Reviewed and Validated by: Srijan Jha, Associate

Introduction to the Employees Provident Funds Act, 1952 (Bare Act PDF)

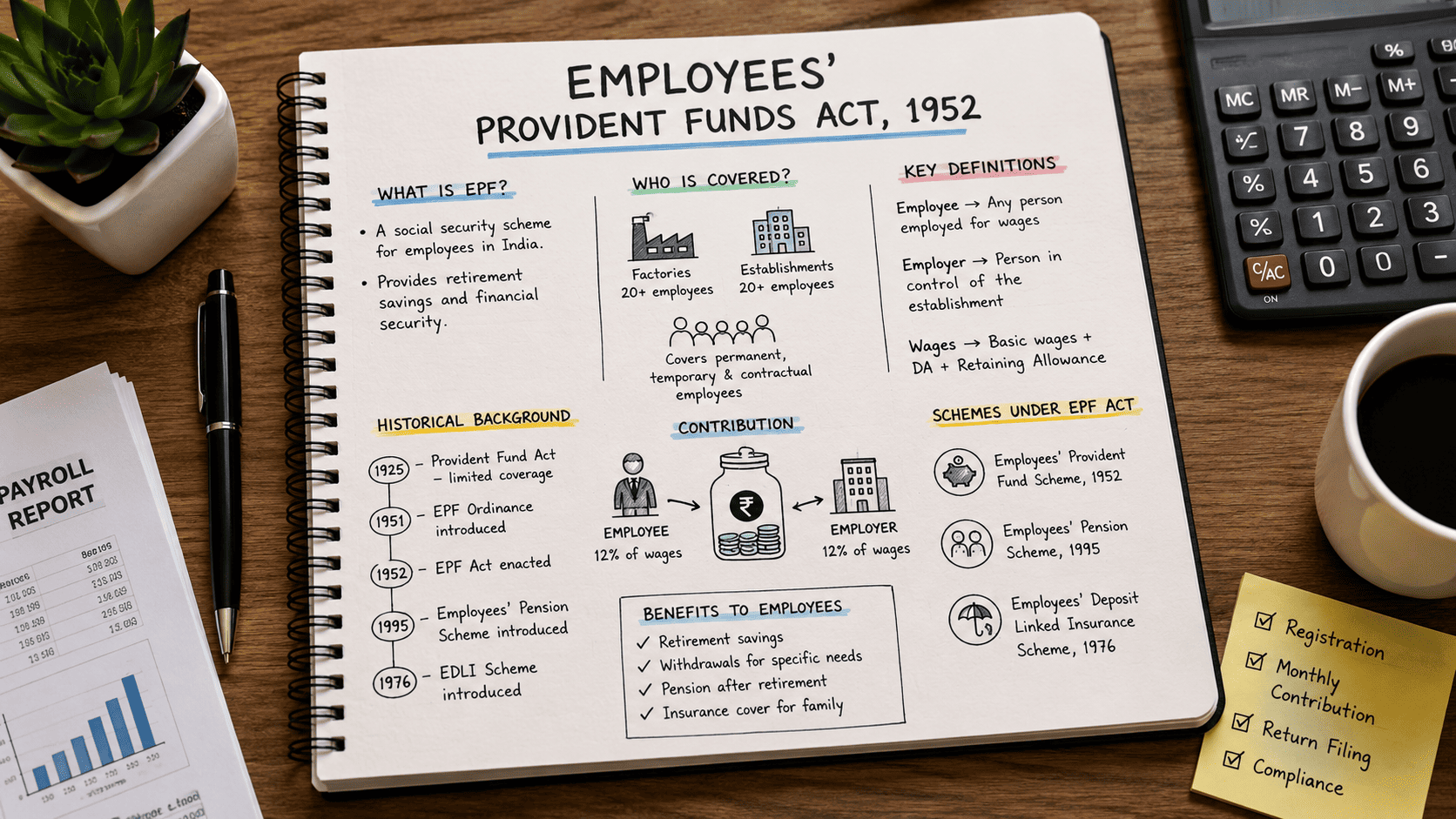

The Employees Provident Funds Act, 1952 bare act PDF is one of the most significant social security laws in India. It was introduced with the central objective of providing financial protection to employees after retirement and during unexpected situations such as illness, disability, or loss of employment. Unlike gratuity, which is a one-time settlement at the end of service, the EPF system is built on continuous contributions that create a retirement corpus over time.

This Act marked a turning point in India’s labour welfare policies. Before its enactment, retirement benefits for workers in the private sector were largely uncertain, dependent on employer discretion, or limited to select industries. The EPF Act created a uniform, statutory scheme that applied across industries and states, giving employees a right to long-term financial security. It also introduced the concept of shared responsibility between employer and employee, making retirement savings a joint effort.

