Reviewed and Validated by: Aamna Munaima, Associate

Introduction: How to Withdraw Provident Fund Amount?

How to withdraw your Provident Fund Amount, but do not know how? Whether you are quitting your job, retiring, or facing an emergency, knowing the right PF withdrawal process can help you save time, effort, and even money.

Salaried employees in India have access to a government-backed savings scheme known as the Employees’ Provident Fund (EPF), which ensures financial security post-retirement. However, due toa lack of clear guidance, many employees face withdrawal delays, rejected claims, and complex documentation. Have you ever needed to withdraw your hard-earned EPF corpus but found the process confusing? Then this guide is for you. It covers all details from eligibility to withdrawal methods, step-by-step instructions, and some lesser-known hacks to get your EPF corpus without rejection. Read our article: How to Calculate Gratuity in India: Formula, Eligibility & Tax Implications

By the end of this guide, you will clearly understand:

- Types of PF withdrawals (Full, Partial, Transfer) and their unique conditions.

- Who can withdraw the PF, and when is it taxable

- How to withdraw funds without delays or rejections.

- How to apply online and offline for PF withdrawal

- Non-obvious factors that impact claim approval rates.

Beyond structured steps, this guide provides expert tips, insider rules, and practical solutions for almost every PF withdrawal scenario.

How to Withdraw Provident Fund Amount?

Here are the steps to withdraw the Provident Fund amount:

- Visit the EPFO Member Portal – https://unifiedportal-mem.epfindia.gov.in

- Click on ‘Online Services’ and then click on ‘Claim (Form-31, 19 & 10C)’.

- Verify your Aadhaar details and click to proceed with the claim.

- Choose a withdrawal type (full, partial, or pension withdrawal).

- The Bank Account Verification Process and Upload PAN or canceled cheque.

- File the claim and check the status via the EPFO portal.

If all documents and KYC details are updated, the process will be smooth and quick.

