Reviewed and Validated by: Aakrist Goyal, Associate

This is the second part of the three-part series where we discuss the types of White-collar crimes in India. This article shall aim to elucidate the prominent types of White-collar crimes in India. It may well be noted that the first part spoke of the concept, origin and scope of White-collar crimes.

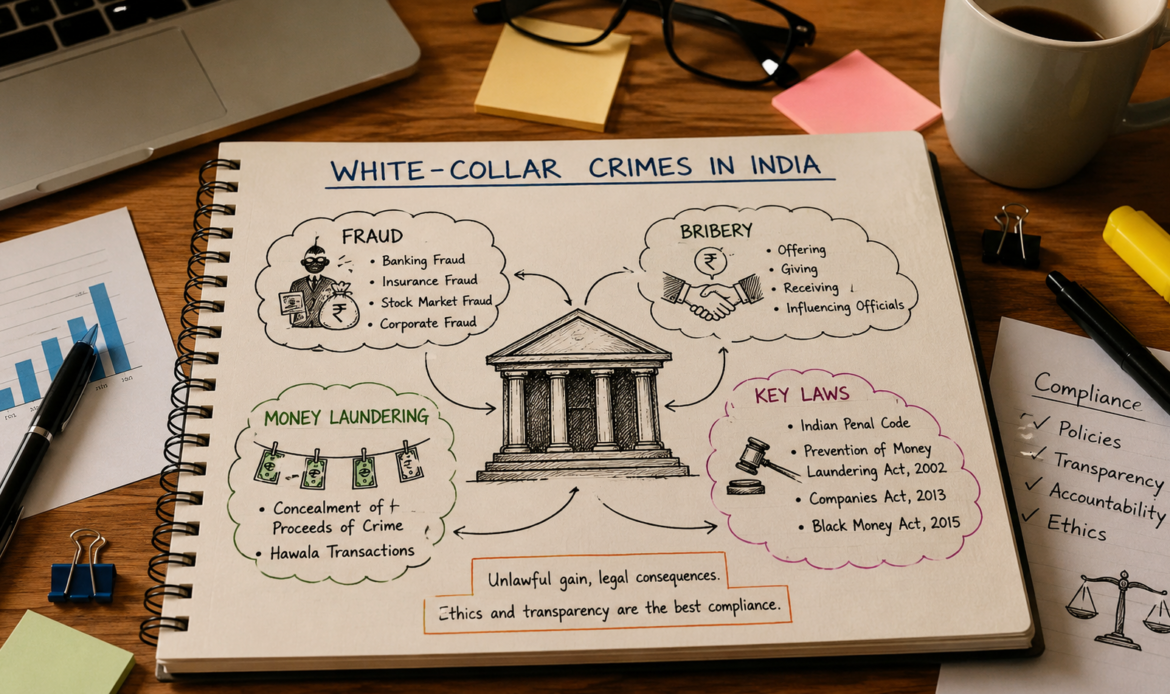

Types of White-collar crimes in India

Fraud:

Section 17 of the Indian Contract Act, 1872 defines fraud as acts committed by a party to a contract, or with his connivance, or by his agent, with an intent to deceive another party thereto of his agent, or to induce him to enter into the contract. These acts include, inter alia, active concealment, untrue suggestions and false promises.

Section 447 of The Companies Act, 2013 deals with the punishment for fraud which states that any person who is found guilty of fraud shall be punishable with imprisonment for a term which shall be not less that 6 (six) months but which may extend to 10 (ten) years and shall also be liable to fine which shall not be less than the amount involved in the fraud, but which may extend to 3 (three) times the amount involved in the fraud. Where the fraud in question involves public interest, the term of imprisonment shall not be less than 3 (three) years.

It may well be noted that fraud in itself is a very large category, which includes within it, a variety of White-collar crimes. An example of fraud is banking fraud, where, a person may withdraw the money or assets from a bank or falsely represent himself/herself as a representative of the bank to induce people to submit money or assets to them. Another example of banking frauds can be obtaining loans basis unreliable or forged documents. One more category of a common White-collar fraud is insurance fraud, which involves persons obtaining insurance money through false documents, by staging theft, accident or any other injury that is covered by an insurance policy.