The importance of this Act in India’s social security framework can be seen in its broad application. Today, millions of workers across factories, shops, establishments, and industries rely on the EPF for their retirement savings. The scheme covers not only permanent employees but also contractual and temporary workers, as long as they fall within the definition of “employee” under the Act. By making it mandatory for establishments employing twenty or more persons to comply, the law ensures widespread coverage.

In practice, the working of the EPF can be understood through three simple features:

- Contributions: Both employer and employee contribute a fixed percentage of the employee’s wages into the provident fund every month.

- Accumulation: These contributions earn interest, which accumulates year after year, creating a significant retirement corpus over time.

- Withdrawals: Employees can withdraw the accumulated amount upon retirement, resignation, or in certain permitted cases such as marriage, education, medical emergencies, or purchase of a home.

The Act is also supported by various schemes, such as the Employees’ Pension Scheme and the Employees’ Deposit Linked Insurance Scheme, which add to its role as a comprehensive social security measure. This multi-layered framework means that the EPF Act is not limited to savings alone but extends to pensions and insurance, creating a holistic approach to employee welfare.

For anyone studying or applying the law, the Employees Provident Funds Act, 1952 bare act PDF remains the primary reference. It contains the original statutory provisions as enacted by Parliament, along with subsequent amendments. By reading it alongside executive summaries, compliance guides, and judicial interpretations, employers and employees can fully understand their rights and responsibilities under the law.

Historical Background and Development of the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF was not created in isolation. It grew out of a larger movement to provide workers with financial security in India’s rapidly industrialising economy. Before independence, retirement savings for employees in the private sector were minimal and scattered. Some progressive employers offered provident fund schemes voluntarily, but there was no uniform law to protect all workers.

The earliest step came with the Provident Fund Act of 1925, which applied to limited groups of workers in certain industries. While it was a beginning, it did not provide comprehensive coverage and left most employees without protection. The demand for a nationwide social security framework grew stronger in the 1940s, particularly after the International Labour Organization began emphasising retirement benefits as part of global labour standards.

Recognising this need, the Government of India introduced the Employees Provident Funds Ordinance in 1951, which was soon replaced by the Employees Provident Funds Act, 1952. This marked the first time that retirement savings were made compulsory for a large number of establishments in India. By requiring contributions from both employers and employees, the law ensured that the financial responsibility was shared, making the scheme sustainable and secure.

Key Milestones Highlighted in the EPF Act, 1952 Executive Summary PDF

The Employees Provident Funds Act 1952 executive summary PDF outlines the major stages in the law’s

development:

- 1925: First Provident Fund Act applied only to certain establishments.

- 1951: Introduction of the Employees Provident Funds Ordinance.

- 1952: Enactment of the EPF Act, covering factories and establishments with 20 or more workers.

- 1971: Introduction of the Family Pension Scheme, later replaced by the Employees’ Pension Scheme, 1995.

- 1976: Creation of the Employees’ Deposit Linked Insurance Scheme, adding an insurance element.

- 1995 onwards: Expansion of coverage and strengthening of compliance, making EPF one of the largest social security schemes in the world.

Historical Growth Explained in the Employees Provident Fund Act PDF

The Employees Provident Fund Act PDF Corrida Legal explains how the Act expanded its scope over time. Initially, it was limited to a small set of industries. Over the decades, the Central Government used its powers under the Act to notify more industries, eventually covering almost all sectors of the economy. Amendments raised contribution rates, extended coverage to contract and casual workers, and strengthened penalties for defaulting employers.

This gradual evolution shows how the EPF Act has adapted to the changing labour market in India. What began as a law for industrial workers in large factories is today a law that protects employees in information technology firms, educational institutions, and service industries.

Growth of EPF Explained in the Gratuity Rules in India PDF Download

The gratuity rules in India PDF download, when compared with EPF, highlight how the two laws developed alongside each other. Gratuity provided a one-time payment at the end of service, while EPF created a lifelong savings mechanism. Together, they ensured that workers leaving service had both a lump-sum settlement and a retirement corpus. This dual framework became central to India’s social security policy.

Lessons for Employers from the EPF Compliance Guide PDF

The Employees Provident Fund compliance guide PDF stresses that history has shaped compliance expectations. Early resistance from employers, who saw contributions as an added burden, gave way to acceptance as the law became firmly embedded in India’s employment system. Today, non-compliance is seen not only as a legal violation but as a breach of corporate responsibility. Employers who understand the historical background appreciate why strict timelines, inspections, and penalties are in place, they exist to protect employees from past abuses and uncertainties.

Why the Historical Perspective Matters in the EPF Act 1952 Key Provisions Summary

The EPF Act 1952 key provisions summary highlights that understanding the history of the law is essential for applying it correctly today. Knowing that the Act was created to meet international labour standards, provide security to workers, and distribute responsibility between employers and employees helps stakeholders see it as more than just a statutory obligation. It is part of a larger story of India’s commitment to social justice and worker protection.