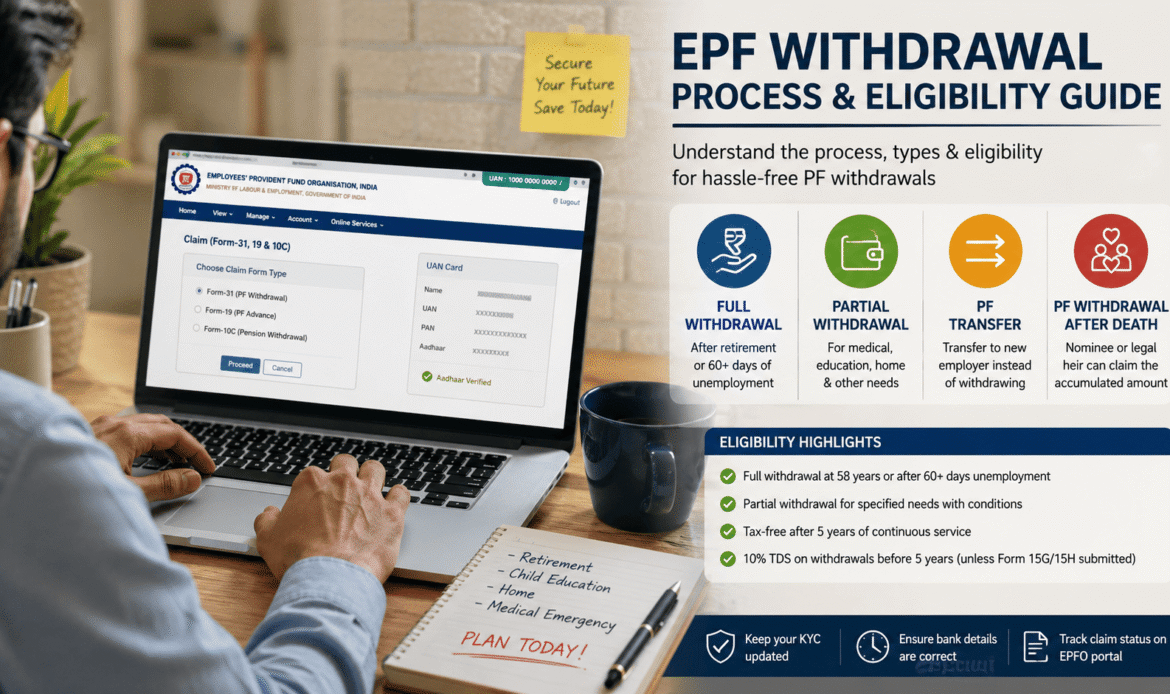

Types of Provident Fund Withdrawals

Before applying for a PF withdrawal, it is essential to know the different kinds of PF withdrawals. Most people withdraw their PF early due to a lack of financial planning, which negatively impacts their long-term retirement savings. Here are the four main types of withdrawals and when they should be used.

1. Full PF Withdrawal (Final Settlement)

- Who is eligible? Employees aged 58 years or more or those employed for 60+ days.

- Why is it important? Final withdrawals enable people to retrieve benefits that combine employer and worker contributions plus interest.

- Key Contributions:

- TDS deduction if the PF account is less than five years old.

- Retirees can opt for an EPF-lined annuity plan instead of withdrawing the lump sum.

- Form 15G/15H must be submitted, if applicable, to avoid the deduction of tax at source (TDS).

2. Partial PF Withdrawal (Advance PF Withdrawal)

Any employee has the option to withdraw part of their PF balance for urgent financial needs without closing their account. Here are some common reasons for partial withdrawals, along with specific limits:

Many employees are not aware that they can avail some portion of a relatively idling PF balance for emergency financial assistance without closing the account. Here are some common reasons why partial withdrawals are made, along with the limits:

| Purpose of Partial Withdrawal | Eligibility Criteria | Maximum Withdrawal Allowed |

| Medical Treatment (self/spouse/children/parents) | Available anytime | whichever is lower (6 months basic salary or total employee share). |

| Higher Education (self/children) | After 7 years of service | 50% of employee share |

| Marriage Expenses (self, siblings, children) | After 7 years of service | 50% of employee share |

| Home Loan Repayment | After 10 years of service | 90% of PF balance |

| House Purchase/Construction | After 5 years of service | 24 months’ basic wages + DA |

- Expert View: Many employees withdraw their PF for weddings or vacations without realizing the long-term impact on retirement savings. These withdrawals should be a last resort.

3. Transfer of PF Amount

Instead of withdrawing, the employees ideally should transfer the PF balance to their new employer’s account when they change jobs.

- Frequent withdrawals disrupt the compounding cycle, reducing the retirement corpus.

- How to transfer? Use the UAN-linked EPFO online portal and use the ‘One Employee, One EPF’ feature.

4. PF Withdrawal After Death

- In case of an unfortunate event of the EPF member passing away, the accumulated balance can be claimed by the nominee or the legal heir.

- Required Documents:

- Death CertificateForm 20 (EPF balance claim)

- Form 10D (if pension is applicable)

- Bank details of the nominee

Expert Tip: Many claims get rejected due to the nominee details being outdated in the EPF account. Hence, employees must ensure their nominee details are updated on the UAN portal to avoid future disputes.

Eligibility Criteria for PF Withdrawal

- Full Withdrawal:

- Available upon retirement at 58 years.

- Permitted after 60+ days of unemployment (employer verification needed).

- Partial Withdrawal:

- Allowed for medical, housing, or education costs, subject to limits.

- Tax-Free Withdrawals:

- Withdrawals after 5 years of continued service are tax-free.

- Withdrawals before 5 years attract a 10% TDS, unless Form 15G/15H is submitted.