Another important category of White-collar fraud in India comes through the illegal sale of stocks by showing a wrongfully inflated price of a stock to induce people to invest in that stock. Lately, corporate fraud has also emerged as a serious White-collar crime that involves fraudulent acts in the context of the affairs of a company. The Companies Act, 2013 has created several provisions to detect, prevent and penalize corporate fraud, which have been dealt with in the sections mentioned below.

Bribery

Black’s Law Dictionary defines Bribery as the offering, giving, receiving, or soliciting of any item of value to influence the actions of an official, or other person, in charge of public or legal duty. It may be done for the purpose of insisting a public official to do something or to prevent them from doing something.

While the Indian Penal Code punishes bribery as an ‘election offence’, the Prevention of Money Laundering Act (PMLA) 2002 covers all kinds of bribery offences committed by domestic public officials. The term public officials include anyone who is authorized to perform a public function. The Case of Central Bureau of Investigation, Bank Securities and Fraud Cell v Ramesh Gelli and Ors has held that even the chairman or MDs of private banking companies can fall within the definition of ‘public officials’ if they are authorized or required to perform a public duty.

Bribery can either be done either directly (through himself or herself) or through a third party, in which case the third party can also be held liable. While public bribery is prohibited extensively, no specific regulations are covering private/commercial bribery. Usually, companies and organisations formulate their own internal regulations prohibiting such instances of bribery.

Read another article: Recent Amendments and Trends in Indian Contract Law

Money Laundering

Section 3 of the PMLA defines the offence as a direct or indirect attempt at indulging in any process or activity connected with the proceeds of crime and projecting it as untainted property. In India, money laundering is popularly referred to as a ‘Hawala transaction’.

The PMLA punishes concealment, possession, acquisition or use of proceeds of crime or attempting to project or claim that such proceeds are not laundered. Mens rea has been implied to be an important element for such offences, provided that PMLA uses the term ‘knowingly’ while describing the offences, which has been interpreted to communicate guilty intention, as held in A K Mukherjee v State.

In addition, regulators such as the Reserve Bank of India, the Securities Exchange Board of India and the Insurance Regulatory and the Development Authority of India have also issued regulations concerning money laundering. Furthermore, the Black Money Act of 2015 empowers the Central government to seek details, investigate and carry out discovery on undisclosed bank accounts and assets.