Applicability and Coverage under the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF is designed to apply widely across industries to ensure that workers in different sectors enjoy a minimum level of retirement security. The central principle is that establishments employing a certain number of workers must compulsorily register and contribute to the provident fund. This ensures uniformity and prevents selective coverage based on employer discretion.

At the core, the Act applies to factories and other establishments where 20 or more persons are employed. The law also empowers the Central Government to extend its coverage to other classes of establishments by notification. Importantly, once an establishment is brought under the Act, it continues to be governed by it even if the number of employees later falls below the threshold. This prevents employers from evading liability by reducing workforce numbers temporarily.

Coverage Explained in the EPF Act, 1952 Executive Summary PDF

The Employees Provident Funds Act 1952 executive summary PDF notes that coverage is not limited to traditional factories but extends to shops, commercial establishments, and service providers. This wide applicability reflects the changing nature of India’s workforce. Coverage includes:

- Factories engaged in any industry specified in Schedule I.

- Establishments employing twenty or more persons in any industry notified by the Central Government.

- Voluntary coverage if both employer and majority of employees agree, even if the workforce is below twenty.

- Contract labour and temporary workers, where the principal employer remains liable for contributions.

Applicability Clarified in the Employees Provident Fund Act PDF Corrida Legal

The Employees Provident Fund Act PDF Corrida Legal highlights practical aspects of applicability. Many employers mistakenly believe that contract workers engaged through an agency are excluded, but courts have consistently held that principal employers are responsible for ensuring contributions. Educational institutions, hospitals, and IT companies are also covered when they meet the employee threshold.

In practice, coverage rules mean that almost all medium and large establishments in India are now part of the EPF system. Even smaller employers often choose voluntary coverage to provide benefits to their staff and build trust.

Coverage Points from the EPF Rules in India PDF Download

The EPF rules in India PDF download sets out clear compliance points for applicability:

- Establishments employing 20 or more persons must register within one month of coming under coverage.

- Once covered, the establishment remains bound by the Act permanently.

- Separate branches of the same company are treated as one establishment for coverage purposes.

- The Act extends across India, including the Union Territories.

These rules close loopholes and ensure that employers cannot split establishments or manipulate workforce size to avoid obligations.

Compliance Duties under the EPF Compliance Guide PDF

The Employees Provident Fund compliance guide PDF provides employers with a roadmap on how to handle applicability. It recommends that employers:

- Assess headcount carefully to determine coverage at the earliest.

- Register with the Employees Provident Fund Organisation (EPFO) without delay.

- Include all eligible employees, whether permanent, temporary, or contractual.

- Keep payroll and employment records updated for inspections.

These steps ensure that compliance is proactive rather than reactive, reducing the risk of penalties.

Importance of Applicability in the EPF Act 1952 Key Provisions Summary

The EPF Act 1952 key provisions summary makes it clear that applicability rules are central to the functioning of the Act. By extending coverage beyond industrial workers to service and knowledge sectors, the law reflects modern employment realities. For employees, it provides assurance that their retirement savings are protected regardless of the type of establishment they work in. For employers, it signals that compliance is not optional but a continuing statutory duty.

Key Definitions and Concepts in the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF begins with a set of definitions that shape how the law is applied in practice. These definitions are not technicalities but determine who is entitled to provident fund benefits, what counts as wages, and who bears responsibility for compliance. For HR professionals, employers, and employees, clarity on these terms is critical because disputes often arise when they are misunderstood or misapplied.

At the heart of the Act are a few key definitions which frame its operation. The definition of “employee” is deliberately wide, covering not just those on permanent payroll but also contract and temporary workers. The term “employer” includes principal employers and heads of establishments, ensuring accountability cannot be avoided by outsourcing. “Wages” is another important term, as it forms the base for calculating contributions. Together, these concepts define the scope of rights and obligations under the EPF system.

Employee and Employer Defined in the EPF Act, 1952 Executive Summary PDF

The Employees Provident Funds Act 1952 executive summary PDF explains that:

- Employee means any person employed for wages in any kind of work, manual or clerical, skilled or unskilled, in connection with the work of an establishment. The definition includes those employed through contractors.

- Employer refers to the person with ultimate control over the affairs of the establishment. In a company, this is typically the managing director; in a factory, it is the occupier. For contract labour, the principal employer is responsible for contributions.

These wide definitions ensure that most categories of workers and all responsible authorities fall within the scope of the Act.

Wages and Allowances in the Employees Provident Fund Act PDF Corrida Legal

The Employees Provident Fund Act PDF Corrida Legal gives special importance to the definition of “basic wages.” Basic wages include all emoluments earned by an employee while on duty or leave, but exclude specific items such as house rent allowance, overtime allowance, bonus, and commission. This definition has been the subject of much litigation, as employers often try to structure salaries to reduce provident fund liability. Courts have repeatedly held that allowances that are universally and ordinarily paid to employees should be included in wages for EPF purposes.