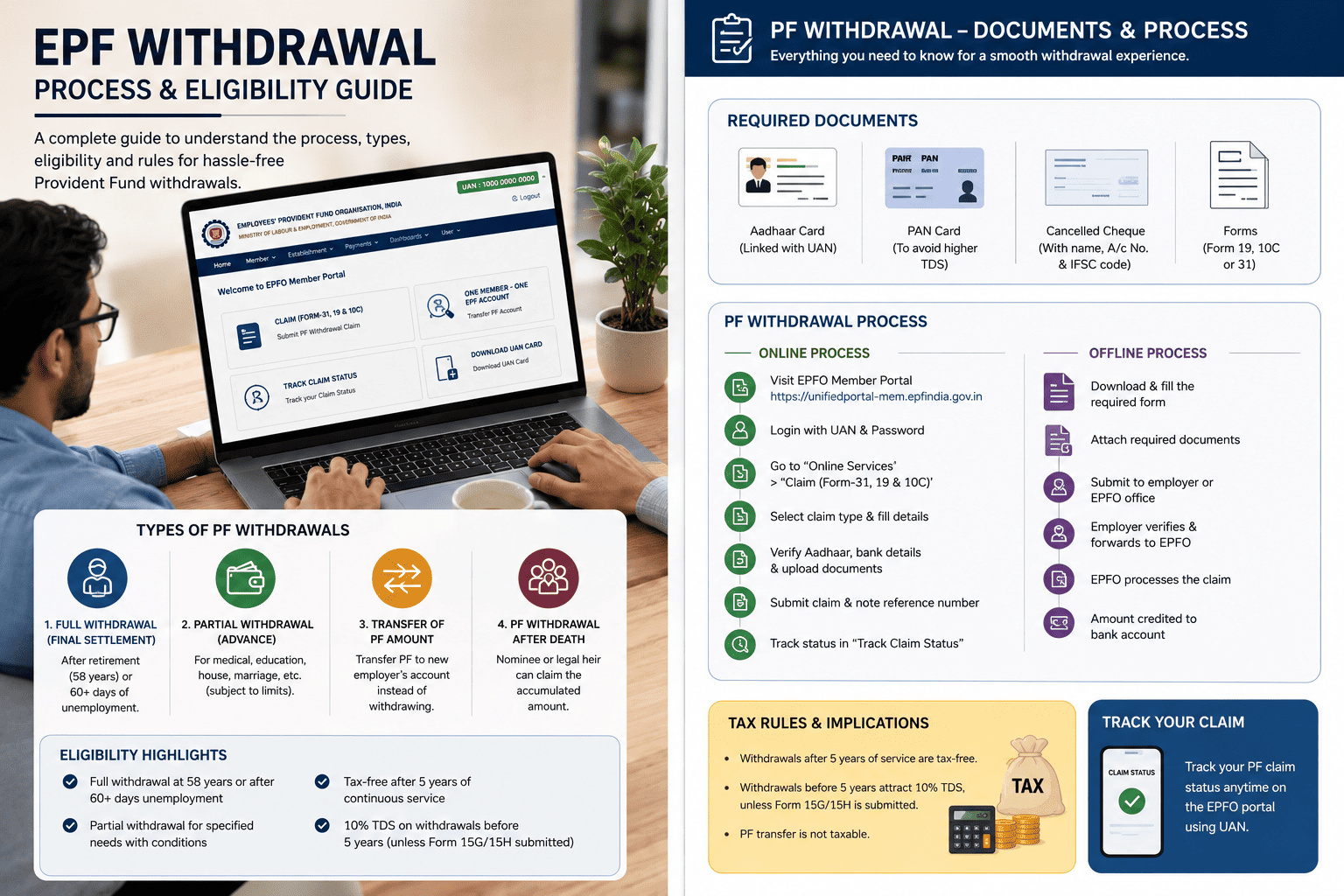

Required Documents for PF Withdrawal

- Aadhaar Card (linked with UAN) – For mandatory online withdrawal.

- PAN Card – Necessary to avoid higher TDS deductions.

- Cancelled Cheque — Must display EPF holder name, account number, and IFSC code.

- Forms – Form 19, Form 10C, or Form 31, and for partial withdrawal, Form 31.

Analysis: Mismatched KYC details lead to higher claim rejection rates. Ensure all given records (Aadhaar, PAN, and bank details) are linked and correctly validated in the EPFO database.

How to Withdraw PF Amount Online?

The Employees’ Provident Fund Organisation (EPFO) has fully digitized the PF withdrawal process, reducing employer intervention. Follow the detailed step-by-step process to withdraw your PF online:

Step 1: Log in to the EPFO Member Portal

- Open the EPFO Unified Member Portal at: https://unifiedportal-mem.epfindia.gov.in/memberinterface/.