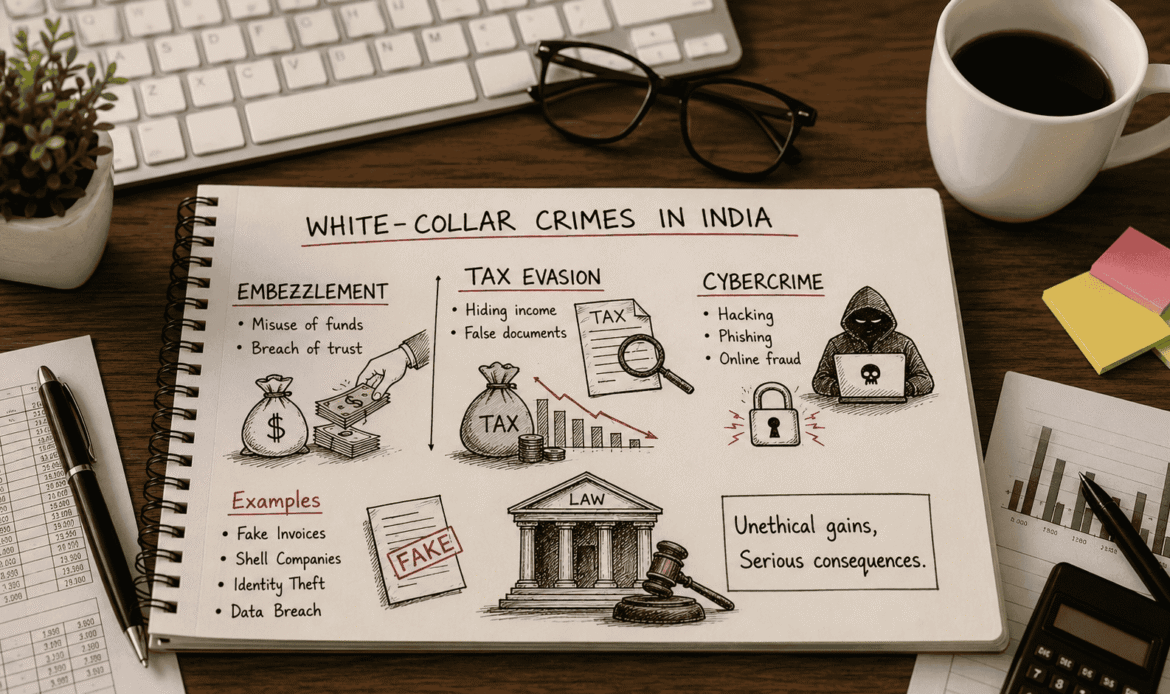

Embezzlement

When an individual, who is entrusted by his or her employer’s money or property either to be held or to be used for specific purposes, misappropriates such resources or falsely converts it to his/her own use or disposes it without any law allowing him to do so, commits an act of embezzlement. Embezzlement is a criminal offence which may be punishable under Section 408, 420 of the Indian Penal Code, dealing with Criminal Breach of Trust by Clerk or Servant , Cheating and dishonestly inducing delivery of property respectively.

It is essential that the parties involved must have shared a fiduciary relationship, which compelled one party to provide money or assets to the other party. Subsequently, the party who was entrusted with the funds uses it for a different purpose than they were intended to be used. Individuals who are entrusted with access to an organization’s funds are expected to safeguard those assets for their intended use. Mens rea is an important element to constitute such an offence. The Allahabad HC has held that even if the amount of embezzlement is insignificant, an employee can be terminated because the mens rea in such offences is enough justification to dismiss a delinquent employee.

Tax Evasion

Tax evasion occurs when a person deliberately forges his or her state of affairs, to deceive the taxing authorities to levy a lesser amount of tax. This can either be done by an individual, a corporation or a trust. It can be calculated as the difference between the amount of tax lawfully required to be reported and the amount reported by a tax evader. The Income Tax Act (ITA), 1961 under Chapter 22 has proscribed that the offence of tax evasion can result in a fine as well as imprisonment.

Some instances of tax evasion constitute a failure to file income tax returns, as laid down under Section 139(1) of the ITA, not providing a PAN card or providing a fake one, giving false information under form 26AS. Recently, the Income Tax Appellate Tribunal, in the case of Galaxy Nirman Pvt Ltd v. Acit, New Delhi has also held that failure to pay the entire amount of self-assessment tax would constitute penal damages.

Cybercrime

Cybercrime is a novel and developing field of law in India. No particular statute has expressly defined the term, but it can be considered as unlawful acts wherein a computer is either a tool or a target. The Information Technology Act of 2000 is the primary legislation that punishes cybercrime under Section 43, 66, 67, 69, and 72 of the Act. It must be noted that Section 66A of the IT Act, dealing with punishment for sending offensive messages through communication service was held unconstitutional via the landmark Shreya Singhal judgement. Certain White-collar cybercrime include: hacking of an account with a view to access a person’s bank or credit/debit card details, phishing i.e., deceiving people into entering their bank account details or scamming individuals into buying counterfeit products. Crimes against the government like hacking government websites or databases have also been held to be a White-collar cybercrime.

This is the second part of the three-part series where we discuss the types of White-collar crimes in India. This article shall aim to elucidate the prominent types of White-collar crimes in India. It may well be noted that the first part spoke of the concept, origin and scope of White-collar crimes.