This interpretation ensures that contributions are calculated on a fair and realistic wage base rather than an artificially reduced figure.

Key Concepts from the EPF Rules in India PDF Download

The EPF rules in India PDF download provides practical guidance on how definitions operate in compliance:

- An employee remains covered until his or her wages exceed the statutory wage ceiling, though once covered, they may continue under the scheme.

- Apprentices engaged under the Apprentices Act, 1961, are excluded.

- Casual or daily wage employees are covered if they meet the definition of employee.

- “Exempted establishments” are those permitted to manage their own provident funds, subject to strict regulatory approval.

These rules help HR departments apply definitions correctly when onboarding employees or managing payroll.

Compliance Guidance in the EPF Compliance Guide PDF

The Employees Provident Fund compliance guide PDF stresses that definitions are the foundation of compliance. Employers must:

- Ensure all categories of employees are enrolled from day one.

- Calculate contributions on wages correctly, including all allowances that qualify under court rulings.

- Recognise that principal employers are responsible for contract workers’ compliance.

- Maintain updated records to avoid penalties during inspections.

Misunderstanding these definitions is one of the most common causes of EPF disputes and penalties.

Importance of Definitions in the EPF Act 1952 Key Provisions Summary

The EPF Act 1952 key provisions summary underlines that definitions are not abstract legal terms but the starting point for enforcing rights and duties. Employees gain security when definitions are applied correctly, and employers avoid disputes when they follow the statutory meaning. By defining employee, employer, and wages in broad but clear terms, the Act ensures inclusivity and accountability in India’s largest retirement savings system.

Schemes under the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF is not limited to creating a single provident fund. Instead, it establishes a broader framework of schemes that together form India’s most important social security mechanism for employees. These schemes cover retirement savings, pension benefits, and life insurance, making the Act a comprehensive instrument of financial protection.

The Act empowers the Central Government to frame schemes for provident funds, pensions, and insurance. Over time, three major schemes have been introduced, each serving a different purpose. Together, they ensure that an employee not only saves for retirement but also receives a pension for life and an insurance cover for unforeseen death during service.

Provident Fund Scheme in the EPF Act, 1952 Executive Summary PDF

The Employees Provident Funds Act 1952 executive summary PDF explains the first and most central

scheme: the Employees’ Provident Fund Scheme, 1952. Under this scheme:

- Both employer and employee contribute a prescribed percentage of wages to the provident fund every month.

- Contributions earn interest, which is credited annually to employees’ accounts.

- The accumulated balance, including interest, is payable at retirement, resignation, or death.

- Partial withdrawals are allowed for specific purposes such as marriage, education, medical treatment, and purchase of a house.

This scheme creates a secure retirement corpus for employees, which is one of the primary objectives of the Act.

Pension Scheme Explained in the Employees Provident Fund Act PDF Corrida Legal

The Employees Provident Fund Act PDF Corrida Legal highlights the Employees’ Pension Scheme (EPS), introduced in 1995 to replace the earlier Family Pension Scheme. The pension scheme ensures that employees not only receive a lump-sum provident fund but also a lifelong pension.

Key features include:

- A portion of the employer’s contribution is diverted to the pension fund.

- Employees completing ten years of eligible service are entitled to a pension on retirement.

- Widows, children, and nominees receive pension benefits in case of the employee’s death.

- Early pension is available from the age of 50 with reduced benefits, while full pension starts at 58. This scheme addresses the need for regular post-retirement income.

Insurance Scheme in the EPF Rules in India PDF Download

The EPF rules in India PDF download also explains the Employees’ Deposit Linked Insurance Scheme (EDLI), introduced in 1976. This scheme provides life insurance benefits linked to the employee’s service under the EPF.

Salient features of EDLI are:

- Provides an insurance cover to nominees or legal heirs in case of death of a member during service.

- No separate premium is payable by employees; contributions are made by employers.

- The insurance amount is linked to the average balance in the provident fund account, subject to prescribed ceilings.

- This ensures financial protection to families during the most difficult times.

Compliance with Schemes in the EPF Compliance Guide PDF

The Employees Provident Fund compliance guide PDF stresses that employers must ensure compliance with all three schemes:

- Deduct and deposit contributions promptly.

- File electronic returns and maintain individual account details.

- Keep nomination forms updated for provident fund, pension, and insurance benefits.

- Educate employees about the benefits and procedures for withdrawals or claims.

Failure to comply with even one scheme can result in penalties, recovery proceedings, and loss of benefits to employees.

Importance of Schemes in the EPF Act 1952 Key Provisions Summary

The EPF Act 1952 key provisions summary makes it clear that the three schemes together create a balanced system of security. The provident fund ensures long-term savings, the pension scheme provides monthly income in retirement, and the insurance scheme protects dependents against loss of life. By integrating these schemes, the Act covers the full cycle of employment and post-employment financial security.