- Log in using your UAN (Universal Account Number) and password.

- If you have not activated your UAN, you will have to click on “Activate UAN” and follow the verification process.

Tip: Ensure UAN is linked with Aadhaar, as Aadhaar authentication is mandatory for filing online claims.

Step 2: Go to ‘Online Services’ and Select ‘Claim (Form-31, 19 & 10C)’

- Tap on the ‘Online Services’ tab on the top navigation bar.

- Choose ‘Claim (Form-31, 19 & 10C)’ from the dropdown.

- The system will automatically fetch all the details such as name, date of birth, Aadhaar, PAN, and bank details.

The issue: If you do not have KYC (Know Your Customer) details, the system will not let you proceed. Before proceeding, update KYC from ‘Manage’ → ‘KYC’

Step 3: Check Aadhaar Info, Submit Withdrawal Request

- Check all the details including Bank Account Details and PAN details.

- Click on ‘Proceed for Online Claim’ and enter the Aadhaar-based OTP sent to the registered mobile number.

Security Tip: Never use the EPFO portal on public computers or unsecured networks to avoid data breaches.

Step 4: Choose the Type of Withdrawal

Select the correct withdrawal type according to your qualifications:

- Form 19: Full withdrawal after retirement/unemployment exceeding 2 months.

- Form 10C: Pension withdrawal for employees employed for 10 years or more.

- Form 31 – To withdraw partly for limited purposes (like for medical, education, home loan, etc.)

Step 5: Submit Necessary Documents

The portal will likely ask you to upload:

- Canceled Cheque (must display name and account details).

- Copy of PAN Card (to prevent higher TDS deductions).

- Bank Account Statement (if additional verification is needed).

Imp: Ensure that the name in the bank account must match the EPF record to prevent claim rejection.

Step 6: Submit the Claim and Track Status

- After submitting, a Claim Reference Number (CRN) will be generated.

- Under ‘Online Services’ → ‘Track Claim Status’ to track the status.

- Once approved, the withdrawal amount will be credited to your account, you will get an SMS update.

Processing time: Online claims are usually processed in about 5-15 business days on successful verification by the EPFO.

How to Withdraw PF Amount Offline?

For individuals who prefer a physical claim process, the offline PF withdrawal method is still available. Here is how to withdraw your amount offline:

Step 1: Download the Required Forms

- Visit the EPFO official website or pick up the forms from the nearest EPFO office.

- Choose the correct form:

- Form 19- Final PF withdrawal.

- Form 10C – Application for Assistant Pension.

- Form 31– Advance/Partial Withdrawal Form.

Step 2: Fill in the Form Correctly

Include the report details:

- UAN, Name, and contact number.

- Date of joining and date of relieving from the organization.

- Cause for withdrawal (elderly, illness, accommodation, etc.).

- Aadhaar-linked full banking account details.

Step 3: Append The Required Documents

- Aadhaar Card (linked with UAN copy and bank details.

- PAN Card Copy (For tax purposes).

- Canceled Cheque (it should be as per your PF account).

- Pass Book Copy (for account confirmation).

Step 4: Download and submit the form at the nearest EPFO office

- Visit the regional EPFO office and submit the filled form along with the required documents.

- The duly filled form shall be submitted with documents at the counter.

- Make sure to keep the acknowledgment slip for your records and track the claim status.

Step 5: Claim Processing and Payment Disbursal

- Offline PF withdrawal takes 15-30 days depending on document verification.

- After processing, the respective amount is credited to the bank account.

Pro Tip: If your employer is unresponsive, you can file a self-attested withdrawal form as long your Aadhaar is linked with UAN.

PF Withdrawal Time & Status Tracking

It is important to know the PF withdrawal processing time and how to check the PF withdrawal status.

Processing Time for PF Withdrawal

| Withdrawal Type | Processing Time |

| Online Withdrawal | 5-15 working days |

| Offline Withdrawal | 15-30 working days |

| Partial Withdrawal | 10-20 working days |

| PF Transfer to New Employer | 15-25 working days |

How to Check Our PF Claim Status?

