, believing a rise in the share price upon touching the above-mentioned price. Both have thus become counterparts to each other. After the expiry of 15 days, depending on whether the actual price of X’s share is below or above 950, one of the parties will either incur profit or loss depending upon the number of shares purchased.

Options: These are Derivative Contracts that enable the buyer to buy or sell the underlying asset from or to the Option seller at a particular future date (expiry date) at a particular price (strike price). This is similar to Futures Contract but the key difference is that in Options Contracts, the buyer is not obliged to either sell or buy an underlying asset. It is merely an opportunity the Option buyer exercises leverage over the option writer by paying a small amount while purchasing the Option (premium) for purchasing the right rather than the obligation to buy or sell the underlying security as per his discretion. The Options Derivatives are traded at the stock exchange and OTC market.

Options are divided into Call Options and Put Options, these have been described in brief below:

Call Option: This Option vests with the Option buyer with the right to buy an underlying asset from the Option writer at the strike price on the expiry date by paying a premium.

Put Option: This Option vests with the Option buyer with the right to sell an underlying asset from the Option writer at the strike price on the expiry date by paying a premium.

For example, with regards to Call Option, two persons A and B are desirous of trading an underlying asset of the shares of Company X, which is currently valued at $1000. A is bullish on the market and buys a Call Option at Rs.1100 (strike price) believing that the price of X may rise substantially. A (Option buyer) paid a premium of Rs.50 to B (Option writer) at the time of entering the transaction for obtaining the right to buy shares of Company X at Rs.1100 on the expiry date. Now here, A will make a profit or loss on his trade depending on whether the price of the stock at the date of expiry was more or less than the sum of strike price and the premium paid. Similar will occur in the instance of Put Option, except here, A would be bearish of the market and A will encounter profit only if the actual price of the stock is lesser than the sum of strike price and premium.

Swaps: In this Derivative Contract, two parties agree to exchange or swap their cash flows whether incoming or outgoing emanating from a financial instrument. Each cash flow comprises one leg of the swap. One cash flow is generally fixed, while the other is variable and based on a benchmark interest rate, floating currency exchange rate, or index price. While there exist several kinds of Swaps, Interest Swaps are the most common. In Interest Swaps, a fixed interest rate is usually swapped with the interbank offer rate. In India, The Mumbai Interbank Offer Rate is one iteration of India’s interbank rate, which is the rate of interest charged by a bank on a short-term loan to another bank.

An example of this would be Company X and Company Y entering into a one-year interest rate swap with a nominal value of $1 million. offers Y a fixed annual rate of 5% in exchange a rate of the interbank offer rate + 1% since both parties believe that the interbank offer rate will be roughly 4%. At the end of the year, X will pay Y $50,000 (5% of $1 million). If the interbank offer rate is trading at 4.75%,

Company Y then will have to pay Company X $57,500 (5.75% of $10 lakh, because of the agreement to pay interbank offer rate plus 1%).

Read another article: Impact of Social Security Code, 2020 on Employees’ State Insurance Scheme

Conclusion

Some of the best hedging instruments are Derivatives Contracts like Forward, Futures, Options, and Swap Contracts. It may be a highly useful means of achieving financial goals. It can also help investors leverage their positions by allowing them to purchase equities via stock options rather than shares. But the main drawback of Derivatives includes counterparty risk and the inherent risks of leverage.