Compliance Duties of Employers under the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF places significant compliance responsibilities on employers. Since the scheme is contributory in nature, the law ensures that employers not only deduct and deposit contributions but also maintain records, file returns, and cooperate with inspections. These duties are essential for safeguarding employees’ rights and ensuring the smooth operation of India’s largest social security framework.

The compliance burden is intentionally strict because past experience showed that voluntary schemes often failed due to poor record-keeping and non-payment by employers. By making compliance mandatory, the Act ensures that employees’ savings are not left to the discretion of management but are secured by law.

Registration and Enrolment in the EPF Act, 1952 Executive Summary PDF

The Employees Provident Funds Act 1952 executive summary PDF explains that the first compliance duty of an employer is to register the establishment with the Employees’ Provident Fund Organisation (EPFO). Once

registered, employers must enrol all eligible employees from the first day of employment. Employer obligations at this stage include:

- Submitting details of establishment and employees to the EPFO.

- Generating Universal Account Numbers (UAN) for employees.

- Ensuring that contract and temporary workers are also enrolled.

- Displaying notices regarding provident fund benefits at the workplace.

Contribution and Deposits in the Employees Provident Fund Act PDF Corrida Legal

The Employees Provident Fund Act PDF Corrida Legal details that employers must deduct employee contributions from wages and match them with equal employer contributions. These must be deposited with the EPFO within prescribed timelines, usually by the 15th of every month.

Compliance points include:

- Calculating contributions on basic wages, dearness allowance, and retaining allowance.

- Splitting employer contributions between provident fund, pension fund, and insurance.

- Avoiding artificial salary structuring to reduce contribution liability.

- Ensuring prompt deposits, as delays attract interest and damages.

Filing Returns and Records in the EPF Rules in India PDF Download

The EPF rules in India PDF download requires employers to maintain accurate records of wages, contributions, and membership details. They must also file electronic returns through the EPFO portal.

Key compliance requirements are:

- Monthly filing of Electronic Challan-cum-Return (ECR).

- Maintaining inspection registers and employee-wise contribution records.

- Submitting annual returns where required.

- Ensuring accuracy of data, as errors may delay employee benefits.

Inspections and Enforcement in the EPF Compliance Guide PDF

The Employees Provident Fund compliance guide PDF stresses that employers must cooperate fully with inspections and audits by EPFO officers. Inspectors have powers to demand records, verify accounts, and question management. Non-compliance may lead to penalties and even prosecution.

Employers are advised to:

- Keep payroll and wage registers up-to-date.

- Reconcile contribution records with bank deposits.

- Rectify errors promptly when pointed out by authorities.

- Treat inspections as part of routine compliance rather than an exceptional burden.

Why Employer Compliance Matters in the EPF Act 1952 Key Provisions Summary

The EPF Act 1952 key provisions summary highlights that compliance duties are not merely bureaucratic requirements but the foundation of employee welfare. Contributions, records, and returns ensure that employees receive their provident fund, pension, and insurance benefits without delay or dispute. Employers who treat compliance seriously not only avoid penalties but also build trust and goodwill among their workforce.

Enforcement, Penalties, and Dispute Resolution under the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF not only creates rights for employees but also establishes strict enforcement mechanisms to ensure compliance. The responsibility to enforce the Act rests primarily with the Employees’ Provident Fund Organisation (EPFO), which has the authority to inspect establishments, recover dues, and penalise defaulters. These enforcement provisions are necessary because provident fund contributions represent employees’ long-term savings, and any default can cause significant financial loss.

Employers who fail to comply face interest charges, damages, and even criminal prosecution in serious cases. At the same time, the Act provides avenues for resolving disputes through quasi-judicial bodies, so that both employers and employees can seek fair determination of issues without unnecessary litigation.

Enforcement Powers in the EPF Act, 1952 Executive Summary PDF

The Employees Provident Funds Act 1952 executive summary PDF highlights the enforcement powers of the EPFO:

- Inspectors can demand production of records, verify wage registers, and question management.

- Recovery officers have powers similar to those under the Income Tax Act to recover arrears, including attachment of bank accounts or property.

- Defaulting employers can be prosecuted in criminal courts for wilful non-payment.

These provisions underline the seriousness with which the law treats provident fund contributions.

Penalties Explained in the Employees Provident Fund Act PDF Corrida Legal

The Employees Provident Fund Act PDF Corrida Legal sets out specific penalties for different violations:

- Late payment of contributions: Attracts statutory interest.

- Default in remittance: Leads to additional damages ranging from 5% to 25% depending on the period of delay.

- Failure to maintain records or submit returns: Punishable with fines and prosecution.

- Wilful default: Can result in imprisonment of up to three years.