- Online Method:

- Login to EPFO Unified Portal.

- Under Online Services, click on ‘Track Claim Status’.

- SMS Method:

- You can send “EPFOHO UAN ENG” to 7738299899 to get status updates.

Reason for the delay: Incorrect bank details, waiting for employer approval, and KYC record discrepancies.

PF Withdrawal Tax Rules and Implications

Before a withdrawal, it is important to know the PF taxation rules.

When is PF Withdrawal Tax-Free?

- If withdrawn after 5+ years of ongoing service.

- If the amount is transferred to another employer’s PF account and not withdrawn.

When is TDS Applicable?

- Withdrawals before 5 years are subjected to a TDS of 10% (if the PAN is linked).

- TDS @34% is deducted, if PAN is not provided.

How to Prevent TDS on PF Withdrawal?

- If the annual income is below the taxable limit, then submission of Form 15G/15H can help avoid tax.

- Ensure that PAN is linked with UAN to avoid higher TDS deductions.

Common Issues & Solutions in PF Withdrawal

1. Claim Rejection Due to Incorrect Bank Details

- Ensure that the bank account number and IFSC code are correct in correspondence to EPF records.

- Submit a new canceled cheque or a copy of your bank passbook for correction.

2. PF Withdrawal is not approved by the Employer

- If the employer refuses approval, opt for Aadhaar-based online withdrawal.

- File a complaint on the EPF Grievance Portal.

3. Rejection of Claim Due to KYC Problems

- Update Aadhaar, PAN, and Bank Details under ‘Manage KYC’

- If discrepancies exist, they should be reported to the department through the employer by submitting a joint declaration form.

Pro Tip: If your claim is repeatedly denied, visit the nearest EPFO office and file a manual complaint

Frequently Asked Questions (FAQs)

1. How much time will it take to receive the PF withdrawal amount?

Processing time varies from 5-20 days, depending on verification and employer approval.

2. Can I withdraw PF without an employer?

Yes, if Aadhaar is linked to UAN, then the employer’s approval is not required.

3. What happens if my PF claim is rejected?

Verify the discrepancy and update your details in KYC through the EPFO portal before you reapply.

4. Do we need to submit a canceled cheque for PF withdrawal?

Yes, a canceled cheque is needed for bank account verification.

5. How to Withdraw PF if Changed Job?

Instead of withdrawal, transfer PF to the new employer’s account.

6. Can I withdraw my 100% PF amount?

Yes, but only on selected conditions:

- Retirement at age 58 (top of the head and employee contribution and interest accrued).

- Employees who have been terminated without cause for more than 60 days are entitled to full withdrawal.

- The nominee or legal heir can withdraw the full PF amount in case of the death of the account holder.

- Permanent disability allows an employee to access the entire sum before retirement.

- Note: As per tax rules, withdrawal of PF before completing 5 years of continuous service will be subjected to TDS (Tax Deducted at Source) but on submission of Form 15G/15H, it can be claimed as an exemption.

7. Can PF be withdrawn anytime?

No, PF cannot be withdrawn whenever one wishes, instead, there are specific EPFO eligibility rules for the same. Only in cases of retirement (58+ age) or unemployment beyond 60 days, full PF withdrawal is eligible. Partial withdrawals are allowed for medical emergencies (of self, spouse, children, or parents), higher education, loan repayment, marriage, and construction of the house.

8. How do I check my PF balance?

- EPFO Member Portal: Log in at https://passbook.epfindia.gov.in with UAN.

- UMANG App: Check PF balance and claim status via the EPFO services section.

- SMS: Send “EPFOHO UAN ENG” to 7738299899.

- Missed Call: Dial 9966044425 from your registered mobile number.

Conclusion

Withdrawing a Provident Fund (PF) is simple and hassle-free if you follow the right steps. To avoid delays, whether on online withdrawal or physical claim, you must ensure that your KYC details are updated, documents are correct, and eligibility criteria are fulfilled,d which would help to avoid delays and claims.