By prescribing both financial and criminal consequences, the Act ensures that compliance is taken seriously.

Recovery Procedures in the EPF Rules in India PDF Download

The EPF rules in India PDF download explains the recovery procedures in case of defaults:

- Dues may be recovered by attachment and sale of employer’s movable or immovable property.

- Bank accounts can be frozen and balances appropriated towards dues.

- Recovery can also be made from third parties owing money to the defaulting employer.

- Disputes over the quantum of dues are decided by the EPF authorities, subject to appeal. These recovery tools make the Act self-enforcing and reduce dependence on prolonged litigation.

Dispute Resolution in the EPF Compliance Guide PDF

The Employees Provident Fund compliance guide PDF notes that disputes often arise over applicability, calculation of wages, or exemption claims. To resolve such disputes, the Act provides for quasi-judicial determination by officers such as the Regional Provident Fund Commissioner. Appeals lie to the Employees’ Provident Fund Appellate Tribunal, and further to the High Court on substantial questions of law.

Employers and employees benefit from this structured mechanism because:

- It provides specialised forums familiar with provident fund issues.

- It ensures quicker resolution compared to ordinary civil courts.

- It reduces uncertainty by offering authoritative rulings.

Importance of Enforcement in the EPF Act 1952 Key Provisions Summary

The EPF Act 1952 key provisions summary emphasises that enforcement is the backbone of the law. Without strict penalties and recovery mechanisms, the scheme would risk non-compliance, leaving employees vulnerable. By combining proactive inspections, financial penalties, and judicial forums, the Act ensures that provident fund contributions remain secure. For employers, it is a reminder that compliance is not optional; for employees, it is an assurance that their savings are protected by law.

Judicial Pronouncements on the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF has been the subject of frequent interpretation by the judiciary. While the statute provides the framework, many of its provisions have been clarified through judgments of the Supreme Court and High Courts. Courts have consistently upheld the pro-employee spirit of the Act, reinforcing that provident fund contributions are not a matter of contract but a statutory obligation that employers cannot evade.

Judicial decisions have shaped key aspects such as the definition of wages, liability of principal employers, coverage of contract workers, and the consequences of default. These rulings ensure that the Act is applied fairly while preventing employers from exploiting loopholes.

Landmark Rulings in the EPF Act, 1952 Executive Summary PDF

The Employees Provident Funds Act 1952 executive summary PDF highlights that the Supreme Court has repeatedly emphasised the welfare character of the Act. Important rulings include:

- Bridge and Roof Co. v. Union of India — Confirmed that the Act is a beneficial legislation and must be interpreted in favour of employees.

- Daily Partap v. Regional Provident Fund Commissioner — Held that contract and temporary workers are also covered under the definition of employee.

- Regional Provident Fund Commissioner v. Hooghly Mills Co. — Reiterated that principal employers are responsible for ensuring compliance for contract labour.

These rulings underline the judiciary’s commitment to protecting workers’ retirement savings.

Wages Dispute Clarified in the Employees Provident Fund Act PDF Corrida Legal

The Employees Provident Fund Act PDF Corrida Legal discusses the landmark case of Manipal Academy of Higher Education v. Provident Fund Commissioner. The Supreme Court held that allowances that are universally, necessarily, and ordinarily paid to employees must be included in the definition of basic wages. This judgment expanded the contribution base and prevented employers from artificially reducing their liability by excluding allowances.

Other rulings, such as Surya Roshni Ltd. v. EPFO, have reinforced this principle, leading to stricter scrutiny of salary structures by authorities.

Case Law in the EPF Rules in India PDF Download

The EPF rules in India PDF download refers to judicial pronouncements clarifying recovery and enforcement:

- Courts have upheld the power of EPFO officers to determine dues under Section 7A of the Act.

- High Courts have stressed that recovery proceedings cannot be stalled by filing writ petitions unless there is a clear case of violation of natural justice.

- The judiciary has emphasised that employees’ savings cannot be compromised by procedural delays or employer defaults.

Judicial Insights in the EPF Compliance Guide PDF

The Employees Provident Fund compliance guide PDF explains that employers must align their practices with judicial rulings. Compliance lessons include:

- Structuring wages transparently to avoid disputes.

- Recognising contract workers as covered employees.

- Avoiding prolonged litigation, as courts generally rule in favour of employees in EPF matters.

- Treating provident fund contributions as a priority financial obligation.

Importance of Judicial Pronouncements in the EPF Act 1952 Key Provisions Summary

The EPF Act 1952 key provisions summary shows that judicial pronouncements are not just clarifications but essential components of the law. By resolving ambiguities, courts ensure that the Act evolves with changing employment patterns. For employees, these rulings strengthen protection; for employers, they provide authoritative guidance on compliance.

EPF Act vs Other Social Security Laws in India (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF is part of a larger framework of labour welfare and social security laws in India. While the EPF Act focuses on creating long-term retirement savings through monthly contributions, other social security laws address different but complementary aspects such as gratuity, medical benefits, or insurance coverage. Understanding these distinctions helps employers maintain compliance across multiple statutes and allows employees to appreciate how different benefits work together to provide financial security.

Comparison with Gratuity in the EPF Act, 1952 Executive Summary PDF

The Employees Provident Funds Act 1952 executive summary PDF often compares EPF with the Payment of Gratuity Act, 1972.

- EPF: A contributory scheme where both employer and employee contribute regularly, creating a retirement corpus.

- Gratuity: A one-time lump sum paid by the employer at the end of service, requiring no employee contribution.

- Complementary nature: Together, they ensure employees receive both periodic savings and a final reward for service.

This shows how provident fund and gratuity operate as two pillars of India’s social security system.

Contrast with ESI in the Employees Provident Fund Act PDF Corrida Legal

The Employees Provident Fund Act PDF Corrida Legal notes that the Employees’ State Insurance Act, 1948 (ESI Act) has a different purpose.

- EPF: Focuses on retirement security and post-employment benefits.

- ESI: Provides medical benefits, sickness benefits, and maternity benefits during service.

- Coverage: EPF applies to establishments with 20 or more employees, while ESI generally covers employees earning wages up to a notified ceiling.

Both laws complement each other, EPF secures the future while ESI protects present health and welfare needs.

Integration with Labour Codes in the EPF Rules in India PDF Download

The EPF rules in India PDF download also discusses the future of EPF under the Code on Social Security, 2020. The Code seeks to consolidate multiple labour welfare laws, including the EPF Act, Gratuity Act, and ESI Act. The objective is to create a unified framework that simplifies compliance while continuing to protect workers’ rights.

Key expected outcomes are:

- Single registration for multiple social security schemes.

- Coverage extended to gig workers and fixed-term employees.

- Streamlined enforcement and digital compliance systems.

Employer Perspective in the EPF Compliance Guide PDF

The Employees Provident Fund compliance guide PDF reminds employers that compliance with EPF does not reduce obligations under other laws. Employers must separately comply with gratuity, ESI, and bonus obligations. Together, these statutes create a holistic employee welfare framework, and failure under one cannot be offset by compliance with another.

Employers are advised to:

- Maintain integrated HR and payroll systems.

- Conduct joint audits for all labour law compliances.

- Communicate clearly to employees about different benefits available to them.

Broader Context in the EPF Act 1952 Key Provisions Summary

The EPF Act 1952 key provisions summary highlights that provident fund is only one part of India’s evolving social security system. Employees rely on a combination of provident fund, gratuity, insurance, and health benefits to achieve financial stability. By comparing EPF with other social security laws, it becomes clear that no single law is sufficient on its own — they must be viewed together as a network of protections designed to safeguard the workforce.

Download Resources for the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF is most useful when supported by well-structured resources that simplify its practical application. For students, employers, HR professionals, and compliance officers, access to reliable downloads saves time and ensures accuracy. Corrida Legal makes these resources available in multiple formats so that users can move beyond statutory text and apply the law effectively in their workplace or studies.

Employees Provident Funds Act, 1952 Executive Summary PDF

The Employees Provident Funds Act 1952 executive summary PDF condenses the statutory framework into a practical overview. It highlights eligibility, contribution rules, employee rights, and employer obligations.

This resource is especially helpful for:

- Students preparing for legal or professional exams.

- HR managers setting up provident fund systems.

- Employees who want to quickly understand their entitlements.

- Employers needing a quick compliance reference.

Accessing the Employees Provident Fund Act PDF Corrida Legal

The Employees Provident Fund Act PDF Corrida Legal is more than just the statutory text. It provides additional commentary, examples of wage calculations, and references to case law. This makes it an essential tool for professionals who need both the bare provisions and their practical interpretation.

It is typically used for:

- Drafting internal policies aligned with EPF law.

- Guiding payroll teams in applying contribution rules.

- Preparing for inspections and audits.

- Educating employees about their provident fund rights.

EPF Rules in India PDF Download

The EPF rules in India PDF download compiles the procedural details required for day-to-day compliance. It sets out forms, returns, inspection powers, and recovery mechanisms.

Employers often rely on this resource for:

- Filing monthly Electronic Challan-cum-Return (ECR).

- Maintaining registers and inspection records.

- Understanding penalties and damages for defaults.

- Ensuring correct application of withdrawal and transfer rules.

Employer Tools in the EPF Compliance Guide PDF

The Employees Provident Fund compliance guide PDF offers ready-to-use tools such as checklists, calculation tables, and compliance timelines. By using these tools, employers can reduce errors and ensure their obligations are met on time.

This guide supports:

- Conducting self-audits of EPF compliance.

- Forecasting financial liabilities for contributions.

- Training HR and payroll staff.

- Reducing litigation risk by following best practices.

Summary of Downloadable Resources in the EPF Act 1952 Key Provisions Summary

The EPF Act 1952 key provisions summary explains that downloadable resources together create a complete package:

- Bare act for statutory reference.

- Executive summary for simplified understanding.

- Corrida Legal PDF for commentary and guidance.

- Rules PDF for procedural compliance.

- Compliance guide for practical tools.

This layered approach ensures that both employers and employees have access to the information they need at the right level of detail.

FAQs on the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF often raises questions for employees, employers, and HR professionals. While the statutory provisions are clear, practical doubts arise during implementation. Below are answers to some of the most frequently asked questions, explained in simple language but with statutory accuracy.

Who is covered under the Employees Provident Funds Act, 1952 Executive Summary PDF?

The Employees Provident Funds Act 1952 executive summary PDF clarifies that:

- All establishments employing 20 or more persons are mandatorily covered.

- Employees earning wages up to the statutory ceiling are automatically enrolled.

- Voluntary coverage is possible even for smaller establishments if both employer and majority of employees agree.

- Contract and temporary workers are also covered, with the principal employer responsible for contributions.

What is the current contribution rate under the Employees Provident Fund Act PDF Corrida Legal?

The Employees Provident Fund Act PDF Corrida Legal sets the standard contribution rate at 12% of an employee’s wages, payable both by the employee and the employer. In some cases, such as small establishments with fewer than 20 employees, the rate may be reduced to 10%.

Breakdown of contributions:

- Employer’s share: split between provident fund, pension scheme, and insurance scheme.

- Employee’s share: entirely towards the provident fund.

- Both contributions together build the retirement corpus.

Can employees withdraw money from the EPF rules in India PDF download before retirement?

Yes, the EPF rules in India PDF download allow withdrawals under specific conditions:

- Marriage or education of self, children, or siblings.

- Medical emergencies for self or family.

- Purchase or construction of a house.

- Repayment of housing loans.

- Retirement after 58 years or permanent disablement.

However, full withdrawal is generally allowed only at retirement or after two months of unemployment.

What happens if an employer defaults, as explained in the EPF compliance guide PDF?

The Employees Provident Fund compliance guide PDF makes it clear that employer default is treated very seriously:

- Interest is charged on late payments.

- Damages up to 25% may be levied based on the period of default.

- Recovery proceedings can include attachment of bank accounts and property.

- Criminal prosecution may follow in cases of wilful non-payment.

Employees are protected because the EPFO has strong recovery powers to secure their savings.

Are contract workers eligible for benefits under the EPF Act 1952 key provisions summary?

The EPF Act 1952 key provisions summary confirms that contract workers are also treated as employees under the Act. The responsibility for compliance lies with the principal employer, even if wages are paid through a contractor. This ensures that all workers, regardless of mode of employment, have access to provident fund benefits.

Is EPF taxable under the Employees Provident Funds Act, 1952 bare act PDF?

While the Act itself does not deal with taxation, income tax rules apply:

- Employee contributions qualify for deduction under Section 80C of the Income Tax Act.

- Employer’s contributions are not taxed at the time of deposit.

- Withdrawals are tax-free if made after five years of continuous service.

- Early withdrawals may attract tax on the employee’s contribution and interest.

This makes EPF not only a social security measure but also a tax-saving investment.

Conclusion on the Employees Provident Funds Act, 1952 (Bare Act PDF)

The Employees Provident Funds Act, 1952 bare act PDF is not just a statute; it is a cornerstone of India’s social security framework. By creating a contributory system of retirement savings, it ensures that millions of employees across industries have a reliable financial cushion for their post-employment years. Over the decades, the Act has evolved through amendments, rules, and judicial pronouncements, but its central purpose has remained the same, to provide dignity, stability, and protection to workers.

For employees, the EPF system is more than a deduction from monthly wages. It represents a secure, interest-bearing investment that grows silently over the years, ensuring a sizeable corpus at retirement or in times of need. For employers, it is a statutory duty that must be carried out with diligence, transparency, and consistency. Non-compliance not only attracts penalties but also erodes employee trust and damages organisational credibility.

Conclusion

The Wholly Owned Subsidiary in India is a strong path that the foreign corporations would aim to have full control and local presence. It involves a rigorous procedure to incorporate a WOS in India, ensuring compliance with the Companies Act, FEMA and sectoral policy of FDI and careful preparation of documents. Although the regulatory system might be perceived to be complicated, reforms, including the SPICe+ form and liberalised FDI policy, have made the process easier. Incorporation can be performed perfectly and work successfully through proper planning, utilising professional advisers, and timely compliance. The long consumer base, available skilled labour force, combined with the increased economy of India, means that a WOS gives foreign investors a lucrative tool to develop sustainable business ventures coupled with the advantages of ownership, flexibility and access to incentives.